|

市場調查報告書

商品編碼

1472214

組織學和細胞學市場:按測試類型、按產品、按測試類型、按應用、按最終用戶:2023-2032 年全球機會分析和行業預測Histology and Cytology Market By Type of Examination, By Product, By Test Type, By Application, By End User : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

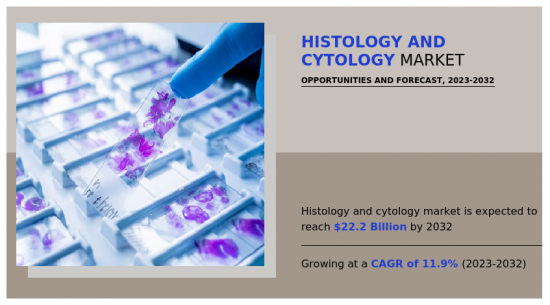

全球組織學和細胞學市場預計到2022年將達到72億美元,2023年至2032年複合年成長率為11.9%,預計到2032年將達到222億美元。

組織學和細胞學是醫療保健領域必不可少的分析技術,對於多種疾病狀態的診斷和治療管理具有重要意義。組織學涉及對組織進行顯微鏡檢查,以檢查其結構特徵並識別異常。另一方面,細胞學著重於檢查單一細胞以識別異常和疾病。這些診斷技術在及時識別癌症、感染疾病和其他病理狀況方面發揮重要作用。

癌症等慢性病盛行率的上升以及醫療基礎設施的改善預計將推動組織學和細胞學市場的成長。例如,根據美國癌症協會估計,2020年預計將有1,930萬新發癌症病例(不包括非黑色素瘤皮膚癌為1,810萬例),約有1,000萬例癌症死亡(非黑色素瘤皮膚癌)。人(不包括黑色素瘤皮膚癌)發生。癌症、心血管疾病和呼吸系統疾病等慢性疾病的顯著增加迫切需要先進的診斷和篩檢方法。

組織學和細胞學為與惡性相關的細胞和組織層面變化提供了寶貴的見解,並有助於準確診斷和製定個人化治療策略。此外,隨著世界人口持續老化,慢性病的發生率也在增加,進一步增加了對組織和細胞學用於疾病診斷的需求。

此外,醫療保健專業人員和患者意識的提高在推動組織學和細胞學檢測的需求方面發揮關鍵作用。患者越來越意識到組織學和細胞學在診斷各種醫療狀況(包括癌症和感染疾病)的重要性,導致對這些診斷技術的需求增加。此外,醫療保健專業人員也越來越意識到組織學和細胞學在提供準確和及時診斷方面的好處。醫學研究和技術的進步使醫療保健專業人員能夠了解這些診斷工具的重要性並將其納入臨床實踐。因此,醫療保健專業人員和患者意識的提高預計將推動市場成長。

此外,新興國家醫療保健基礎設施的改善預計也將推動市場成長。隨著新興國家不斷投資改善其醫療保健系統,對組織學和細胞學等先進診斷技術的需求正在迅速增加,這些技術在疾病檢測和管理中發揮關鍵作用。例如,根據國家醫學圖書館 2023 年的報告,截至 2022 會計年度,印度有超過 2,000 個公共衛生設施。醫院、診斷實驗室和研究中心等醫療保健設施的擴張和現代化正在為採用尖端的組織學和細胞學技術創建一個強大的生態系統。因此,醫療保健基礎設施的改善預計將顯著促進市場成長。

組織學和細胞學市場按測試類型、產品、測試類型、應用、最終用戶和地區進行細分。按測試類型,市場分為組織學和細胞學。依產品分類,市場分為儀器和分析軟體系統、消耗品和試劑。依測試類型,市場分為顯微鏡法、流式細胞技術和分子遺傳學方法。

相關人員的主要利益

- 該報告定量分析了 2022 年至 2032 年組織學和細胞學市場分析的細分市場、當前趨勢、估計趨勢和動態,並確定了組織學和細胞學市場的強大市場機會。

- 我們提供市場研究以及與市場促進因素、市場限制和市場機會相關的資訊。

- 波特的五力分析揭示了買方和供應商的潛力,可幫助相關人員做出以利潤為導向的業務決策並加強供應商和買方網路。

- 對組織學和細胞學市場細分的詳細分析有助於識別市場機會。

- 每個地區的主要國家都根據其對全球市場的收益貢獻繪製了地圖。

- 市場參與者定位有助於基準化分析,並提供對市場參與者當前地位的清晰了解。

- 該報告包括對區域和全球組織學和細胞學市場趨勢、主要企業、細分市場、應用領域和市場成長策略的分析。

其他好處包括:

- 季度更新(僅適用於公司許可證)

- 在購買之前或之後免費更新您選擇的 5 個額外公司簡介。

- 如果您購買 5 使用者許可證或企業使用者許可證,將免費提供下一個版本。

- 16小時分析師支援(購買後,如果在報告審核過程中發現額外資料需求,您將獲得16小時分析師支持,以解決任何問題或售後查詢)

- 15% 免費客製化(如果報告的範圍或部分不符合您的要求,15% 相當於 3 個工作日的免費工作)

- 5 個用戶許可證和企業用戶許可證的免費資料包。 (Excel版報告)

- 如果您的報告已超過 6 至 12 個月,我們將免費提供更新的報告。

- 24小時優先回應

- 免費獲取最新的行業資訊和白皮書。

- 報告客製化的可能性(請聯絡銷售人員以了解額外費用和時間表)

- 根據客戶興趣加入公司簡介

- 公司簡介的擴充列表

- 歷史市場資料

目錄

第1章簡介

第 2 章執行摘要

第3章市場概況

- 市場定義和範圍

- 主要發現

- 主要影響因素

- 關鍵投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 亞太地區製藥業的成長

- 慢性病快速增加

- 改善醫療基礎設施

- 抑制因素

- 組織學和細胞學分析設備高成本

- 機會

- 組織學和細胞學分析技術的技術進步

- 促進因素

第4章組織學/細胞學市場:依測驗類型

- 概述

- 組織學

- 細胞學

第5章組織學/細胞學市場:依產品

- 概述

- 設備/分析軟體系統

- 耗材和試劑

第6章組織學/細胞學市場:依測驗類型

- 概述

- 顯微鏡法

- 流式細胞技術儀法

- 分子遺傳學檢測方法

第7章組織學/細胞學市場:依應用分類

- 概述

- 藥物發現/藥物設計

- 臨床診斷

- 學術研究

第 8 章組織學/細胞學市場:依最終使用者分類

- 概述

- 製藥和生物技術公司

- CDMO

- 診斷實驗室

- 其他

第9章組織學/細胞學市場:按地區

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 哥倫比亞

- 阿根廷

- 其他拉丁美洲

- 中東/非洲

- GCC

- 南非

- 北非

- 其他中東/非洲

第10章競爭格局

- 介紹

- 關鍵成功策略

- 10家主要企業產品圖譜

- 競爭對手儀表板

- 競爭熱圖

- 2022年主要企業定位

第11章 公司簡介

- Hologic, Inc.

- F. Hoffmann-La Roche Ltd.

- Abbott Laboratories

- Becton, Dickinson, and Company

- Danaher Corporation

- Merck KGaA

- Thermo Fisher Scientific, Inc.

- Sysmex Corporation

- Trivitron Healthcare Private Limited

- Koninklijke Philips NV

The global histology and cytology market was valued at $7.2 billion in 2022, and is projected to reach $22.2 billion by 2032, growing at a CAGR of 11.9% from 2023 to 2032.

Histology and cytology constitute indispensable analytical techniques in the healthcare sector, holding a pivotal significance in the diagnosis and therapeutic management of diverse medical conditions. Histology entails the microscopic examination of tissues, scrutinizing their structural characteristics and identifying anomalies, whereas cytology concentrates on the examination of individual cells to identify abnormalities or diseases. These diagnostic methodologies play a critical role in the timely identification of cancer, infectious diseases, and other pathological conditions.

The rise in prevalence of chronic diseases such as cancer and the improving healthcare infrastructure is expected to drive the growth of the histology and cytology market. For instance, according to the American Cancer Society, it was reported that in 2020, Worldwide, an estimated 19.3 million new cancer cases (18.1 million excluding nonmelanoma skin cancer) and almost 10.0 million cancer deaths (9.9 million excluding nonmelanoma skin cancer) occurred in 2020. The notable increase in chronic conditions, such as cancer, cardiovascular diseases, and respiratory disorders, has created a pressing need for advanced diagnostic and screening methods.

Histology and cytology procedures provide invaluable insights into the cellular and tissue-level changes associated with malignancies, aiding in accurate diagnosis and the formulation of personalized treatment strategies. Moreover, as the aging population continues to grow worldwide, there is an inherent increase in the incidence of chronic diseases, further driving the demand for histology and cytology for disease diagnosis.

In addition, surge in awareness among healthcare professionals and patients plays a crucial role in driving the demand for histological and cytological examinations, as individuals become more proactive in managing their health and seeking early detection of diseases. Patients increasingly recognize the importance of histology and cytology in diagnosing various medical conditions, including cancers and infectious diseases, which has led to a rising demand for these diagnostic technologies. Moreover, healthcare professionals have become more aware of the benefits of histology and cytology in providing accurate and timely diagnoses. With advancements in medical research and technology, healthcare professionals are better equipped to understand the significance of these diagnostic tools and incorporate them into their clinical practices. Thus, the rise in awareness among the healthcare professionals and patients is expected to drive the growth of the market.

Furthermore, the improving healthcare infrastructure in developing countries is expected to drive the growth of the market. As countries across the developing regions progressively invest in upgrading their healthcare systems, there is a surge in demand for advanced diagnostic techniques, such as histology and cytology, which play a crucial role in disease detection and management. For instance, according to the 2023 report by National Library of Medicine, it was reported that over two lakh public health facilities were reported in India as of the financial year 2022. The expansion and modernization of healthcare facilities, including hospitals, diagnostic laboratories, and research centers, are creating a robust ecosystem for the adoption of cutting-edge histology and cytology technologies. Thus, the improving healthcare infrastructure is expected to significantly contribute to the growth of the market.

The histology and cytology market is segmented on the basis of type of examination, product, test type, application, end user, and region. On the basis of type of examination, the market is bifurcated into histology and cytology. On the basis of product, the market is classified into instruments and analysis software system and consumable and reagents. On the basis of test type, the market is divided into microscopy methods, flow cytometry, and molecular genetic methods.

On the basis of application, the market is segregated into drug discovery and designing, clinical diagnostics, and academic research. On the basis of end user, the market is fragmented into pharma & biotech companies, CDMO, diagnostic laboratories, and others. Others include hospital and academic research. Region wise, the market is analyzed across North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa. Major key players that operate in the histology and cytology market are Hologic, Inc., F. Hoffmann-La Roche Ltd., Abbott Laboratories, Becton, Dickinson and Company, Danaher Corporation, Merck KGaA, Thermo Fisher Scientific, Inc., Sysmex Corporation, Trivitron Healthcare Private Limited, and Koninklijke Philips N.V.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the histology and cytology market analysis from 2022 to 2032 to identify the prevailing histology and cytology market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the histology and cytology market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global histology and cytology market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

- Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Additional company profiles with specific to client's interest

- Expanded list for Company Profiles

- Historic market data

Key Market Segments

By Type of Examination

- Histology

- Cytology

By Product

- Instruments and Analysis Software System

- Consumable and Reagents

By Test Type

- Microscopy Methods

- Flow Cytometry

- Molecular Genetic Methods

By Application

- Drug Discovery and Designing

- Clinical Diagnostics

- Academic Research

By End User

- Pharma and Biotech Companies

- CDMO

- Diagnostic Laboratories

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Latin America

- Brazil

- Colombia

- Argentina

- Rest of Latin America

- Middle East and Africa

- Gcc

- South Africa

- North Africa

- Rest Of Mea

Key Market Players:

- Abbott Laboratories

- Merck KGaA

- Thermo Fisher Scientific, Inc.

- Trivitron Healthcare Private Limited

- Koninklijke Philips N.V.

- F. Hoffmann-La Roche Ltd.

- Danaher Corporation

- Sysmex Corporation

- Becton, Dickinson, and Company

- Hologic, Inc.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Low bargaining power of suppliers

- 3.3.2. Low threat of new entrants

- 3.3.3. Low threat of substitutes

- 3.3.4. Low intensity of rivalry

- 3.3.5. Low bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Growing Pharmaceutical Industry in Asia Pacific Region.

- 3.4.1.2. Surge in prevalence of chronic diseases.

- 3.4.1.3. Improving Healthcare Infrastructure.

- 3.4.2. Restraints

- 3.4.2.1. High cost of histological and cytological analytical instruments.

- 3.4.3. Opportunities

- 3.4.3.1. Technological advancement in the histological and cytological analysis technology.

- 3.4.1. Drivers

CHAPTER 4: HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Histology

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Cytology

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

CHAPTER 5: HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Instruments and Analysis Software System

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Consumable and Reagents

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

CHAPTER 6: HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Microscopy Methods

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Flow Cytometry

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Molecular Genetic Methods

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION

- 7.1. Overview

- 7.1.1. Market size and forecast

- 7.2. Drug Discovery and Designing

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by region

- 7.2.3. Market share analysis by country

- 7.3. Clinical Diagnostics

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by region

- 7.3.3. Market share analysis by country

- 7.4. Academic Research

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by region

- 7.4.3. Market share analysis by country

CHAPTER 8: HISTOLOGY AND CYTOLOGY MARKET, BY END USER

- 8.1. Overview

- 8.1.1. Market size and forecast

- 8.2. Pharma and Biotech Companies

- 8.2.1. Key market trends, growth factors and opportunities

- 8.2.2. Market size and forecast, by region

- 8.2.3. Market share analysis by country

- 8.3. CDMO

- 8.3.1. Key market trends, growth factors and opportunities

- 8.3.2. Market size and forecast, by region

- 8.3.3. Market share analysis by country

- 8.4. Diagnostic Laboratories

- 8.4.1. Key market trends, growth factors and opportunities

- 8.4.2. Market size and forecast, by region

- 8.4.3. Market share analysis by country

- 8.5. Others

- 8.5.1. Key market trends, growth factors and opportunities

- 8.5.2. Market size and forecast, by region

- 8.5.3. Market share analysis by country

CHAPTER 9: HISTOLOGY AND CYTOLOGY MARKET, BY REGION

- 9.1. Overview

- 9.1.1. Market size and forecast By Region

- 9.2. North America

- 9.2.1. Key market trends, growth factors and opportunities

- 9.2.2. Market size and forecast, by Type of Examination

- 9.2.3. Market size and forecast, by Product

- 9.2.4. Market size and forecast, by Test Type

- 9.2.5. Market size and forecast, by Application

- 9.2.6. Market size and forecast, by End User

- 9.2.7. Market size and forecast, by country

- 9.2.7.1. U.S.

- 9.2.7.1.1. Market size and forecast, by Type of Examination

- 9.2.7.1.2. Market size and forecast, by Product

- 9.2.7.1.3. Market size and forecast, by Test Type

- 9.2.7.1.4. Market size and forecast, by Application

- 9.2.7.1.5. Market size and forecast, by End User

- 9.2.7.2. Canada

- 9.2.7.2.1. Market size and forecast, by Type of Examination

- 9.2.7.2.2. Market size and forecast, by Product

- 9.2.7.2.3. Market size and forecast, by Test Type

- 9.2.7.2.4. Market size and forecast, by Application

- 9.2.7.2.5. Market size and forecast, by End User

- 9.2.7.3. Mexico

- 9.2.7.3.1. Market size and forecast, by Type of Examination

- 9.2.7.3.2. Market size and forecast, by Product

- 9.2.7.3.3. Market size and forecast, by Test Type

- 9.2.7.3.4. Market size and forecast, by Application

- 9.2.7.3.5. Market size and forecast, by End User

- 9.3. Europe

- 9.3.1. Key market trends, growth factors and opportunities

- 9.3.2. Market size and forecast, by Type of Examination

- 9.3.3. Market size and forecast, by Product

- 9.3.4. Market size and forecast, by Test Type

- 9.3.5. Market size and forecast, by Application

- 9.3.6. Market size and forecast, by End User

- 9.3.7. Market size and forecast, by country

- 9.3.7.1. Germany

- 9.3.7.1.1. Market size and forecast, by Type of Examination

- 9.3.7.1.2. Market size and forecast, by Product

- 9.3.7.1.3. Market size and forecast, by Test Type

- 9.3.7.1.4. Market size and forecast, by Application

- 9.3.7.1.5. Market size and forecast, by End User

- 9.3.7.2. France

- 9.3.7.2.1. Market size and forecast, by Type of Examination

- 9.3.7.2.2. Market size and forecast, by Product

- 9.3.7.2.3. Market size and forecast, by Test Type

- 9.3.7.2.4. Market size and forecast, by Application

- 9.3.7.2.5. Market size and forecast, by End User

- 9.3.7.3. UK

- 9.3.7.3.1. Market size and forecast, by Type of Examination

- 9.3.7.3.2. Market size and forecast, by Product

- 9.3.7.3.3. Market size and forecast, by Test Type

- 9.3.7.3.4. Market size and forecast, by Application

- 9.3.7.3.5. Market size and forecast, by End User

- 9.3.7.4. Italy

- 9.3.7.4.1. Market size and forecast, by Type of Examination

- 9.3.7.4.2. Market size and forecast, by Product

- 9.3.7.4.3. Market size and forecast, by Test Type

- 9.3.7.4.4. Market size and forecast, by Application

- 9.3.7.4.5. Market size and forecast, by End User

- 9.3.7.5. Spain

- 9.3.7.5.1. Market size and forecast, by Type of Examination

- 9.3.7.5.2. Market size and forecast, by Product

- 9.3.7.5.3. Market size and forecast, by Test Type

- 9.3.7.5.4. Market size and forecast, by Application

- 9.3.7.5.5. Market size and forecast, by End User

- 9.3.7.6. Rest of Europe

- 9.3.7.6.1. Market size and forecast, by Type of Examination

- 9.3.7.6.2. Market size and forecast, by Product

- 9.3.7.6.3. Market size and forecast, by Test Type

- 9.3.7.6.4. Market size and forecast, by Application

- 9.3.7.6.5. Market size and forecast, by End User

- 9.4. Asia-Pacific

- 9.4.1. Key market trends, growth factors and opportunities

- 9.4.2. Market size and forecast, by Type of Examination

- 9.4.3. Market size and forecast, by Product

- 9.4.4. Market size and forecast, by Test Type

- 9.4.5. Market size and forecast, by Application

- 9.4.6. Market size and forecast, by End User

- 9.4.7. Market size and forecast, by country

- 9.4.7.1. Japan

- 9.4.7.1.1. Market size and forecast, by Type of Examination

- 9.4.7.1.2. Market size and forecast, by Product

- 9.4.7.1.3. Market size and forecast, by Test Type

- 9.4.7.1.4. Market size and forecast, by Application

- 9.4.7.1.5. Market size and forecast, by End User

- 9.4.7.2. China

- 9.4.7.2.1. Market size and forecast, by Type of Examination

- 9.4.7.2.2. Market size and forecast, by Product

- 9.4.7.2.3. Market size and forecast, by Test Type

- 9.4.7.2.4. Market size and forecast, by Application

- 9.4.7.2.5. Market size and forecast, by End User

- 9.4.7.3. India

- 9.4.7.3.1. Market size and forecast, by Type of Examination

- 9.4.7.3.2. Market size and forecast, by Product

- 9.4.7.3.3. Market size and forecast, by Test Type

- 9.4.7.3.4. Market size and forecast, by Application

- 9.4.7.3.5. Market size and forecast, by End User

- 9.4.7.4. Australia

- 9.4.7.4.1. Market size and forecast, by Type of Examination

- 9.4.7.4.2. Market size and forecast, by Product

- 9.4.7.4.3. Market size and forecast, by Test Type

- 9.4.7.4.4. Market size and forecast, by Application

- 9.4.7.4.5. Market size and forecast, by End User

- 9.4.7.5. South Korea

- 9.4.7.5.1. Market size and forecast, by Type of Examination

- 9.4.7.5.2. Market size and forecast, by Product

- 9.4.7.5.3. Market size and forecast, by Test Type

- 9.4.7.5.4. Market size and forecast, by Application

- 9.4.7.5.5. Market size and forecast, by End User

- 9.4.7.6. Rest of Asia-Pacific

- 9.4.7.6.1. Market size and forecast, by Type of Examination

- 9.4.7.6.2. Market size and forecast, by Product

- 9.4.7.6.3. Market size and forecast, by Test Type

- 9.4.7.6.4. Market size and forecast, by Application

- 9.4.7.6.5. Market size and forecast, by End User

- 9.5. Latin America

- 9.5.1. Key market trends, growth factors and opportunities

- 9.5.2. Market size and forecast, by Type of Examination

- 9.5.3. Market size and forecast, by Product

- 9.5.4. Market size and forecast, by Test Type

- 9.5.5. Market size and forecast, by Application

- 9.5.6. Market size and forecast, by End User

- 9.5.7. Market size and forecast, by country

- 9.5.7.1. Brazil

- 9.5.7.1.1. Market size and forecast, by Type of Examination

- 9.5.7.1.2. Market size and forecast, by Product

- 9.5.7.1.3. Market size and forecast, by Test Type

- 9.5.7.1.4. Market size and forecast, by Application

- 9.5.7.1.5. Market size and forecast, by End User

- 9.5.7.2. Colombia

- 9.5.7.2.1. Market size and forecast, by Type of Examination

- 9.5.7.2.2. Market size and forecast, by Product

- 9.5.7.2.3. Market size and forecast, by Test Type

- 9.5.7.2.4. Market size and forecast, by Application

- 9.5.7.2.5. Market size and forecast, by End User

- 9.5.7.3. Argentina

- 9.5.7.3.1. Market size and forecast, by Type of Examination

- 9.5.7.3.2. Market size and forecast, by Product

- 9.5.7.3.3. Market size and forecast, by Test Type

- 9.5.7.3.4. Market size and forecast, by Application

- 9.5.7.3.5. Market size and forecast, by End User

- 9.5.7.4. Rest of Latin America

- 9.5.7.4.1. Market size and forecast, by Type of Examination

- 9.5.7.4.2. Market size and forecast, by Product

- 9.5.7.4.3. Market size and forecast, by Test Type

- 9.5.7.4.4. Market size and forecast, by Application

- 9.5.7.4.5. Market size and forecast, by End User

- 9.6. Middle East and Africa

- 9.6.1. Key market trends, growth factors and opportunities

- 9.6.2. Market size and forecast, by Type of Examination

- 9.6.3. Market size and forecast, by Product

- 9.6.4. Market size and forecast, by Test Type

- 9.6.5. Market size and forecast, by Application

- 9.6.6. Market size and forecast, by End User

- 9.6.7. Market size and forecast, by country

- 9.6.7.1. Gcc

- 9.6.7.1.1. Market size and forecast, by Type of Examination

- 9.6.7.1.2. Market size and forecast, by Product

- 9.6.7.1.3. Market size and forecast, by Test Type

- 9.6.7.1.4. Market size and forecast, by Application

- 9.6.7.1.5. Market size and forecast, by End User

- 9.6.7.2. South Africa

- 9.6.7.2.1. Market size and forecast, by Type of Examination

- 9.6.7.2.2. Market size and forecast, by Product

- 9.6.7.2.3. Market size and forecast, by Test Type

- 9.6.7.2.4. Market size and forecast, by Application

- 9.6.7.2.5. Market size and forecast, by End User

- 9.6.7.3. North Africa

- 9.6.7.3.1. Market size and forecast, by Type of Examination

- 9.6.7.3.2. Market size and forecast, by Product

- 9.6.7.3.3. Market size and forecast, by Test Type

- 9.6.7.3.4. Market size and forecast, by Application

- 9.6.7.3.5. Market size and forecast, by End User

- 9.6.7.4. Rest Of Mea

- 9.6.7.4.1. Market size and forecast, by Type of Examination

- 9.6.7.4.2. Market size and forecast, by Product

- 9.6.7.4.3. Market size and forecast, by Test Type

- 9.6.7.4.4. Market size and forecast, by Application

- 9.6.7.4.5. Market size and forecast, by End User

CHAPTER 10: COMPETITIVE LANDSCAPE

- 10.1. Introduction

- 10.2. Top winning strategies

- 10.3. Product mapping of top 10 player

- 10.4. Competitive dashboard

- 10.5. Competitive heatmap

- 10.6. Top player positioning, 2022

CHAPTER 11: COMPANY PROFILES

- 11.1. Hologic, Inc.

- 11.1.1. Company overview

- 11.1.2. Key executives

- 11.1.3. Company snapshot

- 11.1.4. Operating business segments

- 11.1.5. Product portfolio

- 11.1.6. Business performance

- 11.2. F. Hoffmann-La Roche Ltd.

- 11.2.1. Company overview

- 11.2.2. Key executives

- 11.2.3. Company snapshot

- 11.2.4. Operating business segments

- 11.2.5. Product portfolio

- 11.2.6. Business performance

- 11.2.7. Key strategic moves and developments

- 11.3. Abbott Laboratories

- 11.3.1. Company overview

- 11.3.2. Key executives

- 11.3.3. Company snapshot

- 11.3.4. Operating business segments

- 11.3.5. Product portfolio

- 11.3.6. Business performance

- 11.4. Becton, Dickinson, and Company

- 11.4.1. Company overview

- 11.4.2. Key executives

- 11.4.3. Company snapshot

- 11.4.4. Operating business segments

- 11.4.5. Product portfolio

- 11.4.6. Business performance

- 11.4.7. Key strategic moves and developments

- 11.5. Danaher Corporation

- 11.5.1. Company overview

- 11.5.2. Key executives

- 11.5.3. Company snapshot

- 11.5.4. Operating business segments

- 11.5.5. Product portfolio

- 11.5.6. Business performance

- 11.6. Merck KGaA

- 11.6.1. Company overview

- 11.6.2. Key executives

- 11.6.3. Company snapshot

- 11.6.4. Operating business segments

- 11.6.5. Product portfolio

- 11.6.6. Business performance

- 11.7. Thermo Fisher Scientific, Inc.

- 11.7.1. Company overview

- 11.7.2. Key executives

- 11.7.3. Company snapshot

- 11.7.4. Operating business segments

- 11.7.5. Product portfolio

- 11.7.6. Business performance

- 11.8. Sysmex Corporation

- 11.8.1. Company overview

- 11.8.2. Key executives

- 11.8.3. Company snapshot

- 11.8.4. Operating business segments

- 11.8.5. Product portfolio

- 11.8.6. Business performance

- 11.9. Trivitron Healthcare Private Limited

- 11.9.1. Company overview

- 11.9.2. Key executives

- 11.9.3. Company snapshot

- 11.9.4. Operating business segments

- 11.9.5. Product portfolio

- 11.10. Koninklijke Philips N.V.

- 11.10.1. Company overview

- 11.10.2. Key executives

- 11.10.3. Company snapshot

- 11.10.4. Operating business segments

- 11.10.5. Product portfolio

- 11.10.6. Business performance

LIST OF TABLES

- TABLE 01. GLOBAL HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 02. HISTOLOGY AND CYTOLOGY MARKET FOR HISTOLOGY, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. HISTOLOGY AND CYTOLOGY MARKET FOR CYTOLOGY, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. GLOBAL HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 05. HISTOLOGY AND CYTOLOGY MARKET FOR INSTRUMENTS AND ANALYSIS SOFTWARE SYSTEM, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. HISTOLOGY AND CYTOLOGY MARKET FOR CONSUMABLE AND REAGENTS, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. GLOBAL HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 08. HISTOLOGY AND CYTOLOGY MARKET FOR MICROSCOPY METHODS, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. HISTOLOGY AND CYTOLOGY MARKET FOR FLOW CYTOMETRY, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. HISTOLOGY AND CYTOLOGY MARKET FOR MOLECULAR GENETIC METHODS, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. GLOBAL HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 12. HISTOLOGY AND CYTOLOGY MARKET FOR DRUG DISCOVERY AND DESIGNING, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. HISTOLOGY AND CYTOLOGY MARKET FOR CLINICAL DIAGNOSTICS, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. HISTOLOGY AND CYTOLOGY MARKET FOR ACADEMIC RESEARCH, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. GLOBAL HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 16. HISTOLOGY AND CYTOLOGY MARKET FOR PHARMA AND BIOTECH COMPANIES, BY REGION, 2022-2032 ($MILLION)

- TABLE 17. HISTOLOGY AND CYTOLOGY MARKET FOR CDMO, BY REGION, 2022-2032 ($MILLION)

- TABLE 18. HISTOLOGY AND CYTOLOGY MARKET FOR DIAGNOSTIC LABORATORIES, BY REGION, 2022-2032 ($MILLION)

- TABLE 19. HISTOLOGY AND CYTOLOGY MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 20. HISTOLOGY AND CYTOLOGY MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 21. NORTH AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 22. NORTH AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 23. NORTH AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 24. NORTH AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 25. NORTH AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 26. NORTH AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 27. U.S. HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 28. U.S. HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 29. U.S. HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 30. U.S. HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 31. U.S. HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 32. CANADA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 33. CANADA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 34. CANADA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 35. CANADA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 36. CANADA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 37. MEXICO HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 38. MEXICO HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 39. MEXICO HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 40. MEXICO HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 41. MEXICO HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 42. EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 43. EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 44. EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 45. EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 46. EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 47. EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 48. GERMANY HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 49. GERMANY HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 50. GERMANY HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 51. GERMANY HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 52. GERMANY HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 53. FRANCE HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 54. FRANCE HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 55. FRANCE HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 56. FRANCE HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 57. FRANCE HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 58. UK HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 59. UK HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 60. UK HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 61. UK HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 62. UK HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 63. ITALY HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 64. ITALY HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 65. ITALY HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 66. ITALY HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 67. ITALY HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 68. SPAIN HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 69. SPAIN HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 70. SPAIN HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 71. SPAIN HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 72. SPAIN HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 73. REST OF EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 74. REST OF EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 75. REST OF EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 76. REST OF EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 77. REST OF EUROPE HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 78. ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 79. ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 80. ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 81. ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 82. ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 83. ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 84. JAPAN HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 85. JAPAN HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 86. JAPAN HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 87. JAPAN HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 88. JAPAN HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 89. CHINA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 90. CHINA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 91. CHINA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 92. CHINA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 93. CHINA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 94. INDIA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 95. INDIA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 96. INDIA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 97. INDIA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 98. INDIA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 99. AUSTRALIA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 100. AUSTRALIA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 101. AUSTRALIA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 102. AUSTRALIA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 103. AUSTRALIA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 104. SOUTH KOREA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 105. SOUTH KOREA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 106. SOUTH KOREA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 107. SOUTH KOREA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 108. SOUTH KOREA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 109. REST OF ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 110. REST OF ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 111. REST OF ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 112. REST OF ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 113. REST OF ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 114. LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 115. LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 116. LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 117. LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 118. LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 119. LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 120. BRAZIL HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 121. BRAZIL HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 122. BRAZIL HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 123. BRAZIL HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 124. BRAZIL HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 125. COLOMBIA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 126. COLOMBIA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 127. COLOMBIA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 128. COLOMBIA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 129. COLOMBIA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 130. ARGENTINA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 131. ARGENTINA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 132. ARGENTINA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 133. ARGENTINA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 134. ARGENTINA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 135. REST OF LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 136. REST OF LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 137. REST OF LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 138. REST OF LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 139. REST OF LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 140. MIDDLE EAST AND AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 141. MIDDLE EAST AND AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 142. MIDDLE EAST AND AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 143. MIDDLE EAST AND AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 144. MIDDLE EAST AND AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 145. MIDDLE EAST AND AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 146. GCC HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 147. GCC HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 148. GCC HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 149. GCC HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 150. GCC HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 151. SOUTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 152. SOUTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 153. SOUTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 154. SOUTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 155. SOUTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 156. NORTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 157. NORTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 158. NORTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 159. NORTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 160. NORTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 161. REST OF MEA HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022-2032 ($MILLION)

- TABLE 162. REST OF MEA HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 163. REST OF MEA HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022-2032 ($MILLION)

- TABLE 164. REST OF MEA HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 165. REST OF MEA HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 166. HOLOGIC, INC.: KEY EXECUTIVES

- TABLE 167. HOLOGIC, INC.: COMPANY SNAPSHOT

- TABLE 168. HOLOGIC, INC.: PRODUCT SEGMENTS

- TABLE 169. HOLOGIC, INC.: PRODUCT PORTFOLIO

- TABLE 170. F. HOFFMANN-LA ROCHE LTD.: KEY EXECUTIVES

- TABLE 171. F. HOFFMANN-LA ROCHE LTD.: COMPANY SNAPSHOT

- TABLE 172. F. HOFFMANN-LA ROCHE LTD.: PRODUCT SEGMENTS

- TABLE 173. F. HOFFMANN-LA ROCHE LTD.: PRODUCT PORTFOLIO

- TABLE 174. F. HOFFMANN-LA ROCHE LTD.: KEY STRATERGIES

- TABLE 175. ABBOTT LABORATORIES: KEY EXECUTIVES

- TABLE 176. ABBOTT LABORATORIES: COMPANY SNAPSHOT

- TABLE 177. ABBOTT LABORATORIES: PRODUCT SEGMENTS

- TABLE 178. ABBOTT LABORATORIES: PRODUCT PORTFOLIO

- TABLE 179. BECTON, DICKINSON, AND COMPANY: KEY EXECUTIVES

- TABLE 180. BECTON, DICKINSON, AND COMPANY: COMPANY SNAPSHOT

- TABLE 181. BECTON, DICKINSON, AND COMPANY: PRODUCT SEGMENTS

- TABLE 182. BECTON, DICKINSON, AND COMPANY: PRODUCT PORTFOLIO

- TABLE 183. BECTON, DICKINSON, AND COMPANY: KEY STRATERGIES

- TABLE 184. DANAHER CORPORATION: KEY EXECUTIVES

- TABLE 185. DANAHER CORPORATION: COMPANY SNAPSHOT

- TABLE 186. DANAHER CORPORATION: PRODUCT SEGMENTS

- TABLE 187. DANAHER CORPORATION: PRODUCT PORTFOLIO

- TABLE 188. MERCK KGAA: KEY EXECUTIVES

- TABLE 189. MERCK KGAA: COMPANY SNAPSHOT

- TABLE 190. MERCK KGAA: PRODUCT SEGMENTS

- TABLE 191. MERCK KGAA: PRODUCT PORTFOLIO

- TABLE 192. THERMO FISHER SCIENTIFIC, INC.: KEY EXECUTIVES

- TABLE 193. THERMO FISHER SCIENTIFIC, INC.: COMPANY SNAPSHOT

- TABLE 194. THERMO FISHER SCIENTIFIC, INC.: PRODUCT SEGMENTS

- TABLE 195. THERMO FISHER SCIENTIFIC, INC.: PRODUCT PORTFOLIO

- TABLE 196. SYSMEX CORPORATION: KEY EXECUTIVES

- TABLE 197. SYSMEX CORPORATION: COMPANY SNAPSHOT

- TABLE 198. SYSMEX CORPORATION: PRODUCT SEGMENTS

- TABLE 199. SYSMEX CORPORATION: PRODUCT PORTFOLIO

- TABLE 200. TRIVITRON HEALTHCARE PRIVATE LIMITED: KEY EXECUTIVES

- TABLE 201. TRIVITRON HEALTHCARE PRIVATE LIMITED: COMPANY SNAPSHOT

- TABLE 202. TRIVITRON HEALTHCARE PRIVATE LIMITED: PRODUCT SEGMENTS

- TABLE 203. TRIVITRON HEALTHCARE PRIVATE LIMITED: PRODUCT PORTFOLIO

- TABLE 204. KONINKLIJKE PHILIPS N.V.: KEY EXECUTIVES

- TABLE 205. KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT

- TABLE 206. KONINKLIJKE PHILIPS N.V.: SERVICE SEGMENTS

- TABLE 207. KONINKLIJKE PHILIPS N.V.: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. HISTOLOGY AND CYTOLOGY MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF HISTOLOGY AND CYTOLOGY MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN HISTOLOGY AND CYTOLOGY MARKET (2022 TO 2032)

- FIGURE 04. TOP INVESTMENT POCKETS IN HISTOLOGY AND CYTOLOGY MARKET (2023-2032)

- FIGURE 05. LOW BARGAINING POWER OF SUPPLIERS

- FIGURE 06. LOW THREAT OF NEW ENTRANTS

- FIGURE 07. LOW THREAT OF SUBSTITUTES

- FIGURE 08. LOW INTENSITY OF RIVALRY

- FIGURE 09. LOW BARGAINING POWER OF BUYERS

- FIGURE 10. GLOBAL HISTOLOGY AND CYTOLOGY MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. HISTOLOGY AND CYTOLOGY MARKET, BY TYPE OF EXAMINATION, 2022 AND 2032(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR HISTOLOGY, BY COUNTRY 2022 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR CYTOLOGY, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. HISTOLOGY AND CYTOLOGY MARKET, BY PRODUCT, 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR INSTRUMENTS AND ANALYSIS SOFTWARE SYSTEM, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR CONSUMABLE AND REAGENTS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. HISTOLOGY AND CYTOLOGY MARKET, BY TEST TYPE, 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR MICROSCOPY METHODS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR FLOW CYTOMETRY, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR MOLECULAR GENETIC METHODS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. HISTOLOGY AND CYTOLOGY MARKET, BY APPLICATION, 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR DRUG DISCOVERY AND DESIGNING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR CLINICAL DIAGNOSTICS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR ACADEMIC RESEARCH, BY COUNTRY 2022 AND 2032(%)

- FIGURE 25. HISTOLOGY AND CYTOLOGY MARKET, BY END USER, 2022 AND 2032(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR PHARMA AND BIOTECH COMPANIES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 27. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR CDMO, BY COUNTRY 2022 AND 2032(%)

- FIGURE 28. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR DIAGNOSTIC LABORATORIES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 29. COMPARATIVE SHARE ANALYSIS OF HISTOLOGY AND CYTOLOGY MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 30. HISTOLOGY AND CYTOLOGY MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 31. U.S. HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 32. CANADA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 33. MEXICO HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 34. GERMANY HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 35. FRANCE HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 36. UK HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 37. ITALY HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 38. SPAIN HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 39. REST OF EUROPE HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 40. JAPAN HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 41. CHINA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 42. INDIA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 43. AUSTRALIA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 44. SOUTH KOREA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 45. REST OF ASIA-PACIFIC HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 46. BRAZIL HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 47. COLOMBIA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 48. ARGENTINA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 49. REST OF LATIN AMERICA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 50. GCC HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 51. SOUTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 52. NORTH AFRICA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 53. REST OF MEA HISTOLOGY AND CYTOLOGY MARKET, 2022-2032 ($MILLION)

- FIGURE 54. TOP WINNING STRATEGIES, BY YEAR (2021-2023)

- FIGURE 55. TOP WINNING STRATEGIES, BY DEVELOPMENT (2021-2023)

- FIGURE 56. TOP WINNING STRATEGIES, BY COMPANY (2021-2023)

- FIGURE 57. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 58. COMPETITIVE DASHBOARD

- FIGURE 59. COMPETITIVE HEATMAP: HISTOLOGY AND CYTOLOGY MARKET

- FIGURE 60. TOP PLAYER POSITIONING, 2022

- FIGURE 61. HOLOGIC, INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 62. HOLOGIC, INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 63. HOLOGIC, INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 64. F. HOFFMANN-LA ROCHE LTD.: SALES REVENUE, 2020-2022 ($MILLION)

- FIGURE 65. F. HOFFMANN-LA ROCHE LTD.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 66. ABBOTT LABORATORIES: NET SALES, 2020-2022 ($MILLION)

- FIGURE 67. ABBOTT LABORATORIES: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 68. ABBOTT LABORATORIES: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 69. BECTON, DICKINSON, AND COMPANY: NET REVENUE, 2021-2023 ($MILLION)

- FIGURE 70. BECTON, DICKINSON, AND COMPANY: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 71. BECTON, DICKINSON, AND COMPANY: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 72. DANAHER CORPORATION: NET SALES, 2020-2022 ($MILLION)

- FIGURE 73. DANAHER CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 74. DANAHER CORPORATION: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 75. MERCK KGAA: NET SALES, 2020-2022 ($MILLION)

- FIGURE 76. MERCK KGAA: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 77. MERCK KGAA: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 78. THERMO FISHER SCIENTIFIC, INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 79. THERMO FISHER SCIENTIFIC, INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 80. THERMO FISHER SCIENTIFIC, INC.: REVENUE SHARE BY REGION, 2021 (%)

- FIGURE 81. SYSMEX CORPORATION: NET REVENUE, 2021-2023 ($MILLION)

- FIGURE 82. SYSMEX CORPORATION: REVENUE SHARE BY REGION, 2023 (%)

- FIGURE 83. KONINKLIJKE PHILIPS N.V.: NET SALES, 2020-2022 ($MILLION)

- FIGURE 84. KONINKLIJKE PHILIPS N.V.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 85. KONINKLIJKE PHILIPS N.V.: REVENUE SHARE BY REGION, 2022 (%)

組織學和細胞學市場:按測試類型、按應用、按產品類型、按測試類型、按最終用途、按地區

組織學和細胞學市場:按測試類型、按應用、按產品類型、按測試類型、按最終用途、按地區 組織學/細胞學市場:按測試類型、產品類型、測試類型、最終用戶 - 2025-2030 年全球預測

組織學/細胞學市場:按測試類型、產品類型、測試類型、最終用戶 - 2025-2030 年全球預測 組織學和細胞學市場,按類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測2024-2032 年組織學和細胞學市場報告(按產品、檢查類型、測試類型、應用和地區)

組織學和細胞學市場,按類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測2024-2032 年組織學和細胞學市場報告(按產品、檢查類型、測試類型、應用和地區) 組織學與細胞學 IVD 市場:2024 年組織學與細胞學市場報告:2030 年趨勢、預測與競爭分析

組織學與細胞學 IVD 市場:2024 年組織學與細胞學市場報告:2030 年趨勢、預測與競爭分析 組織學與細胞學市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按檢查類型、按產品、按應用、按地區、按競爭細分

組織學與細胞學市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按檢查類型、按產品、按應用、按地區、按競爭細分