|

市場調查報告書

商品編碼

1414709

第二代生質燃料的全球市場:按類型、原料、製程和應用:機會分析和產業預測(2023-2032)Second Generation Biofuels Market By Type, By Feedstock, By Process, By Application : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

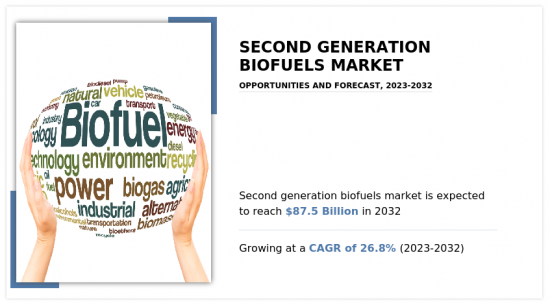

預計2022年全球第二代生質燃料市場規模將達82億美元,2023年至2032年複合年成長率為26.8%,2032年將達875億美元。

第二代生質燃料,也稱為先進生質燃料,是由工業和家庭的殘留物和廢棄物生產的。

大量廢煎炸油和屠宰場廢棄物也被用來生產生質燃料。此外,它是由非食用作物生產的,例如農業殘留物、木片和小麥生產中的秸稈,以及從木質纖維素作物中獲得。此生產技術可以分離植物木質素和纖維素,並將纖維素發酵成酒精。第二代生質燃料工業定義了有機碳的任何來源,因此這些生質燃料是由不同類型的生質能生產的。

第二代生質燃料透過永續且經濟實惠地提供更多生質燃料來解決第一代生質燃料的局限性,並具有顯著的環境效益。 <它還具有多種優點,例如:

大多數廉價且豐富的非糧食原料包括穀物秸稈、砂糖渣、森林殘渣、城市固態廢棄物的有機成分等產品,以及營養草和矮樹梢等專用原料將會出現。

原料木質纖維素是地球上最豐富的生質能,由大約 70% 的糖組成。這種糖在轉化為生質乙醇和其他生質燃料之前要經過各種過程。

生物纖維素提供了一種永續的能源來源,不會損害其從糧食生產中轉移的土地或環境。它還有助於解決現代社會廢棄物造成的問題,並為弱勢群體提供以前不存在的就業機會。充足的生質燃料生產和分配不但不會造成糧食短缺,反而為新興低度開發國家提供了實現長期經濟成長的最佳機會。生質燃料有潛力帶來真正的市場競爭和更低的油價。根據《華爾街日誌》報道,如果沒有生質燃料,原油價格將上漲 15%,汽油價格可能會上漲 25%。替代能源的健康供應將有助於應對汽油價格急劇上升。上述趨勢和各種用途需求的存在正在推動第二代生質燃料市場的成長。

第二代生質燃料市場的成長受到低溫性能不佳、纖維素轉化效率以及原料污染造成的疾病傳播風險的阻礙。第二代生質燃料市場分為原料、類型、製程、應用和區域。

依原料分類,全球第二代生質燃料市場分為簡單木質纖維素、複雜木質纖維素、合成氣、藻類等。按類型分類,全球第二代生質燃料市場分為纖維素乙醇、生質柴油、生物丁醇等。依製程分類,全球第二代生質燃料市場分為生化製程和熱化學製程。按應用分類,全球第二代生質燃料市場分為交通運輸、發電等。

按地區分類,調查涵蓋北美、歐洲、亞太地區以及拉丁美洲/中東/非洲。 2020年,北美市場佔有率最大,亞太地區成長最快。本報告主要企業包括 Algenol Biofuels、Clariant AG、International Flavors & Fragrances Inc、Fiberight LLC、GranBio、Ineos Group、Orsted A/S、POET-DSM Advanced Biofuels LLC、Reliance Industries、Zea2, LLCs 等。

目錄

第1章簡介

第 2 章執行摘要

第3章市場概況

- 市場定義和範圍

- 主要發現

- 影響因素

- 主要投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 能源安全疑慮

- 環境法規

- 抑制因素

- 生產成本高

- 缺乏基礎設施

- 機會

- 可再生能源儲存

- 促進因素

- 價值鏈分析

- 關鍵監管分析

- 價格分析

第4章第二代生質燃料市場:依類型

- 概述

- 纖維素乙醇

- 生質柴油

- 生物丁醇

- 其他

第5章 第二代生質燃料市場:依原料分類

- 概述

- 簡單木質纖維素

- 複合木質纖維素

- 合成氣

- 藻類

- 其他

第6章 第二代生質燃料市場:依流程

- 概述

- 生化過程

- 熱化學過程

第7章 第二代生質燃料市場:依應用分類

- 概述

- 運輸

- 發電

- 其他

第8章第二代生質燃料市場:按地區

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 泰國

- 其他

- 拉丁美洲/中東/非洲

- 巴西

- 南非

- 以色列

- 其他

第9章 競爭形勢

- 介紹

- 關鍵成功策略

- 10家主要企業產品圖譜

- 競爭對手儀表板

- 競爭熱圖

- 主要企業定位(2022年)

第10章 公司簡介

- Algenol Biotech LLC

- Clariant AG.

- International Flavors & Fragrances Inc.

- Fiberight

- GranBio Investimentos SA

- INEOS Group

- Orsted A/S

- POET-DSM Advanced Biofuels LLC

- Reliance Industries Limited

- Zea2

According to a new report published by Allied Market Research, titled, "Second Generation Biofuels Market," The second generation biofuels market was valued at $8.2 billion in 2022, and is estimated to reach $87.5 billion by 2032, growing at a CAGR of 26.8% from 2023 to 2032.

Second generation biofuels are also known as advanced biofuels that are produced from residual and waste products such as

1) industry and households. Large quantities of used frying oil and slaughterhouse waste are also used in producing them. In addition, they are also produced from non-food crops including agricultural residue, wood chips, and wheat straw from wheat production. It is derived from lignocellulosic crops. This generation technology allows the lignin and cellulose of plants to be separated so that cellulose is fermented into alcohol. These biofuels are manufactured from different types of biomasses as it defines any source of organic carbon in second generation biofuel industry.

Second-generation biofuels solve the limitations of first-generation biofuels such as

1), it supply a larger proportion of biofuel sustainably and affordably with greater environmental benefits. The presence of various advantages such as

1) the majority of the cheap and abundant nonfood materials include by-products such as

1) cereal straw, sugar bagasse, forest residues; waste such as

1) organic components from municipal solid wastes; and dedicated feedstocks such as

1) vegetative grasses, and short-rotation forests. The presence of the raw material lignocellulose is the most abundant biomass on earth, consisting of about 70% sugars, which depend on various processes before they are transformed into bioethanol or other biofuels.

It provides a sustainable energy source that does not require any land to be converted from food production or harm the environment. It also assist in solving the difficulties caused by contemporary society waste and offer jobs for the underprivileged where none existed previously. Far from causing food shortages, proper biofuel production and distribution provide the finest chance for emerging and underdeveloped countries to achieve long-term economic growth. Biofuels provide the potential of genuine market competition and a drop in oil prices. According to the Wall Street Journal, if it were not for biofuels, crude oil would be 15% higher and gasoline would be up to 25% more expensive. A healthy supply of alternative energy resources will help to combat gasoline price hikes. The abovementioned trends and presence of demand for various purposes drive the growth of the second-generation biofuels market.

The growth of the second generation biofuel market is hampered due to its low performance in cold temperatures, efficiency of the cellulose conversion, and the risk of spreading sickness from contaminated feedstocks. The second generation biofuels market scope is segmented into feedstock, type, process, application, and region.

On the basis of feedstock, the global second generation biofuels market is categorized into simple lignocellulose, complex lignocellulose, syngas, algae, and others. By type, the global second generation biofuels market is classified into cellulosic ethanol, biodiesel, bio butanol, and others. On the basis of process, the global second generation biofuels market is segregated into biochemical process and thermochemical process. By application, the global second generation biofuels market is divided into transportation, power generation, and others.

Region wise, the market is studied across North America, Europe, Asia-Pacific, and LAMEA. North America accounted for the largest share of the market in 2020, with Asia-Pacific being the fastest growing region. The major companies profiled in this report include Algenol Biofuels, Clariant AG, International Flavors & Fragrances Inc, Fiberight LLC., GranBio, Ineos Group, Orsted A/S, POET-DSM Advanced Biofuels LLC, Reliance Industries, and Zea2, LLC.

In addition to the abovementioned companies, there are Algae. Tec, Chemrec Inc., Gevo, Inc., and Muradel competing for the share of the market through product launch, joint venture, partnership, and expanding the production capabilities to meet the future demand for the second generation biofuels market forecast period.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the second generation biofuels market analysis from 2022 to 2032 to identify the prevailing second generation biofuels market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the second generation biofuels market size segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global second generation biofuels market trends, key players, market segments, application areas, and second generation biofuels market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Investment Opportunities

- Upcoming/New Entrant by Regions

- Technology Trend Analysis

- Regulatory Guidelines

- Strategic Recommedations

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- Import Export Analysis/Data

- Market share analysis of players at global/region/country level

- Volume Market Size and Forecast

Key Market Segments

By Type

- Cellulosic Ethanol

- Biodiesel

- Bio Butanol

- Others

By Feedstock

- Simple Lignocellulose

- Complex Lignocellulose

- Syngas

- Algae

- Others

By Process

- Biochemical Process

- Thermochemical Process

By Application

- Transportation

- Power Generation

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- Italy

- Spain

- UK

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Thailand

- Rest of Asia-Pacific

- LAMEA

- Brazil

- South Africa

- Israel

- Rest of LAMEA

Key Market Players:

- INEOS Group

- Algenol Biotech LLC

- Fiberight

- International Flavors & Fragrances Inc.

- Reliance Industries Limited

- Clariant AG.

- Orsted A/S

- POET-DSM Advanced Biofuels LLC

- Zea2

- GranBio Investimentos S.A.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Low bargaining power of suppliers

- 3.3.2. Low threat of new entrants

- 3.3.3. Low threat of substitutes

- 3.3.4. Low intensity of rivalry

- 3.3.5. Low bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Energy Security Concerns

- 3.4.1.2. Environment Regulations

- 3.4.2. Restraints

- 3.4.2.1. High Production Costs

- 3.4.2.2. Lack of Infrastructure

- 3.4.3. Opportunities

- 3.4.3.1. Renewable Energy Storage

- 3.4.1. Drivers

- 3.5. Value Chain Analysis

- 3.6. Key Regulation Analysis

- 3.7. Pricing Analysis

CHAPTER 4: SECOND GENERATION BIOFUELS MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Cellulosic Ethanol

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Biodiesel

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Bio Butanol

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Others

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

CHAPTER 5: SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Simple Lignocellulose

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Complex Lignocellulose

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Syngas

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Algae

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

- 5.6. Others

- 5.6.1. Key market trends, growth factors and opportunities

- 5.6.2. Market size and forecast, by region

- 5.6.3. Market share analysis by country

CHAPTER 6: SECOND GENERATION BIOFUELS MARKET, BY PROCESS

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Biochemical Process

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Thermochemical Process

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

CHAPTER 7: SECOND GENERATION BIOFUELS MARKET, BY APPLICATION

- 7.1. Overview

- 7.1.1. Market size and forecast

- 7.2. Transportation

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by region

- 7.2.3. Market share analysis by country

- 7.3. Power Generation

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by region

- 7.3.3. Market share analysis by country

- 7.4. Others

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by region

- 7.4.3. Market share analysis by country

CHAPTER 8: SECOND GENERATION BIOFUELS MARKET, BY REGION

- 8.1. Overview

- 8.1.1. Market size and forecast By Region

- 8.2. North America

- 8.2.1. Key market trends, growth factors and opportunities

- 8.2.2. Market size and forecast, by Type

- 8.2.3. Market size and forecast, by Feedstock

- 8.2.4. Market size and forecast, by Process

- 8.2.5. Market size and forecast, by Application

- 8.2.6. Market size and forecast, by country

- 8.2.6.1. U.S.

- 8.2.6.1.1. Market size and forecast, by Type

- 8.2.6.1.2. Market size and forecast, by Feedstock

- 8.2.6.1.3. Market size and forecast, by Process

- 8.2.6.1.4. Market size and forecast, by Application

- 8.2.6.2. Canada

- 8.2.6.2.1. Market size and forecast, by Type

- 8.2.6.2.2. Market size and forecast, by Feedstock

- 8.2.6.2.3. Market size and forecast, by Process

- 8.2.6.2.4. Market size and forecast, by Application

- 8.2.6.3. Mexico

- 8.2.6.3.1. Market size and forecast, by Type

- 8.2.6.3.2. Market size and forecast, by Feedstock

- 8.2.6.3.3. Market size and forecast, by Process

- 8.2.6.3.4. Market size and forecast, by Application

- 8.3. Europe

- 8.3.1. Key market trends, growth factors and opportunities

- 8.3.2. Market size and forecast, by Type

- 8.3.3. Market size and forecast, by Feedstock

- 8.3.4. Market size and forecast, by Process

- 8.3.5. Market size and forecast, by Application

- 8.3.6. Market size and forecast, by country

- 8.3.6.1. Germany

- 8.3.6.1.1. Market size and forecast, by Type

- 8.3.6.1.2. Market size and forecast, by Feedstock

- 8.3.6.1.3. Market size and forecast, by Process

- 8.3.6.1.4. Market size and forecast, by Application

- 8.3.6.2. France

- 8.3.6.2.1. Market size and forecast, by Type

- 8.3.6.2.2. Market size and forecast, by Feedstock

- 8.3.6.2.3. Market size and forecast, by Process

- 8.3.6.2.4. Market size and forecast, by Application

- 8.3.6.3. Italy

- 8.3.6.3.1. Market size and forecast, by Type

- 8.3.6.3.2. Market size and forecast, by Feedstock

- 8.3.6.3.3. Market size and forecast, by Process

- 8.3.6.3.4. Market size and forecast, by Application

- 8.3.6.4. Spain

- 8.3.6.4.1. Market size and forecast, by Type

- 8.3.6.4.2. Market size and forecast, by Feedstock

- 8.3.6.4.3. Market size and forecast, by Process

- 8.3.6.4.4. Market size and forecast, by Application

- 8.3.6.5. UK

- 8.3.6.5.1. Market size and forecast, by Type

- 8.3.6.5.2. Market size and forecast, by Feedstock

- 8.3.6.5.3. Market size and forecast, by Process

- 8.3.6.5.4. Market size and forecast, by Application

- 8.3.6.6. Rest of Europe

- 8.3.6.6.1. Market size and forecast, by Type

- 8.3.6.6.2. Market size and forecast, by Feedstock

- 8.3.6.6.3. Market size and forecast, by Process

- 8.3.6.6.4. Market size and forecast, by Application

- 8.4. Asia-Pacific

- 8.4.1. Key market trends, growth factors and opportunities

- 8.4.2. Market size and forecast, by Type

- 8.4.3. Market size and forecast, by Feedstock

- 8.4.4. Market size and forecast, by Process

- 8.4.5. Market size and forecast, by Application

- 8.4.6. Market size and forecast, by country

- 8.4.6.1. China

- 8.4.6.1.1. Market size and forecast, by Type

- 8.4.6.1.2. Market size and forecast, by Feedstock

- 8.4.6.1.3. Market size and forecast, by Process

- 8.4.6.1.4. Market size and forecast, by Application

- 8.4.6.2. Japan

- 8.4.6.2.1. Market size and forecast, by Type

- 8.4.6.2.2. Market size and forecast, by Feedstock

- 8.4.6.2.3. Market size and forecast, by Process

- 8.4.6.2.4. Market size and forecast, by Application

- 8.4.6.3. India

- 8.4.6.3.1. Market size and forecast, by Type

- 8.4.6.3.2. Market size and forecast, by Feedstock

- 8.4.6.3.3. Market size and forecast, by Process

- 8.4.6.3.4. Market size and forecast, by Application

- 8.4.6.4. Thailand

- 8.4.6.4.1. Market size and forecast, by Type

- 8.4.6.4.2. Market size and forecast, by Feedstock

- 8.4.6.4.3. Market size and forecast, by Process

- 8.4.6.4.4. Market size and forecast, by Application

- 8.4.6.5. Rest of Asia-Pacific

- 8.4.6.5.1. Market size and forecast, by Type

- 8.4.6.5.2. Market size and forecast, by Feedstock

- 8.4.6.5.3. Market size and forecast, by Process

- 8.4.6.5.4. Market size and forecast, by Application

- 8.5. LAMEA

- 8.5.1. Key market trends, growth factors and opportunities

- 8.5.2. Market size and forecast, by Type

- 8.5.3. Market size and forecast, by Feedstock

- 8.5.4. Market size and forecast, by Process

- 8.5.5. Market size and forecast, by Application

- 8.5.6. Market size and forecast, by country

- 8.5.6.1. Brazil

- 8.5.6.1.1. Market size and forecast, by Type

- 8.5.6.1.2. Market size and forecast, by Feedstock

- 8.5.6.1.3. Market size and forecast, by Process

- 8.5.6.1.4. Market size and forecast, by Application

- 8.5.6.2. South Africa

- 8.5.6.2.1. Market size and forecast, by Type

- 8.5.6.2.2. Market size and forecast, by Feedstock

- 8.5.6.2.3. Market size and forecast, by Process

- 8.5.6.2.4. Market size and forecast, by Application

- 8.5.6.3. Israel

- 8.5.6.3.1. Market size and forecast, by Type

- 8.5.6.3.2. Market size and forecast, by Feedstock

- 8.5.6.3.3. Market size and forecast, by Process

- 8.5.6.3.4. Market size and forecast, by Application

- 8.5.6.4. Rest of LAMEA

- 8.5.6.4.1. Market size and forecast, by Type

- 8.5.6.4.2. Market size and forecast, by Feedstock

- 8.5.6.4.3. Market size and forecast, by Process

- 8.5.6.4.4. Market size and forecast, by Application

CHAPTER 9: COMPETITIVE LANDSCAPE

- 9.1. Introduction

- 9.2. Top winning strategies

- 9.3. Product mapping of top 10 player

- 9.4. Competitive dashboard

- 9.5. Competitive heatmap

- 9.6. Top player positioning, 2022

CHAPTER 10: COMPANY PROFILES

- 10.1. Algenol Biotech LLC

- 10.1.1. Company overview

- 10.1.2. Key executives

- 10.1.3. Company snapshot

- 10.1.4. Operating business segments

- 10.1.5. Product portfolio

- 10.2. Clariant AG.

- 10.2.1. Company overview

- 10.2.2. Key executives

- 10.2.3. Company snapshot

- 10.2.4. Operating business segments

- 10.2.5. Product portfolio

- 10.2.6. Business performance

- 10.2.7. Key strategic moves and developments

- 10.3. International Flavors & Fragrances Inc.

- 10.3.1. Company overview

- 10.3.2. Key executives

- 10.3.3. Company snapshot

- 10.3.4. Operating business segments

- 10.3.5. Product portfolio

- 10.3.6. Business performance

- 10.3.7. Key strategic moves and developments

- 10.4. Fiberight

- 10.4.1. Company overview

- 10.4.2. Key executives

- 10.4.3. Company snapshot

- 10.4.4. Operating business segments

- 10.4.5. Product portfolio

- 10.5. GranBio Investimentos S.A.

- 10.5.1. Company overview

- 10.5.2. Key executives

- 10.5.3. Company snapshot

- 10.5.4. Operating business segments

- 10.5.5. Product portfolio

- 10.5.6. Business performance

- 10.5.7. Key strategic moves and developments

- 10.6. INEOS Group

- 10.6.1. Company overview

- 10.6.2. Key executives

- 10.6.3. Company snapshot

- 10.6.4. Operating business segments

- 10.6.5. Product portfolio

- 10.6.6. Business performance

- 10.7. Orsted A/S

- 10.7.1. Company overview

- 10.7.2. Key executives

- 10.7.3. Company snapshot

- 10.7.4. Operating business segments

- 10.7.5. Product portfolio

- 10.7.6. Business performance

- 10.8. POET-DSM Advanced Biofuels LLC

- 10.8.1. Company overview

- 10.8.2. Key executives

- 10.8.3. Company snapshot

- 10.8.4. Operating business segments

- 10.8.5. Product portfolio

- 10.9. Reliance Industries Limited

- 10.9.1. Company overview

- 10.9.2. Key executives

- 10.9.3. Company snapshot

- 10.9.4. Operating business segments

- 10.9.5. Product portfolio

- 10.9.6. Business performance

- 10.10. Zea2

- 10.10.1. Company overview

- 10.10.2. Key executives

- 10.10.3. Company snapshot

- 10.10.4. Operating business segments

- 10.10.5. Product portfolio

LIST OF TABLES

- TABLE 01. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 02. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 03. SECOND GENERATION BIOFUELS MARKET FOR CELLULOSIC ETHANOL, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. SECOND GENERATION BIOFUELS MARKET FOR CELLULOSIC ETHANOL, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 05. SECOND GENERATION BIOFUELS MARKET FOR BIODIESEL, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. SECOND GENERATION BIOFUELS MARKET FOR BIODIESEL, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 07. SECOND GENERATION BIOFUELS MARKET FOR BIO BUTANOL, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. SECOND GENERATION BIOFUELS MARKET FOR BIO BUTANOL, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 09. SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 11. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 12. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 13. SECOND GENERATION BIOFUELS MARKET FOR SIMPLE LIGNOCELLULOSE, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. SECOND GENERATION BIOFUELS MARKET FOR SIMPLE LIGNOCELLULOSE, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 15. SECOND GENERATION BIOFUELS MARKET FOR COMPLEX LIGNOCELLULOSE, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. SECOND GENERATION BIOFUELS MARKET FOR COMPLEX LIGNOCELLULOSE, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 17. SECOND GENERATION BIOFUELS MARKET FOR SYNGAS, BY REGION, 2022-2032 ($MILLION)

- TABLE 18. SECOND GENERATION BIOFUELS MARKET FOR SYNGAS, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 19. SECOND GENERATION BIOFUELS MARKET FOR ALGAE, BY REGION, 2022-2032 ($MILLION)

- TABLE 20. SECOND GENERATION BIOFUELS MARKET FOR ALGAE, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 21. SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 22. SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 23. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 24. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 25. SECOND GENERATION BIOFUELS MARKET FOR BIOCHEMICAL PROCESS, BY REGION, 2022-2032 ($MILLION)

- TABLE 26. SECOND GENERATION BIOFUELS MARKET FOR BIOCHEMICAL PROCESS, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 27. SECOND GENERATION BIOFUELS MARKET FOR THERMOCHEMICAL PROCESS, BY REGION, 2022-2032 ($MILLION)

- TABLE 28. SECOND GENERATION BIOFUELS MARKET FOR THERMOCHEMICAL PROCESS, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 29. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 30. GLOBAL SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 31. SECOND GENERATION BIOFUELS MARKET FOR TRANSPORTATION, BY REGION, 2022-2032 ($MILLION)

- TABLE 32. SECOND GENERATION BIOFUELS MARKET FOR TRANSPORTATION, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 33. SECOND GENERATION BIOFUELS MARKET FOR POWER GENERATION, BY REGION, 2022-2032 ($MILLION)

- TABLE 34. SECOND GENERATION BIOFUELS MARKET FOR POWER GENERATION, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 35. SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 36. SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 37. SECOND GENERATION BIOFUELS MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 38. SECOND GENERATION BIOFUELS MARKET, BY REGION, 2022-2032 (MILLION LITERS)

- TABLE 39. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 40. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 41. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 42. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 43. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 44. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 45. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 46. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 47. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 48. NORTH AMERICA SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 (MILLION LITERS)

- TABLE 49. U.S. SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 50. U.S. SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 51. U.S. SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 52. U.S. SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 53. U.S. SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 54. U.S. SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 55. U.S. SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 56. U.S. SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 57. CANADA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 58. CANADA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 59. CANADA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 60. CANADA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 61. CANADA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 62. CANADA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 63. CANADA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 64. CANADA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 65. MEXICO SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 66. MEXICO SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 67. MEXICO SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 68. MEXICO SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 69. MEXICO SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 70. MEXICO SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 71. MEXICO SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 72. MEXICO SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 73. EUROPE SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 74. EUROPE SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 75. EUROPE SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 76. EUROPE SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 77. EUROPE SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 78. EUROPE SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 79. EUROPE SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 80. EUROPE SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 81. EUROPE SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 82. EUROPE SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 (MILLION LITERS)

- TABLE 83. GERMANY SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 84. GERMANY SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 85. GERMANY SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 86. GERMANY SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 87. GERMANY SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 88. GERMANY SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 89. GERMANY SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 90. GERMANY SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 91. FRANCE SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 92. FRANCE SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 93. FRANCE SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 94. FRANCE SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 95. FRANCE SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 96. FRANCE SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 97. FRANCE SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 98. FRANCE SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 99. ITALY SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 100. ITALY SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 101. ITALY SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 102. ITALY SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 103. ITALY SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 104. ITALY SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 105. ITALY SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 106. ITALY SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 107. SPAIN SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 108. SPAIN SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 109. SPAIN SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 110. SPAIN SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 111. SPAIN SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 112. SPAIN SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 113. SPAIN SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 114. SPAIN SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 115. UK SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 116. UK SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 117. UK SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 118. UK SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 119. UK SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 120. UK SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 121. UK SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 122. UK SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 123. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 124. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 125. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 126. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 127. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 128. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 129. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 130. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 131. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 132. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 133. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 134. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 135. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 136. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 137. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 138. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 139. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 140. ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 (MILLION LITERS)

- TABLE 141. CHINA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 142. CHINA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 143. CHINA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 144. CHINA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 145. CHINA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 146. CHINA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 147. CHINA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 148. CHINA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 149. JAPAN SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 150. JAPAN SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 151. JAPAN SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 152. JAPAN SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 153. JAPAN SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 154. JAPAN SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 155. JAPAN SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 156. JAPAN SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 157. INDIA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 158. INDIA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 159. INDIA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 160. INDIA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 161. INDIA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 162. INDIA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 163. INDIA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 164. INDIA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 165. THAILAND SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 166. THAILAND SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 167. THAILAND SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 168. THAILAND SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 169. THAILAND SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 170. THAILAND SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 171. THAILAND SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 172. THAILAND SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 173. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 174. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 175. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 176. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 177. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 178. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 179. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 180. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 181. LAMEA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 182. LAMEA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 183. LAMEA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 184. LAMEA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 185. LAMEA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 186. LAMEA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 187. LAMEA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 188. LAMEA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 189. LAMEA SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 190. LAMEA SECOND GENERATION BIOFUELS MARKET, BY COUNTRY, 2022-2032 (MILLION LITERS)

- TABLE 191. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 192. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 193. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 194. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 195. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 196. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 197. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 198. BRAZIL SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 199. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 200. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 201. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 202. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 203. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 204. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 205. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 206. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 207. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 208. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 209. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 210. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 211. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 212. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 213. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 214. ISRAEL SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 215. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 216. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022-2032 (MILLION LITERS)

- TABLE 217. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 ($MILLION)

- TABLE 218. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022-2032 (MILLION LITERS)

- TABLE 219. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 220. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022-2032 (MILLION LITERS)

- TABLE 221. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 222. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022-2032 (MILLION LITERS)

- TABLE 223. ALGENOL BIOTECH LLC: KEY EXECUTIVES

- TABLE 224. ALGENOL BIOTECH LLC: COMPANY SNAPSHOT

- TABLE 225. ALGENOL BIOTECH LLC: PRODUCT SEGMENTS

- TABLE 226. ALGENOL BIOTECH LLC: PRODUCT PORTFOLIO

- TABLE 227. CLARIANT AG.: KEY EXECUTIVES

- TABLE 228. CLARIANT AG.: COMPANY SNAPSHOT

- TABLE 229. CLARIANT AG.: PRODUCT SEGMENTS

- TABLE 230. CLARIANT AG.: PRODUCT PORTFOLIO

- TABLE 231. CLARIANT AG.: KEY STRATERGIES

- TABLE 232. INTERNATIONAL FLAVORS & FRAGRANCES INC.: KEY EXECUTIVES

- TABLE 233. INTERNATIONAL FLAVORS & FRAGRANCES INC.: COMPANY SNAPSHOT

- TABLE 234. INTERNATIONAL FLAVORS & FRAGRANCES INC.: PRODUCT SEGMENTS

- TABLE 235. INTERNATIONAL FLAVORS & FRAGRANCES INC.: PRODUCT PORTFOLIO

- TABLE 236. INTERNATIONAL FLAVORS & FRAGRANCES INC.: KEY STRATERGIES

- TABLE 237. FIBERIGHT: KEY EXECUTIVES

- TABLE 238. FIBERIGHT: COMPANY SNAPSHOT

- TABLE 239. FIBERIGHT: PRODUCT SEGMENTS

- TABLE 240. FIBERIGHT: PRODUCT PORTFOLIO

- TABLE 241. GRANBIO INVESTIMENTOS S.A.: KEY EXECUTIVES

- TABLE 242. GRANBIO INVESTIMENTOS S.A.: COMPANY SNAPSHOT

- TABLE 243. GRANBIO INVESTIMENTOS S.A.: PRODUCT SEGMENTS

- TABLE 244. GRANBIO INVESTIMENTOS S.A.: PRODUCT PORTFOLIO

- TABLE 245. GRANBIO INVESTIMENTOS S.A.: KEY STRATERGIES

- TABLE 246. INEOS GROUP: KEY EXECUTIVES

- TABLE 247. INEOS GROUP: COMPANY SNAPSHOT

- TABLE 248. INEOS GROUP: PRODUCT SEGMENTS

- TABLE 249. INEOS GROUP: PRODUCT PORTFOLIO

- TABLE 250. ORSTED A/S: KEY EXECUTIVES

- TABLE 251. ORSTED A/S: COMPANY SNAPSHOT

- TABLE 252. ORSTED A/S: SERVICE SEGMENTS

- TABLE 253. ORSTED A/S: PRODUCT PORTFOLIO

- TABLE 254. POET-DSM ADVANCED BIOFUELS LLC: KEY EXECUTIVES

- TABLE 255. POET-DSM ADVANCED BIOFUELS LLC: COMPANY SNAPSHOT

- TABLE 256. POET-DSM ADVANCED BIOFUELS LLC: PRODUCT SEGMENTS

- TABLE 257. POET-DSM ADVANCED BIOFUELS LLC: PRODUCT PORTFOLIO

- TABLE 258. RELIANCE INDUSTRIES LIMITED: KEY EXECUTIVES

- TABLE 259. RELIANCE INDUSTRIES LIMITED: COMPANY SNAPSHOT

- TABLE 260. RELIANCE INDUSTRIES LIMITED: PRODUCT SEGMENTS

- TABLE 261. RELIANCE INDUSTRIES LIMITED: PRODUCT PORTFOLIO

- TABLE 262. ZEA2: KEY EXECUTIVES

- TABLE 263. ZEA2: COMPANY SNAPSHOT

- TABLE 264. ZEA2: PRODUCT SEGMENTS

- TABLE 265. ZEA2: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. SECOND GENERATION BIOFUELS MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF SECOND GENERATION BIOFUELS MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN SECOND GENERATION BIOFUELS MARKET (2022 TO 2032)

- FIGURE 04. TOP INVESTMENT POCKETS IN SECOND GENERATION BIOFUELS MARKET (2023-2032)

- FIGURE 05. LOW BARGAINING POWER OF SUPPLIERS

- FIGURE 06. LOW THREAT OF NEW ENTRANTS

- FIGURE 07. LOW THREAT OF SUBSTITUTES

- FIGURE 08. LOW INTENSITY OF RIVALRY

- FIGURE 09. LOW BARGAINING POWER OF BUYERS

- FIGURE 10. GLOBAL SECOND GENERATION BIOFUELS MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. IMPACT OF KEY REGULATION: SECOND GENERATION BIOFUELS MARKET

- FIGURE 12. PRICING ANALYSIS: SECOND GENERATION BIOFUELS MARKET 2022 AND 2032

- FIGURE 13. SECOND GENERATION BIOFUELS MARKET, BY TYPE, 2022 AND 2032(%)

- FIGURE 14. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR CELLULOSIC ETHANOL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR BIODIESEL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR BIO BUTANOL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. SECOND GENERATION BIOFUELS MARKET, BY FEEDSTOCK, 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR SIMPLE LIGNOCELLULOSE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR COMPLEX LIGNOCELLULOSE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR SYNGAS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR ALGAE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. SECOND GENERATION BIOFUELS MARKET, BY PROCESS, 2022 AND 2032(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR BIOCHEMICAL PROCESS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR THERMOCHEMICAL PROCESS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 27. SECOND GENERATION BIOFUELS MARKET, BY APPLICATION, 2022 AND 2032(%)

- FIGURE 28. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR TRANSPORTATION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 29. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR POWER GENERATION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 30. COMPARATIVE SHARE ANALYSIS OF SECOND GENERATION BIOFUELS MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 31. SECOND GENERATION BIOFUELS MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 32. U.S. SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 33. CANADA SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 34. MEXICO SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 35. GERMANY SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 36. FRANCE SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 37. ITALY SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 38. SPAIN SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 39. UK SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 40. REST OF EUROPE SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 41. CHINA SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 42. JAPAN SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 43. INDIA SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 44. THAILAND SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 45. REST OF ASIA-PACIFIC SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 46. BRAZIL SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 47. SOUTH AFRICA SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 48. ISRAEL SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 49. REST OF LAMEA SECOND GENERATION BIOFUELS MARKET, 2022-2032 ($MILLION)

- FIGURE 50. TOP WINNING STRATEGIES, BY YEAR (2020-2021)

- FIGURE 51. TOP WINNING STRATEGIES, BY DEVELOPMENT (2020-2021)

- FIGURE 52. TOP WINNING STRATEGIES, BY COMPANY (2020-2021)

- FIGURE 53. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 54. COMPETITIVE DASHBOARD

- FIGURE 55. COMPETITIVE HEATMAP: SECOND GENERATION BIOFUELS MARKET

- FIGURE 56. TOP PLAYER POSITIONING, 2022

- FIGURE 57. CLARIANT AG.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 58. CLARIANT AG.: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 59. CLARIANT AG.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 60. CLARIANT AG.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 61. INTERNATIONAL FLAVORS & FRAGRANCES INC.: NET SALES, 2020-2022 ($MILLION)

- FIGURE 62. INTERNATIONAL FLAVORS & FRAGRANCES INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 63. INTERNATIONAL FLAVORS & FRAGRANCES INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 64. GRANBIO INVESTIMENTOS S.A.: NET REVENUE, 2019-2021 ($MILLION)

- FIGURE 65. GRANBIO INVESTIMENTOS S.A.: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 66. INEOS GROUP: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 67. INEOS GROUP: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 68. INEOS GROUP: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 69. ORSTED A/S: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 70. ORSTED A/S: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 71. RELIANCE INDUSTRIES LIMITED: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 72. RELIANCE INDUSTRIES LIMITED: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 73. RELIANCE INDUSTRIES LIMITED: REVENUE SHARE BY REGION, 2022 (%)