|

市場調查報告書

商品編碼

1513347

流量計市場:按類型、最終用戶分類:2024-2033 年全球機會分析與產業預測Flow Meter Market By Type, By End User : Global Opportunity Analysis and Industry Forecast, 2024-2033 |

||||||

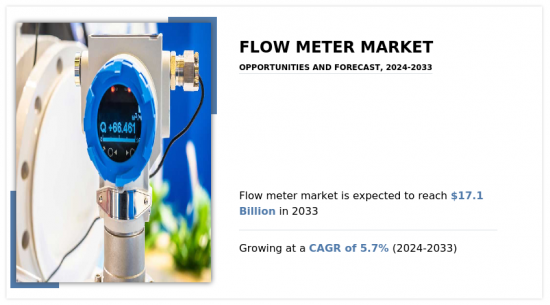

2023年流量計市值為99億美元,預計2033年將達到171億美元,2024年至2033年的複合年成長率為5.7%。

母市場概覽

流量計市場衍生工業自動化和儀器領域,其中包括旨在控制、監控和最佳化工業製程的各種設備、系統和解決方案。這個廣泛的市場包括控制系統(PLC、SCADA、DCS)、各種類型的儀器(感測器、變換器、流量計等儀表)、自動化軟體和機器人等技術。這些組件對於提高從製造到能源、製藥到用水和污水管理等眾多行業的生產力、效率和準確性至關重要。

主要市場促進因素包括對業務效率和生產力日益成長的需求、物聯網、人工智慧和機器人技術的進步,以及需要先進監控技術的嚴格環境和安全法規。人們越來越關注永續性和能源效率,進一步推動了自動化技術的採用。然而,高昂的初始投資成本、整合新系統的複雜性以及缺乏技術純熟勞工等挑戰正在阻礙市場成長。

介紹

流量計市場包括各種旨在測量通過管道的液體、氣體或蒸氣的流量或體積的設備。流量計是各種行業中極為重要的組件,包括用水和污水管理、石油和天然氣、化學品、發電、製藥和食品加工。這些設備對於確保許多工業製程的準確性、效率、安全性和法規遵循至關重要。

流量計有多種類型,包括差動流量計、容積式流量計、渦輪流量計、超音波、電磁流量計和科氏流量計,每種流量計都適合特定的應用,並具有獨特的操作優勢。使用者或公司選擇流量計取決於多種因素,包括流體特性、所需的精度、安裝環境和成本考量。

市場動態

流量計的技術進步,如智慧流量計和超音波流量計的發展,擴大了其應用範圍,提高了其精度和可靠性。這些進步透過提供更好的資料整合功能和減少維護要求,增加了流量計在各個行業的吸引力。隨著工業界對自動化和精確製程控制的關注,先進的流量計變得越來越重要。這些創新提高了業務效率,有助於長期節省成本,鼓勵更多公司採用這些先進技術。全球嚴格的環境法規迫使工業界更密切地監控和減少排放和資源使用。流量計是滿足這些監管要求的關鍵工具,因為它們可以準確測量氣體、液體和蒸氣的流量。這些監管壓力使得流量計在製造、發電和化學加工等行業中變得至關重要,在這些行業中,準確的測量是最大限度地減少環境足跡和避免巨額罰款的關鍵。

景氣衰退對新技術和設備(包括流量計)的投資有重大影響。在景氣衰退和經濟不穩定時期,產業往往會減少資本支出以節省資源,直接影響先進流量計等非必需的高成本設備的銷售。石油和天然氣等週期性較強的行業預計將推遲或減少儀器基礎設施升級的投資。經濟狀況導致的支出下降成為流量計市場的限制因素,在經濟狀況改善之前減緩其成長。

由於快速的工業化、都市化和基礎設施發展的投資,新興市場為流量計市場提供了巨大的成長機會。亞太、非洲和拉丁美洲國家正在增加對用水和污水管理、石油和天然氣以及能源等領域的投資,這些領域需要廣泛使用流量計。隨著這些經濟體的不斷發展,對流量計量解決方案的需求預計將增加,為製造商擴大其地理覆蓋範圍和提高市場滲透率提供有利可圖的機會。

由於對永續能源實踐的日益重視,可再生能源產業正在全球範圍內經歷顯著成長。流量計在可再生能源生產的操作過程中發揮重要作用,例如生質燃料生產、地熱能和太陽能熱能系統。它確保效率和監控系統性能的能力對於最佳化能源輸出和減少浪費至關重要。因此,不斷擴大的可再生能源領域為流量計帶來了不斷成長的市場。因為這些設備有助於滿足永續能源應用中特定產業對準確性和可靠性的需求。

專利分析-2023

2023年流量計產業的專利狀況突顯了全球的重大變化,其中中國佔專利申請的大部分,顯示出對流量測量技術創新的強烈關注。本分析旨在深入了解流量計領域的區域分佈和主要申請人,反映不同地區和企業之間的策略重點和創新趨勢。

中國專利申請量領先流量計產業,佔2023年專利申請總量的90.04%。這可能是由大規模工業化、政府支持以及對水資源管理、石化和能源等領域國內製造能力的強烈關注所推動,從而帶動了國內流量測量技術的發展。

美國緊隨其後,佔 2.9% 的申請量,這表明該行業可能正在關注更專業的創新。允許多國同時保護的專利合作條約(PCT)申請佔2.06%,顯示了旨在全球市場拓展和國際智慧財產權保護的策略。

其他值得注意的貢獻包括歐洲專利局(1.50%)、日本(1.24%)和俄羅斯聯邦(0.99%),每個國家都對流量測量技術進步做出了微小但重要的承諾。韓國、印度、加拿大和波蘭等國家的申請活動不大,但這顯示 2023 年各自地區將出現新的興趣和利基創新。

流量計產業的主要專利申請人以中國企業或公司為主,反映了中國在該領域的主導地位。中國石油化學股份有限公司(中石化)以專利申請總量的16.44%位居第一,凸顯其2023年策略重點是化學石油產業技術提升。

2023 年的專利格局凸顯出流量計技術的創新主要集中在中國,這表明國家戰略重點關注需要精密流量測量技術的產業。大型石油和燃氣公司被納入主要申請人之列,凸顯了該行業對流量計技術在營運效率和監管合規性方面的依賴。 PCT 申請的全球影響力也顯示了尋求跨國界創新的公司的策略利益,並且與業務擴張目標一致。

該分析概述了技術進步的關鍵領域和主要市場參與者的策略重點,為流量計行業相關人員(包括投資者、競爭對手和政策制定者)提供了重要見解。它也顯示了合作和競爭的潛力,特別是在專利活動較少但工業成長潛力強勁的地區。

分部概覽

流量計市場按類型、最終用戶和地區細分。依類型分為差壓式、正排量式、超音波、渦輪式、磁力式、科氏式、渦流式等。依最終用戶分為用水和污水、石油和天然氣、化學、發電、紙漿和造紙、食品和飲料等。從區域來看,我們對北美、歐洲、亞太地區和拉丁美洲地區進行了分析。

差壓 (DP) 流量計在流量計市場中的主導地位歸因於這些流量計的多功能性、成熟的技術和成本效益。 DP 流量計的工作原理很簡單,即管道收縮處的壓力降與流量直接相關。這種簡單性使得差壓計極其可靠且易於維護,使其在需要高精度和可靠性的行業中特別受重視。 DP流量計相容於多種流體,因此可應用於石油天然氣、化學、水處理等多種領域。此外,差壓流量計已被廣泛使用和測試數十年,形成了成熟的知識體系,易於整合到現有系統中,並被工程師和操作員廣泛接受。這些因素保證了差壓流量計在流量計市場的持續主導地位。

在流量計市場中,由於發電廠精確流量測量的重要性,發電業已成為主要的最終用戶。該領域的流量計對於營運效率、安全性和法規遵循至關重要。它廣泛用於測量發電過程中蒸氣、水和燃料(如天然氣和煤漿)的流量。準確的流量測量可確保最佳的鍋爐和渦輪機性能、有效的燃料管理並減少排放,符合環境法規。傳統能源和可再生能源領域的成長不斷增加對可靠、高效的流量測量解決方案的需求。隨著全球能源需求的增加以及技術向更高效、更環保的解決方案發展,發電業依賴精密流量測量技術,確保其在流量計市場的主導地位。

亞太地區在流量計市場的主導地位很大程度上歸功於全部區域快速的工業化和基礎設施開拓,以及對能源、用水和污水管理以及製造業等行業的大規模投資。中國和印度等國家擁有龐大的人口基數和快速成長的工業部門,對精密流量測量技術的需求正在激增,以支持和提高工業效率和監管合規性。此外,亞太地區對提高環境標準和投資可再生能源計劃的關注進一步增加了對先進流量測量解決方案的需求。該地區的技術採用和創新工作得到了政府措施和投資的支持,這也推動了市場的成長。

相關人員的主要利益

- 本報告對2023年至2033年流量計市場分析的細分市場、當前趨勢、估計/趨勢分析和動態進行了定量分析,以確定領先的流量計市場機會。

- 我們提供市場研究以及與市場促進因素、市場限制和市場機會相關的資訊。

- 波特的五力分析強調買家和供應商幫助相關人員做出利潤驅動的商業決策並加強供應商-買家網路的潛力。

- 詳細分析流量計市場細分以確定市場機會。

- 每個地區的主要國家都根據其對全球市場的收益貢獻繪製了地圖。

- 市場參與者定位有助於基準化分析,並提供對市場參與者當前地位的清晰了解。

- 它包括區域和全球流量計市場趨勢、主要企業、細分市場、應用領域、市場成長策略等的分析。

可使用此報告進行客製化(需要額外費用和時間表)

- 資本投資明細

- 最終用戶偏好和痛點

- 投資機會

- 按地區分類的新參與企業

- 科技趨勢分析

- 按產品/細分市場分類的參與者的市場佔有率分析

- 監管指引

- 策略建議

- 根據客戶興趣新增其他公司簡介

- 按國家或地區進行的附加分析 – 市場規模和預測

- 公司簡介的擴充列表

- 歷史市場資料

- 導入/匯出分析/資料

- 主要參與者的詳細資料(Excel格式,包括位置、聯絡資訊、供應商/供應商網路等)

- 客戶/消費者/原料供應商名單 - 價值鏈分析

- 全球/區域/國家層級參與者的市場佔有率分析

- SWOT分析

目錄

第1章簡介

第 2 章執行摘要

第3章市場概況

- 市場定義和範圍

- 主要發現

- 影響因素

- 主要投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 抑制因素

- 機會

- 價值鏈分析

- 關鍵監管分析

- 專利情況

第4章流量計市場:按類型

- 概述

- 差壓流量計

- 容積式流量計

- 超音波流量計

- 渦輪流量計

- 電磁流量計

- 科氏流量計

- 渦式流量計

- 其他

第5章流量計市場:依最終用戶分類

- 概述

- 用水和污水

- 油和氣

- 化學

- 發電

- 紙漿/造紙製造

- 食品與飲品

- 其他

第6章流量計市場:按地區

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 法國

- 德國

- 義大利

- 西班牙

- 英國

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他

- 拉丁美洲/中東/非洲

- 巴西

- 南非

- 沙烏地阿拉伯

- 其他

第7章 競爭格局

- 介紹

- 關鍵成功策略

- 10家主要企業產品圖譜

- 競爭對手儀表板

- 競爭熱圖

- 2023年主要企業定位

第8章 公司簡介

- Badger Meter Inc.

- Honeywell International Inc.

- Krohne Group

- Yokogawa Electric Corporation

- Schneider Electric

- Siemens AG

- Hitachi Ltd.

- ABB Ltd.

- Emerson Electric Co.

- Azbil Group

The flow meter market was valued at $9.9 billion in 2023, and is estimated to reach $17.1 billion by 2033, growing at a CAGR of 5.7% from 2024 to 2033.

Parent Market Overview

The flow meter market is derived from the industrial automation and instrumentation sector, which includes a wide array of devices, systems, and solutions designed to control, monitor, and optimize industrial processes. This broader market includes technologies such as control systems (PLCs, SCADA, and DCS), various types of instrumentation (sensors, transducers, and meters such as flow meters), automation software, and robotics. These components are integral to enhancing productivity, efficiency, and accuracy in industries ranging from manufacturing to energy, and from pharmaceuticals to water and wastewater management.

Key drivers of the market include increase in demand for operational efficiency and productivity, technological advancements in IoT, AI, and robotics, and stringent environmental and safety regulations that necessitate advanced monitoring and control technologies. In addition, there is a growing emphasis on sustainability and energy efficiency, which further propels the adoption of automation technologies. However, challenges such as high initial investment costs, the complexity of integrating new systems, and a shortage of skilled labor impede the market growth.

Introduction

The flow meter market includes a diverse range of devices designed to measure the flow rate or volume of a liquid, gas, or vapor through a pipe. Flow meters are crucial components across various industries, including water and wastewater management, oil and gas, chemicals, power generation, pharmaceuticals, food processing, and others. These devices are essential for ensuring accuracy, efficiency, safety, and regulatory compliance in numerous industrial processes.

Flow meters come in various types, including differential pressure, positive displacement, turbine, ultrasonic, magnetic, and Coriolis, each suited to specific applications and characterized by distinct operational advantages. The choice of flow meter by the user or a firm depends on several factors, such as the fluid characteristics, required accuracy, installation environment, and cost considerations.

Market Dynamics

Technological advancements in flow meters, such as the development of smart and ultrasonic flow meters, have broadened their applications and improved their accuracy and reliability. These advancements enhance the appeal of flow meters across various industries by offering better data integration capabilities and reducing maintenance needs. The importance of advanced flow meters grows as industries focus on automation and precise process control. These innovations improve operational efficiency as well as contribute to cost savings over time, thus encouraging more businesses to adopt these advanced technologies. Stringent environmental regulations globally compel industries to monitor and reduce their emissions and resource usage more closely. Flow meters are critical tools in achieving these regulatory requirements, as they precisely measure the flow of gases, liquids, and steam, which is essential for environmental reporting and ensuring compliance with laws aimed at reducing environmental impact. This regulatory pressure has made flow meters indispensable in industries such as manufacturing, power generation, and chemical processing, where accurate measurement is key to minimizing environmental footprints and avoiding hefty fines.

Economic downturns significantly impact investment in new technologies and equipment, including flow meters. During recessions or periods of economic instability, industries tend to cut back on capital expenditures to conserve resources, which directly affects the sales of non-essential and high-cost equipment such as advanced flow meters. Industries such as oil and gas, which are extremely sensitive to economic cycles, are expected to postpone or reduce their investment in upgrading instrumentation infrastructure. This reduction in spending due to economic conditions acts as a restraint on the flow meter market, delaying its growth until economic conditions improve.

Emerging markets offer significant growth opportunities for the flow meter market due to rapid industrialization, urbanization, and investment in infrastructure development. Countries in Asia-Pacific, Africa, and Latin America are witnessing increase in investments in sectors such as water & wastewater management, oil & gas, and energy, all of which require extensive use of flow meters. As these economies continue to develop, the demand for flow measurement solutions is expected to increase, providing a lucrative opportunity for manufacturers to expand their geographic footprint and increase market penetration.

The renewable energy sector is experiencing significant growth globally, driven by increase in emphasis on sustainable energy practices. Flow meters play a critical role in the operational processes of renewable energy production, such as in biofuel production, geothermal energy, and solar thermal energy systems. Their ability to ensure efficiency and monitor system performance is essential for optimizing energy output and reducing waste. The expanding renewable energy sector, therefore, presents a growing market for flow meters, as these devices help meet the industry's specific needs for precision and reliability in sustainable energy applications.

Patent Analysis-2023

The flow meter industry's patent landscape in 2023 highlighted significant global activity, particularly in China, which dominated the patent filings, signaling a robust focus on innovation in flow measurement technologies. This analysis aims to provide insights into the geographical distribution and key applicants in the flow meter sector, reflecting the strategic priorities and innovation trends across different regions and companies.

China led in patent filings in the flow meter industry with 90.04% of the total patents filed in 2023. This indicates a massive emphasis on developing flow measurement technologies within the country, potentially driven by large-scale industrialization, governmental support, and a strong focus on domestic manufacturing capabilities in sectors such as water management, petrochemicals, and energy.

The U.S. followed distantly with 2.9% of the filings, suggesting targeted, perhaps more specialized, innovation within the industry. The Patent Cooperation Treaty (PCT) applications, which allow for simultaneous protection in multiple countries, account for 2.06%, pointing to strategies aimed at global market expansion and international intellectual property protection.

Other notable contributions are from the European Patent Office (1.50%), Japan (1.24%), and the Russian Federation (0.99%), each reflecting a smaller, yet significant commitment to technological advancements in flow measurement. Countries such as the Republic of Korea, India, Canada, and Poland had modest filing activities, indicating emerging interests or niche innovations in their respective regions in 2023.

The leading applicants for patents in the flow meter industry include corporations or firms primarily based in China, indicative of the country's dominance in this sector. China Petroleum and Chemical Co (Sinopec) leads with 16.44% of the total patents filed, emphasizing its strategic focus on enhancing technology in the chemical and petroleum industries in 2023.

Micro Motion Inc. and Ningbo Water Meter (Group) Co. Ltd. each hold 11.56% of the filings, showcasing their significant contributions to advancing flow meter technology. Xi'an Thermal Power Research Institute Co. Ltd. and PetroChina Company Limited also display considerable activity, underlining the importance of flow measurement in the energy and power sectors.

Southwest Petroleum University and Saudi Arabian Oil Company (Saudi Aramco) show substantial engagement in patent filings, reflecting the academic and industry synergies driving innovation. Sanchuan Wisdom Tech Co. Ltd., Juelong Sensing Tech (Shenzhen) Co. Ltd., and Qingdao Topscomm Communication Co. Ltd. firms are illustrating the technological advancements being pursued across different applications within China.

The patent landscape in 2023 underscores a significant concentration of flow meter technology innovations within China, suggesting a national strategic focus on industries requiring precise flow measurement technologies. The presence of major oil and gas players among the top applicants highlights the sector's reliance on flow meter technologies for operational efficiency and regulatory compliance. Also, the global spread in PCT filings indicates a strategic interest by companies to secure their innovations across borders, aligning with business expansion goals.

This analysis provides crucial insights for stakeholders within the flow meter industry, including investors, competitors, and policymakers, by outlining key areas of technological advancement and the strategic focus of leading market players. It also suggests potential areas for collaboration and competition, particularly in regions with lower patent activity but significant industrial growth potential.

Segment Overview

The flow meter market is segmented into type, end user, and region. Depending on type, the market is divided into differential pressure, positive displacement, ultrasonic, turbine, magnetic, coriolis, vortex, and others. By end user, it is classified into water & wastewater, oil & gas, chemicals, power generation, pulp & paper, food & beverages, and others. Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

The dominance of the differential pressure (DP) flow meter segment in the flow meter market is attributed to the versatility, proven technology, and cost-effectiveness of these meters. DP flow meters operate on a straightforward principle where the pressure drop across a constriction in the pipeline correlates directly to the flow rate. This simplicity makes DP meters exceptionally reliable and easy to maintain, which is particularly valued in industries requiring high accuracy and reliability. They are suitable for a wide range of fluids, making them applicable across various sectors such as oil and gas, chemicals, and water treatment. Moreover, DP flow meters have been extensively used and tested over decades, leading to a well-established body of knowledge, ease of integration into existing systems, and widespread acceptance among engineers and operators. These factors collectively ensure their ongoing dominance in the flow meter market.

In the flow meter market, the power generation segment emerges as a dominant end-user due to the critical importance of accurate flow measurement in power plants. Flow meters in this sector are vital for operational efficiency, safety, and regulatory compliance. They are used extensively for measuring the flow of steam, water, and fuels (such as natural gas or coal slurry) within the power generation process. Accurate flow measurements ensure optimal performance of boilers and turbines, effective fuel management, and reduced emissions, aligning with environmental regulations. The growth in both traditional and renewable energy sectors continue to drive demand for reliable and efficient flow measurement solutions. As global energy needs increase and as technologies evolve towards more efficient and eco-friendly solutions, the power generation sector's reliance on precise flow measurement technologies ensures its dominant status in the flow meter market.

Asia-Pacific's dominance in the flow meter market is largely attributed to the rapid industrialization and infrastructure development across the region, coupled with significant investments in sectors such as energy, water & wastewater management, and manufacturing. Countries like China and India, with their massive population bases and burgeoning industrial sectors, have seen a surge in demand for precise flow measurement technologies to support and enhance industrial efficiency and regulatory compliance. In addition, Asia-Pacific's focus on improving environmental standards and investing in renewable energy projects has further increased the demand for advanced flow metering solutions. The region's commitment to technological adoption and innovation, supported by government initiatives and investments, also fuels the market growth.

The major flow meter market players include Badger Meter Inc., Honeywell International, Krohne Group, Yokogawa Electric Corporation, Schneider Electric SE, Siemens AG, Hitachi, Ltd., ABB Ltd., Emerson Electric Company, and Azbil Group.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the flow meter market analysis from 2023 to 2033 to identify the prevailing flow meter market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the flow meter market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global flow meter market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Capital Investment breakdown

- End user preferences and pain points

- Investment Opportunities

- Upcoming/New Entrant by Regions

- Technology Trend Analysis

- Market share analysis of players by products/segments

- Regulatory Guidelines

- Strategic Recommendations

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- Import Export Analysis/Data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- List of customers/consumers/raw material suppliers- value chain analysis

- Market share analysis of players at global/region/country level

- SWOT Analysis

Key Market Segments

By Type

- Positive displacement Flow Meter

- Ultrasonic Flow Meter

- Turbine Flow Meter

- Magnetic Flow Meter

- Coriolis Flow Meter

- Vortex Flow Meter

- Others

- Differential Pressure Flow Meter

By End User

- Water and Wastewater

- Oil and Gas

- Chemicals

- Power Generation

- Pulp and Paper

- Food and Beverages

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- South Africa,

- Saudi Arabia

- Rest of LAMEA

Key Market Players:

- Badger Meter Inc.

- Honeywell International Inc.

- Krohne Group

- Yokogawa Electric Corporation

- Schneider Electric

- Siemens AG

- Hitachi Ltd.

- ABB Ltd.

- Emerson Electric Co.

- Azbil Group

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

- 3.5. Value Chain Analysis

- 3.6. Key Regulation Analysis

- 3.7. Patent Landscape

CHAPTER 4: FLOW METER MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Differential Pressure Flow Meter

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Positive displacement Flow Meter

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Ultrasonic Flow Meter

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Turbine Flow Meter

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

- 4.6. Magnetic Flow Meter

- 4.6.1. Key market trends, growth factors and opportunities

- 4.6.2. Market size and forecast, by region

- 4.6.3. Market share analysis by country

- 4.7. Coriolis Flow Meter

- 4.7.1. Key market trends, growth factors and opportunities

- 4.7.2. Market size and forecast, by region

- 4.7.3. Market share analysis by country

- 4.8. Vortex Flow Meter

- 4.8.1. Key market trends, growth factors and opportunities

- 4.8.2. Market size and forecast, by region

- 4.8.3. Market share analysis by country

- 4.9. Others

- 4.9.1. Key market trends, growth factors and opportunities

- 4.9.2. Market size and forecast, by region

- 4.9.3. Market share analysis by country

CHAPTER 5: FLOW METER MARKET, BY END USER

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Water and Wastewater

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Oil and Gas

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Chemicals

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Power Generation

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

- 5.6. Pulp and Paper

- 5.6.1. Key market trends, growth factors and opportunities

- 5.6.2. Market size and forecast, by region

- 5.6.3. Market share analysis by country

- 5.7. Food and Beverages

- 5.7.1. Key market trends, growth factors and opportunities

- 5.7.2. Market size and forecast, by region

- 5.7.3. Market share analysis by country

- 5.8. Others

- 5.8.1. Key market trends, growth factors and opportunities

- 5.8.2. Market size and forecast, by region

- 5.8.3. Market share analysis by country

CHAPTER 6: FLOW METER MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by Type

- 6.2.3. Market size and forecast, by End User

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Market size and forecast, by Type

- 6.2.4.1.2. Market size and forecast, by End User

- 6.2.4.2. Canada

- 6.2.4.2.1. Market size and forecast, by Type

- 6.2.4.2.2. Market size and forecast, by End User

- 6.2.4.3. Mexico

- 6.2.4.3.1. Market size and forecast, by Type

- 6.2.4.3.2. Market size and forecast, by End User

- 6.3. Europe

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by Type

- 6.3.3. Market size and forecast, by End User

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. France

- 6.3.4.1.1. Market size and forecast, by Type

- 6.3.4.1.2. Market size and forecast, by End User

- 6.3.4.2. Germany

- 6.3.4.2.1. Market size and forecast, by Type

- 6.3.4.2.2. Market size and forecast, by End User

- 6.3.4.3. Italy

- 6.3.4.3.1. Market size and forecast, by Type

- 6.3.4.3.2. Market size and forecast, by End User

- 6.3.4.4. Spain

- 6.3.4.4.1. Market size and forecast, by Type

- 6.3.4.4.2. Market size and forecast, by End User

- 6.3.4.5. UK

- 6.3.4.5.1. Market size and forecast, by Type

- 6.3.4.5.2. Market size and forecast, by End User

- 6.3.4.6. Rest of Europe

- 6.3.4.6.1. Market size and forecast, by Type

- 6.3.4.6.2. Market size and forecast, by End User

- 6.4. Asia-Pacific

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by Type

- 6.4.3. Market size and forecast, by End User

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Market size and forecast, by Type

- 6.4.4.1.2. Market size and forecast, by End User

- 6.4.4.2. Japan

- 6.4.4.2.1. Market size and forecast, by Type

- 6.4.4.2.2. Market size and forecast, by End User

- 6.4.4.3. India

- 6.4.4.3.1. Market size and forecast, by Type

- 6.4.4.3.2. Market size and forecast, by End User

- 6.4.4.4. South Korea

- 6.4.4.4.1. Market size and forecast, by Type

- 6.4.4.4.2. Market size and forecast, by End User

- 6.4.4.5. Australia

- 6.4.4.5.1. Market size and forecast, by Type

- 6.4.4.5.2. Market size and forecast, by End User

- 6.4.4.6. Rest of Asia-Pacific

- 6.4.4.6.1. Market size and forecast, by Type

- 6.4.4.6.2. Market size and forecast, by End User

- 6.5. LAMEA

- 6.5.1. Key market trends, growth factors and opportunities

- 6.5.2. Market size and forecast, by Type

- 6.5.3. Market size and forecast, by End User

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Market size and forecast, by Type

- 6.5.4.1.2. Market size and forecast, by End User

- 6.5.4.2. South Africa,

- 6.5.4.2.1. Market size and forecast, by Type

- 6.5.4.2.2. Market size and forecast, by End User

- 6.5.4.3. Saudi Arabia

- 6.5.4.3.1. Market size and forecast, by Type

- 6.5.4.3.2. Market size and forecast, by End User

- 6.5.4.4. Rest of LAMEA

- 6.5.4.4.1. Market size and forecast, by Type

- 6.5.4.4.2. Market size and forecast, by End User

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product mapping of top 10 player

- 7.4. Competitive dashboard

- 7.5. Competitive heatmap

- 7.6. Top player positioning, 2023

CHAPTER 8: COMPANY PROFILES

- 8.1. Badger Meter Inc.

- 8.1.1. Company overview

- 8.1.2. Key executives

- 8.1.3. Company snapshot

- 8.1.4. Operating business segments

- 8.1.5. Product portfolio

- 8.1.6. Business performance

- 8.1.7. Key strategic moves and developments

- 8.2. Honeywell International Inc.

- 8.2.1. Company overview

- 8.2.2. Key executives

- 8.2.3. Company snapshot

- 8.2.4. Operating business segments

- 8.2.5. Product portfolio

- 8.2.6. Business performance

- 8.2.7. Key strategic moves and developments

- 8.3. Krohne Group

- 8.3.1. Company overview

- 8.3.2. Key executives

- 8.3.3. Company snapshot

- 8.3.4. Operating business segments

- 8.3.5. Product portfolio

- 8.3.6. Business performance

- 8.3.7. Key strategic moves and developments

- 8.4. Yokogawa Electric Corporation

- 8.4.1. Company overview

- 8.4.2. Key executives

- 8.4.3. Company snapshot

- 8.4.4. Operating business segments

- 8.4.5. Product portfolio

- 8.4.6. Business performance

- 8.4.7. Key strategic moves and developments

- 8.5. Schneider Electric

- 8.5.1. Company overview

- 8.5.2. Key executives

- 8.5.3. Company snapshot

- 8.5.4. Operating business segments

- 8.5.5. Product portfolio

- 8.5.6. Business performance

- 8.5.7. Key strategic moves and developments

- 8.6. Siemens AG

- 8.6.1. Company overview

- 8.6.2. Key executives

- 8.6.3. Company snapshot

- 8.6.4. Operating business segments

- 8.6.5. Product portfolio

- 8.6.6. Business performance

- 8.6.7. Key strategic moves and developments

- 8.7. Hitachi Ltd.

- 8.7.1. Company overview

- 8.7.2. Key executives

- 8.7.3. Company snapshot

- 8.7.4. Operating business segments

- 8.7.5. Product portfolio

- 8.7.6. Business performance

- 8.7.7. Key strategic moves and developments

- 8.8. ABB Ltd.

- 8.8.1. Company overview

- 8.8.2. Key executives

- 8.8.3. Company snapshot

- 8.8.4. Operating business segments

- 8.8.5. Product portfolio

- 8.8.6. Business performance

- 8.8.7. Key strategic moves and developments

- 8.9. Emerson Electric Co.

- 8.9.1. Company overview

- 8.9.2. Key executives

- 8.9.3. Company snapshot

- 8.9.4. Operating business segments

- 8.9.5. Product portfolio

- 8.9.6. Business performance

- 8.9.7. Key strategic moves and developments

- 8.10. Azbil Group

- 8.10.1. Company overview

- 8.10.2. Key executives

- 8.10.3. Company snapshot

- 8.10.4. Operating business segments

- 8.10.5. Product portfolio

- 8.10.6. Business performance

- 8.10.7. Key strategic moves and developments

LIST OF TABLES

- TABLE 01. GLOBAL FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 02. FLOW METER MARKET FOR DIFFERENTIAL PRESSURE FLOW METER, BY REGION, 2023-2033 ($MILLION)

- TABLE 03. FLOW METER MARKET FOR POSITIVE DISPLACEMENT FLOW METER, BY REGION, 2023-2033 ($MILLION)

- TABLE 04. FLOW METER MARKET FOR ULTRASONIC FLOW METER, BY REGION, 2023-2033 ($MILLION)

- TABLE 05. FLOW METER MARKET FOR TURBINE FLOW METER, BY REGION, 2023-2033 ($MILLION)

- TABLE 06. FLOW METER MARKET FOR MAGNETIC FLOW METER, BY REGION, 2023-2033 ($MILLION)

- TABLE 07. FLOW METER MARKET FOR CORIOLIS FLOW METER, BY REGION, 2023-2033 ($MILLION)

- TABLE 08. FLOW METER MARKET FOR VORTEX FLOW METER, BY REGION, 2023-2033 ($MILLION)

- TABLE 09. FLOW METER MARKET FOR OTHERS, BY REGION, 2023-2033 ($MILLION)

- TABLE 10. GLOBAL FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 11. FLOW METER MARKET FOR WATER AND WASTEWATER, BY REGION, 2023-2033 ($MILLION)

- TABLE 12. FLOW METER MARKET FOR OIL AND GAS, BY REGION, 2023-2033 ($MILLION)

- TABLE 13. FLOW METER MARKET FOR CHEMICALS, BY REGION, 2023-2033 ($MILLION)

- TABLE 14. FLOW METER MARKET FOR POWER GENERATION, BY REGION, 2023-2033 ($MILLION)

- TABLE 15. FLOW METER MARKET FOR PULP AND PAPER, BY REGION, 2023-2033 ($MILLION)

- TABLE 16. FLOW METER MARKET FOR FOOD AND BEVERAGES, BY REGION, 2023-2033 ($MILLION)

- TABLE 17. FLOW METER MARKET FOR OTHERS, BY REGION, 2023-2033 ($MILLION)

- TABLE 18. FLOW METER MARKET, BY REGION, 2023-2033 ($MILLION)

- TABLE 19. NORTH AMERICA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 20. NORTH AMERICA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 21. NORTH AMERICA FLOW METER MARKET, BY COUNTRY, 2023-2033 ($MILLION)

- TABLE 22. U.S. FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 23. U.S. FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 24. CANADA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 25. CANADA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 26. MEXICO FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 27. MEXICO FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 28. EUROPE FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 29. EUROPE FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 30. EUROPE FLOW METER MARKET, BY COUNTRY, 2023-2033 ($MILLION)

- TABLE 31. FRANCE FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 32. FRANCE FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 33. GERMANY FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 34. GERMANY FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 35. ITALY FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 36. ITALY FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 37. SPAIN FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 38. SPAIN FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 39. UK FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 40. UK FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 41. REST OF EUROPE FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 42. REST OF EUROPE FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 43. ASIA-PACIFIC FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 44. ASIA-PACIFIC FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 45. ASIA-PACIFIC FLOW METER MARKET, BY COUNTRY, 2023-2033 ($MILLION)

- TABLE 46. CHINA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 47. CHINA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 48. JAPAN FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 49. JAPAN FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 50. INDIA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 51. INDIA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 52. SOUTH KOREA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 53. SOUTH KOREA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 54. AUSTRALIA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 55. AUSTRALIA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 56. REST OF ASIA-PACIFIC FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 57. REST OF ASIA-PACIFIC FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 58. LAMEA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 59. LAMEA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 60. LAMEA FLOW METER MARKET, BY COUNTRY, 2023-2033 ($MILLION)

- TABLE 61. BRAZIL FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 62. BRAZIL FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 63. SOUTH AFRICA, FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 64. SOUTH AFRICA, FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 65. SAUDI ARABIA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 66. SAUDI ARABIA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 67. REST OF LAMEA FLOW METER MARKET, BY TYPE, 2023-2033 ($MILLION)

- TABLE 68. REST OF LAMEA FLOW METER MARKET, BY END USER, 2023-2033 ($MILLION)

- TABLE 69. BADGER METER INC.: KEY EXECUTIVES

- TABLE 70. BADGER METER INC.: COMPANY SNAPSHOT

- TABLE 71. BADGER METER INC.: PRODUCT SEGMENTS

- TABLE 72. BADGER METER INC.: SERVICE SEGMENTS

- TABLE 73. BADGER METER INC.: PRODUCT PORTFOLIO

- TABLE 74. BADGER METER INC.: KEY STRATEGIES

- TABLE 75. HONEYWELL INTERNATIONAL INC.: KEY EXECUTIVES

- TABLE 76. HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

- TABLE 77. HONEYWELL INTERNATIONAL INC.: PRODUCT SEGMENTS

- TABLE 78. HONEYWELL INTERNATIONAL INC.: SERVICE SEGMENTS

- TABLE 79. HONEYWELL INTERNATIONAL INC.: PRODUCT PORTFOLIO

- TABLE 80. HONEYWELL INTERNATIONAL INC.: KEY STRATEGIES

- TABLE 81. KROHNE GROUP: KEY EXECUTIVES

- TABLE 82. KROHNE GROUP: COMPANY SNAPSHOT

- TABLE 83. KROHNE GROUP: PRODUCT SEGMENTS

- TABLE 84. KROHNE GROUP: SERVICE SEGMENTS

- TABLE 85. KROHNE GROUP: PRODUCT PORTFOLIO

- TABLE 86. KROHNE GROUP: KEY STRATEGIES

- TABLE 87. YOKOGAWA ELECTRIC CORPORATION: KEY EXECUTIVES

- TABLE 88. YOKOGAWA ELECTRIC CORPORATION: COMPANY SNAPSHOT

- TABLE 89. YOKOGAWA ELECTRIC CORPORATION: PRODUCT SEGMENTS

- TABLE 90. YOKOGAWA ELECTRIC CORPORATION: SERVICE SEGMENTS

- TABLE 91. YOKOGAWA ELECTRIC CORPORATION: PRODUCT PORTFOLIO

- TABLE 92. YOKOGAWA ELECTRIC CORPORATION: KEY STRATEGIES

- TABLE 93. SCHNEIDER ELECTRIC: KEY EXECUTIVES

- TABLE 94. SCHNEIDER ELECTRIC: COMPANY SNAPSHOT

- TABLE 95. SCHNEIDER ELECTRIC: PRODUCT SEGMENTS

- TABLE 96. SCHNEIDER ELECTRIC: SERVICE SEGMENTS

- TABLE 97. SCHNEIDER ELECTRIC: PRODUCT PORTFOLIO

- TABLE 98. SCHNEIDER ELECTRIC: KEY STRATEGIES

- TABLE 99. SIEMENS AG: KEY EXECUTIVES

- TABLE 100. SIEMENS AG: COMPANY SNAPSHOT

- TABLE 101. SIEMENS AG: PRODUCT SEGMENTS

- TABLE 102. SIEMENS AG: SERVICE SEGMENTS

- TABLE 103. SIEMENS AG: PRODUCT PORTFOLIO

- TABLE 104. SIEMENS AG: KEY STRATEGIES

- TABLE 105. HITACHI LTD.: KEY EXECUTIVES

- TABLE 106. HITACHI LTD.: COMPANY SNAPSHOT

- TABLE 107. HITACHI LTD.: PRODUCT SEGMENTS

- TABLE 108. HITACHI LTD.: SERVICE SEGMENTS

- TABLE 109. HITACHI LTD.: PRODUCT PORTFOLIO

- TABLE 110. HITACHI LTD.: KEY STRATEGIES

- TABLE 111. ABB LTD.: KEY EXECUTIVES

- TABLE 112. ABB LTD.: COMPANY SNAPSHOT

- TABLE 113. ABB LTD.: PRODUCT SEGMENTS

- TABLE 114. ABB LTD.: SERVICE SEGMENTS

- TABLE 115. ABB LTD.: PRODUCT PORTFOLIO

- TABLE 116. ABB LTD.: KEY STRATEGIES

- TABLE 117. EMERSON ELECTRIC CO.: KEY EXECUTIVES

- TABLE 118. EMERSON ELECTRIC CO.: COMPANY SNAPSHOT

- TABLE 119. EMERSON ELECTRIC CO.: PRODUCT SEGMENTS

- TABLE 120. EMERSON ELECTRIC CO.: SERVICE SEGMENTS

- TABLE 121. EMERSON ELECTRIC CO.: PRODUCT PORTFOLIO

- TABLE 122. EMERSON ELECTRIC CO.: KEY STRATEGIES

- TABLE 123. AZBIL GROUP: KEY EXECUTIVES

- TABLE 124. AZBIL GROUP: COMPANY SNAPSHOT

- TABLE 125. AZBIL GROUP: PRODUCT SEGMENTS

- TABLE 126. AZBIL GROUP: SERVICE SEGMENTS

- TABLE 127. AZBIL GROUP: PRODUCT PORTFOLIO

- TABLE 128. AZBIL GROUP: KEY STRATEGIES

LIST OF FIGURES

- FIGURE 01. FLOW METER MARKET, 2023-2033

- FIGURE 02. SEGMENTATION OF FLOW METER MARKET,2023-2033

- FIGURE 03. TOP IMPACTING FACTORS IN FLOW METER MARKET

- FIGURE 04. TOP INVESTMENT POCKETS IN FLOW METER MARKET (2024-2033)

- FIGURE 05. BARGAINING POWER OF SUPPLIERS

- FIGURE 06. BARGAINING POWER OF BUYERS

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. THREAT OF SUBSTITUTION

- FIGURE 09. COMPETITIVE RIVALRY

- FIGURE 10. GLOBAL FLOW METER MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. IMPACT OF KEY REGULATION: FLOW METER MARKET

- FIGURE 12. PATENT ANALYSIS BY COMPANY

- FIGURE 13. PATENT ANALYSIS BY COUNTRY

- FIGURE 14. FLOW METER MARKET, BY TYPE, 2023 AND 2033(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR DIFFERENTIAL PRESSURE FLOW METER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR POSITIVE DISPLACEMENT FLOW METER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR ULTRASONIC FLOW METER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR TURBINE FLOW METER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR MAGNETIC FLOW METER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR CORIOLIS FLOW METER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR VORTEX FLOW METER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR OTHERS, BY COUNTRY 2023 AND 2033(%)

- FIGURE 23. FLOW METER MARKET, BY END USER, 2023 AND 2033(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR WATER AND WASTEWATER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR OIL AND GAS, BY COUNTRY 2023 AND 2033(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR CHEMICALS, BY COUNTRY 2023 AND 2033(%)

- FIGURE 27. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR POWER GENERATION, BY COUNTRY 2023 AND 2033(%)

- FIGURE 28. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR PULP AND PAPER, BY COUNTRY 2023 AND 2033(%)

- FIGURE 29. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR FOOD AND BEVERAGES, BY COUNTRY 2023 AND 2033(%)

- FIGURE 30. COMPARATIVE SHARE ANALYSIS OF FLOW METER MARKET FOR OTHERS, BY COUNTRY 2023 AND 2033(%)

- FIGURE 31. FLOW METER MARKET BY REGION, 2023 AND 2033(%)

- FIGURE 32. U.S. FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 33. CANADA FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 34. MEXICO FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 35. FRANCE FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 36. GERMANY FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 37. ITALY FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 38. SPAIN FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 39. UK FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 40. REST OF EUROPE FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 41. CHINA FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 42. JAPAN FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 43. INDIA FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 44. SOUTH KOREA FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 45. AUSTRALIA FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 46. REST OF ASIA-PACIFIC FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 47. BRAZIL FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 48. SOUTH AFRICA, FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 49. SAUDI ARABIA FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 50. REST OF LAMEA FLOW METER MARKET, 2023-2033 ($MILLION)

- FIGURE 51. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 52. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 53. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 54. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 55. COMPETITIVE DASHBOARD

- FIGURE 56. COMPETITIVE HEATMAP: FLOW METER MARKET

- FIGURE 57. TOP PLAYER POSITIONING, 2023

2025 年流量計全球市場報告

2025 年流量計全球市場報告 全球流量計市場規模、佔有率、趨勢分析報告:2024 年至 2031 年按應用、產品類型和地區分類的展望和預測

全球流量計市場規模、佔有率、趨勢分析報告:2024 年至 2031 年按應用、產品類型和地區分類的展望和預測 2025-2033 年按產品類型、應用和地區分類的流量計市場規模、佔有率、趨勢和預測

2025-2033 年按產品類型、應用和地區分類的流量計市場規模、佔有率、趨勢和預測 電磁式流量計市場規模、佔有率和成長分析(按產品類型、組件、技術、最終用途產業和地區)- 產業預測,2025-2032 年

電磁式流量計市場規模、佔有率和成長分析(按產品類型、組件、技術、最終用途產業和地區)- 產業預測,2025-2032 年 流量計 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

流量計 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 文丘里管市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、材料類型、應用、地區和競爭細分,2019-2029F

文丘里管市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、材料類型、應用、地區和競爭細分,2019-2029F 流量計市場規模、佔有率、成長分析、類型、最終用戶產業、地區 - 產業預測,2024-2031

流量計市場規模、佔有率、成長分析、類型、最終用戶產業、地區 - 產業預測,2024-2031 文氏管市場,按材料類型、尺寸、應用、最終用戶、國家和地區 - 2024-2032年行業分析、市場規模、市場佔有率和預測

文氏管市場,按材料類型、尺寸、應用、最終用戶、國家和地區 - 2024-2032年行業分析、市場規模、市場佔有率和預測 管線內時間差超音波流量計市場,按介質類型、技術、流量範圍、應用、國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測

管線內時間差超音波流量計市場,按介質類型、技術、流量範圍、應用、國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測 流量計市場:按類型、流體類型、便攜性、安裝形式、應用分類 - 2025-2030 年全球預測

流量計市場:按類型、流體類型、便攜性、安裝形式、應用分類 - 2025-2030 年全球預測