|

市場調查報告書

商品編碼

1641781

全球清潔能源基礎設施市場(按基礎設施類型和最終用途)- 機會分析和產業預測,2024 年至 2033 年Clean Energy Infrastructure Market By Infrastructure Type, By End-Use : Global Opportunity Analysis and Industry Forecast, 2024-2033 |

||||||

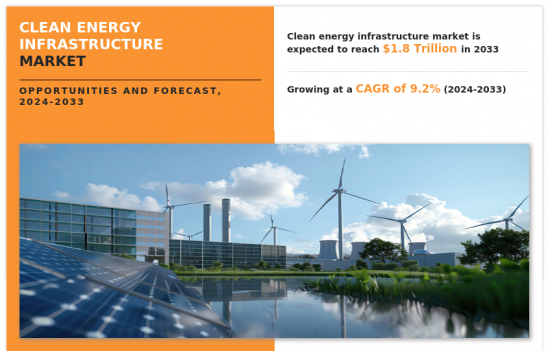

預計2023年全球清潔能源基礎設施市場規模將達到7,000億美元,到2033年將達到1.8兆美元,2024年至2033年的複合年成長率為9.2%。

清潔能源基礎設施是指用於產生、儲存、分配和管理風能、太陽能、水力發電、地熱能和生質能源等可再生、環保能源來源的系統、設施和技術網路。這種基礎設施在世界向永續能源系統轉變的過程中發揮著至關重要的作用,旨在減少傳統石化燃料能源生產對環境的影響。這種轉變是由於人們對氣候變遷、自然資源枯竭和能源安全需求日益成長的擔憂所致。清潔能源基礎設施對於實現減少碳排放、在不損害環境的情況下促進經濟和社會發展的全球目標至關重要。

技術進步在改造清潔能源基礎設施、提高效率和可負擔性方面發揮關鍵作用。技術創新的重點領域之一是能源儲存。電池技術的進步,特別是鋰離子和固態電池電池和液流電池等下一代解決方案,使得可再生能源的儲存更加可靠。透過確保在發電量低的時期儲存和部署多餘的能源,可以更好地管理風能和太陽能等間歇性能源來源。大規模能源儲存系統擴大被整合到電網中,以穩定供電並實現向全天候清潔能源發電的過渡。根據國際可再生能源機構的預測,2022年全球水力發電裝置容量將達到1,393吉瓦(GW),比2021年成長2.19%。由於即將上馬的發電工程和技術進步,水力發電裝置容量預計會增加。預計所有這些因素都將在預測期內推動全球清潔能源基礎設施市場的成長。

然而,高昂的前期投資成本對清潔能源基礎設施的擴張構成了重大挑戰。建造太陽能和風力發電場等可再生能源計劃以及對現有電網進行必要的升級,需要大量的前期投資資本。這些成本不僅包括採購先進技術,還包括安裝、土地徵用和與更廣泛的電網的整合。對於資金籌措管道有限的地區,尤其是新興國家,獲得啟動此類計劃所需的資金可能是一個巨大的障礙。儘管清潔能源技術可以帶來長期的經濟和環境效益,但這些資金障礙往往會阻礙其應用。

如果沒有政府強力的獎勵和盈利保障,私部門不願意在可再生能源基礎設施上進行大量投資。傳統石化燃料能源來源通常具有成熟的供應鏈和基礎設施,使得其在短期內具有經濟吸引力。因此,可再生能源計劃被視為風險較高的投資,前期成本更高,並且依賴長期收益,容易受到市場條件波動和政策變化的影響。所有這些因素都在阻礙全球清潔能源基礎設施市場的成長。

微電網和分散式發電技術的興起使得在當地進行能源生產和消費成為可能,減少了對大型集中式能源電網的依賴。這種轉變對於能源基礎設施不穩定或易發生自然災害的地區尤其有吸引力,因為分散式系統可以提供能源安全性和彈性。此外,分散式系統使社區和企業能夠產生、儲存和管理其能源需求,為清潔能源產品和服務創造新的市場。 2022 年 12 月,班加羅爾電力供應有限公司 (BESCOM) 啟動了其併網屋頂太陽能舉措的第二階段。這一階段旨在擴大太陽能板的安裝,BESCOM 已收到印度新可再生能源部 (MNRE) 的指令,安裝 10 兆瓦的太陽能容量。該舉措是鼓勵分散式能源發電的更廣泛策略的一部分。 2022年11月,密西根州分散式發電計畫成長了37%,增加了3,709名新客戶。這一成長使參與人數總數達到 14,262 人,分散式發電裝置數量達到 14,446 個。該計劃主要關注太陽能,讓客戶自行發電並降低家庭能源成本。所有這些因素預計將為全球清潔能源基礎設施市場提供新的成長機會。

清潔能源基礎設施市場根據基礎設施類型、最終用途和地區進行細分。依基礎設施類型,分為發電設備、能源儲存系統、輸電和配電網路。根據最終用途,市場分為住宅、商業和工業。根據地區,市場分為北美、歐洲、亞太、拉丁美洲和中東及非洲。

根據基礎設施類型,發電設施部門佔據市場主導地位,預測期內複合年成長率為 9.2%。清潔能源基礎設施在發電中發揮關鍵作用,推動了從石化燃料轉向永續能源來源的轉變。在公共產業規模的太陽能發電廠,使用太陽能追蹤器和能源儲存系統等先進技術可以提高效率。太陽能追蹤器使光伏板能夠跟隨太陽的路徑,全天捕獲最大量的能量。電池透過儲存多餘的電力以供陰天或夜間使用來解決間歇性問題。

根據最終用途,工業領域在預測期內以 8.9% 的複合年成長率佔據市場主導地位。工業領域清潔能源轉型最重要的策略之一是再生能源來源的整合。太陽能和風能由於其擴充性和成本下降而成為主要選擇。現在,許多工業設施都在其屋頂或廠房內安裝了太陽能電池板來利用太陽能。除了太陽能和風能之外,生質能能由於可以利用有機廢棄物和單一產品而在工業領域越來越受歡迎。生質能可以轉化為電能和熱能,使其成為傳統能源來源的永續能源來源品。排放大量有機廢棄物的產業,如造紙、食品加工和農業,特別適合從生質能系統中受益。

根據地區,市場分析涵蓋北美、歐洲、亞太、中東和拉丁美洲。預計2023年亞太地區將佔全球清潔能源基礎設施市場佔有率的三分之一以上,並在預測期內保持主導地位。亞太地區是全球清潔能源關鍵零件的製造地。中國在全球太陽能板生產領域佔據主導地位,生產了全球相當一部分供應。該國廣泛的製造能力也延伸到風力發電機和電池領域,中國和韓國在生產對於能源儲存和電動車至關重要的鋰離子電池方面處於領先地位。

主要發現

- 根據基礎設施類型,發電設施將成長最快,預測期內複合年成長率為 9.2%。

- 根據最終用途,商業設施預計將成長最快,預測期內複合年成長率為 9.6%。

- 按地區分類,亞太地區在 2022 年佔據最大的銷售額佔有率。

相關人員的主要利益

- 本報告定量分析了 2023 年至 2033 年清潔能源基礎設施市場分析的市場細分、當前趨勢、估計、趨勢和動態,並確定了清潔能源基礎設施市場中的突出市場機會。

- 它為市場研究提供與市場促進因素、市場限制因素和市場機會相關的資訊。

- 波特五力分析揭示了買家和供應商的潛力,幫助相關人員做出利潤驅動的商業決策,並加強供應商-買家網路。

- 對清潔能源基礎設施市場細分進行詳細分析有助於發現市場機會。

- 每個地區的主要國家都根據收益貢獻進行分類。

- 市場公司的定位有利於基準化分析,並能清楚了解市場公司的當前地位。

- 本報告包括區域和全球清潔能源基礎設施市場趨勢、主要企業、細分市場、應用領域和市場成長策略的分析。

此報告可進行客製化(可能需要支付額外費用和製定時間表)

- 生產能力

- 資本投資明細

- 消費者購買行為分析

- 投資機會

- 供應鏈分析與供應商利潤

- 新參與企業(按地區)

- 科技趨勢分析

- 經銷商利潤分析

- 打入市場策略

- 按產品/細分市場進行市場細分

- 主要公司的新產品開發/產品矩陣

- 監管指南

- 根據客戶興趣提供額外的公司簡介

- 按國家或地區進行的額外分析 - 市場規模和預測

- 品牌佔有率分析

- 擴展公司簡介列表

- 歷史市場資料

- 導入/匯出分析/資料

- Excel 格式的主要企業詳細資料(包括位置、聯絡資訊、供應商/供應商網路等)

- 全球/地區/國家層面的公司市場佔有率分析

- 產品消費分析

- SWOT 分析

目錄

第 1 章 簡介

第 2 章執行摘要

第3章 市場概況

- 市場定義和範圍

- 主要發現

- 關鍵影響因素

- 重大投資機會

- 波特五力分析

- 市場動態

- 驅動程式

- 能源儲存、智慧電網和可再生能源技術快速發展

- 增加政府政策和獎勵

- 限制因素

- 初期投資成本高

- 機會

- 分散式能源系統需求不斷成長

- 驅動程式

- 價值鏈分析

- 監管指南

第4章 清潔能源基礎設施市場(依基礎設施類型)

- 概述

- 發電設施

- 能源儲存系統

- 傳播

- 電網

第5章 清潔能源基礎設施市場(按應用)

- 概述

- 住宅

- 商業的

- 產業

第6章 清潔能源基礎設施市場(按區域)

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他

- 拉丁美洲、中東和非洲

- 巴西

- 南非

- 沙烏地阿拉伯

- 其他

第7章 競爭格局

- 介紹

- 關鍵成功策略

- 前 10 家公司的產品映射

- 競爭儀錶板

- 競爭熱圖

- 2023年主要企業的定位

第8章 公司簡介

- NextEra Energy, Inc.

- Enel Spa

- Iberdrola SA

- Canadian Solar

- First Solar, Inc.

- SunPower Corporation

- ACCIONA Energia

- Suzlon Energy Limited

- Adani Group.

- Tata Power Renewable Energy Limited

The global clean energy infrastructure market was valued at $0.7 trillion in 2023 and is estimated to reach $1.8 trillion by 2033, growing at a CAGR of 9.2% from 2024 to 2033.

Clean energy infrastructure refers to the network of systems, facilities, and technologies that generate, store, distribute, and manage energy from renewable and environmentally friendly sources such as wind, solar, hydropower, geothermal, and bioenergy. These infrastructures play a pivotal role in the global shift toward sustainable energy systems, designed to mitigate the environmental impacts of traditional fossil fuel-based energy production. This shift is driven by growing concerns about climate change, the depletion of natural resources, and the need for energy security. Clean energy infrastructure is essential for achieving global targets for reducing carbon emissions and promoting economic and social development without harming the environment.

Technological advancements are playing a pivotal role in transforming clean energy infrastructure, driving both efficiency and affordability. One of the key areas of innovation is energy storage. Advances in battery technology, particularly lithium-ion and next-generation solutions such as solid-state and flow batteries, are enabling more reliable storage of renewable energy. This allows for better management of intermittent energy sources like wind and solar by ensuring that surplus energy can be stored and deployed during periods of low generation. Large-scale energy storage systems are increasingly being integrated into power grids, stabilizing supply and enabling the shift to 24/7 clean energy generation. According to the International Renewable Energy Agency, in 2022, the global hydropower installed capacity reached 1,393 gigawatts (GW), representing a rise of 2.19% compared to 2021. The hydropower installed capacity is expected to grow with the upcoming hydro projects and technological advancements. All these factors are expected to drive the growth of the global clean energy infrastructure market during the forecast period.

However, High initial investment costs present a significant challenge to the expansion of clean energy infrastructure. The construction of renewable energy projects such as solar plants, wind farms, and the necessary upgrades to existing energy grids demands substantial upfront capital. These costs encompass not only the procurement of advanced technology but also the installation, land acquisition, and integration with the broader power grid. For regions with limited access to financing, particularly developing countries, securing the necessary funds to initiate such projects can be a formidable barrier. This financial hurdle often delays the adoption of clean energy, despite the long-term economic and environmental benefits these technologies can deliver.

The private sector is reluctant to invest heavily in renewable energy infrastructure without strong government incentives or assurances of profitability. Traditional fossil fuel energy sources often have established supply chains and infrastructure, making them more financially attractive in the short term. As a result, renewable energy projects are perceived as riskier investments due to their higher initial costs and the reliance on long-term returns, which can be influenced by fluctuating market conditions and policy shifts. All these factors hamper the global clean energy infrastructure market growth.

The rise of microgrids and distributed generation technologies allows energy production and consumption at the local level, reducing dependence on large, centralized energy grids. This shift is particularly attractive in regions with unstable energy infrastructure or in areas prone to natural disasters, where decentralized systems offer energy security and resilience. Additionally, decentralized systems are empowering communities and businesses to generate, store, and manage their energy needs, creating a new market for clean energy products and services. In December 2022, Bangalore Electricity Supply Company Limited (BESCOM) launched Phase 2 of its grid-connected rooftop solar initiative. This phase aimed at expanding the installation of solar panels, with BESCOM receiving a directive from the Union Ministry of New and Renewable Energy (MNRE) to deploy 10 MW of solar capacity. This effort is part of a broader strategy to encourage distributed energy generation. In November 2022, Michigan's distributed generation program experienced a 37% increase, welcoming 3,709 new customers. This growth brought the total number of participants to 14,262 and the total number of distributed generation installations to 14,446. The program primarily focused on solar energy, allowing customers to generate their own electricity and reduce their household energy expenses. All these factors are anticipated to offer new growth opportunities for the global clean energy infrastructure market.

The clean energy infrastructure market is segmented into infrastructure type, end-use, and region. On the basis of infrastructure type, the market is classified into power generation facilitates, energy storage systems, transmission, and distribution networks. On the basis of end-use, the market is classified into residential, commercial, and industrial. Based on region the market is divided into North America, Europe, Asia-Pacific, and LAMEA.

On the basis of infrastructure type, the power generation facilities segment is the dominated the market representing the CAGR of 9.2% during the forecast period. Clean energy infrastructure plays a vital role in power generation facilities, enabling the transition from fossil fuels to sustainable energy sources. In utility-scale solar power plants, the use of advanced technology such as solar trackers and energy storage systems enhances efficiency. Solar trackers allow PV panels to follow the sun's path, maximizing energy capture throughout the day. Energy storage, in the form of batteries, addresses the intermittency issue by storing excess electricity for use during cloudy periods or nighttime.

On the basis of end-use, the industrial segment is the dominated the market representing the CAGR of 8.9% during the forecast period. One of the foremost strategies in the industrial sector's clean energy transition is the integration of renewable energy sources. Solar and wind power have emerged as prominent choices due to their scalability and decreasing costs. Many industrial facilities are now installing solar panels on their rooftops or within their premises to harness solar energy. In addition to solar and wind, biomass energy is gaining traction in industries with access to organic waste or by-products. Biomass can be converted into electricity or heat, offering a sustainable alternative to traditional energy sources. Industries such as paper, food processing, and agriculture, which generate significant amounts of organic waste, are particularly well-positioned to benefit from biomass energy systems.

Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, Middle East, and Latin America. The Asia-Pacific region accounted for more than one-third of the global clean energy infrastructure market share in 2023 and is expected to maintain its dominance during the forecast period. Asia-Pacific is the world's manufacturing hub for key clean energy components. China dominates the global production of solar panels, producing a significant share of the world's supply. The country's extensive manufacturing capabilities extend to wind turbines and batteries, with China and South Korea leading in the production of lithium-ion batteries crucial for energy storage and electric vehicles.

The major players operating in the clean energy infrastructure market include NextEra Energy, Inc., Enel Spa, Iberdrola, Canadian Solar, First Solar, SunPower Corporation, ACCIONA ENERGIA, Suzlon Energy Limited, Adani Group., and Tata Power.

Key findings of the study

- On the basis of infrastructure type, power generation facilities are the fastest growing segment in the market representing the CAGR of 9.2% during the forecast period.

- On the basis of end-use, commercial is the fastest growing segment in the market representing the CAGR of 9.6% during the forecast period.

- Region-wise, Asia-Pacific has the highest share in 2022 in terms of revenue.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the clean energy infrastructure market analysis from 2023 to 2033 to identify the prevailing clean energy infrastructure market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the clean energy infrastructure market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global clean energy infrastructure market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Manufacturing Capacity

- Capital Investment breakdown

- Consumer Buying Behavior Analysis

- Investment Opportunities

- Supply Chain Analysis & Vendor Margins

- Upcoming/New Entrant by Regions

- Technology Trend Analysis

- Distributor margin Analysis

- Go To Market Strategy

- Market share analysis of players by products/segments

- New Product Development/ Product Matrix of Key Players

- Regulatory Guidelines

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Brands Share Analysis

- Expanded list for Company Profiles

- Historic market data

- Import Export Analysis/Data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- Market share analysis of players at global/region/country level

- Product Consumption Analysis

- SWOT Analysis

Key Market Segments

By Infrastructure Type

- Transmission

- Distribution Networks

- Power Generation Facilities

- Energy Storage Systems

By End-Use

- Residential

- Commercial

- Industrial

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- Italy

- Spain

- UK

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- South Africa

- Saudi Arabia

- Rest of LAMEA

Key Market Players:

- ACCIONA Energia

- Adani Group.

- Canadian Solar

- Enel Spa

- First Solar, Inc.

- Iberdrola S.A.

- NextEra Energy, Inc.

- SunPower Corporation

- Suzlon Energy Limited

- Tata Power Renewable Energy Limited

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Moderate bargaining power of suppliers

- 3.3.2. Moderate threat of new entrants

- 3.3.3. Moderate threat of substitutes

- 3.3.4. Moderate intensity of rivalry

- 3.3.5. Moderate bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Rapid developments in energy storage, smart grids, and renewable energy technologies

- 3.4.1.2. Increase in government policies and incentives

- 3.4.2. Restraints

- 3.4.2.1. High Initial Investment Costs

- 3.4.3. Opportunities

- 3.4.3.1. Increase in demand for decentralized energy systems

- 3.4.1. Drivers

- 3.5. Value Chain Analysis

- 3.6. Regulatory Guidelines

CHAPTER 4: CLEAN ENERGY INFRASTRUCTURE MARKET, BY INFRASTRUCTURE TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Power Generation Facilities

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Energy Storage Systems

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Transmission

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Distribution Networks

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

CHAPTER 5: CLEAN ENERGY INFRASTRUCTURE MARKET, BY END-USE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Residential

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Commercial

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Industrial

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

CHAPTER 6: CLEAN ENERGY INFRASTRUCTURE MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by Infrastructure Type

- 6.2.3. Market size and forecast, by End-Use

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Market size and forecast, by Infrastructure Type

- 6.2.4.1.2. Market size and forecast, by End-Use

- 6.2.4.2. Canada

- 6.2.4.2.1. Market size and forecast, by Infrastructure Type

- 6.2.4.2.2. Market size and forecast, by End-Use

- 6.2.4.3. Mexico

- 6.2.4.3.1. Market size and forecast, by Infrastructure Type

- 6.2.4.3.2. Market size and forecast, by End-Use

- 6.3. Europe

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by Infrastructure Type

- 6.3.3. Market size and forecast, by End-Use

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. Germany

- 6.3.4.1.1. Market size and forecast, by Infrastructure Type

- 6.3.4.1.2. Market size and forecast, by End-Use

- 6.3.4.2. France

- 6.3.4.2.1. Market size and forecast, by Infrastructure Type

- 6.3.4.2.2. Market size and forecast, by End-Use

- 6.3.4.3. Italy

- 6.3.4.3.1. Market size and forecast, by Infrastructure Type

- 6.3.4.3.2. Market size and forecast, by End-Use

- 6.3.4.4. Spain

- 6.3.4.4.1. Market size and forecast, by Infrastructure Type

- 6.3.4.4.2. Market size and forecast, by End-Use

- 6.3.4.5. UK

- 6.3.4.5.1. Market size and forecast, by Infrastructure Type

- 6.3.4.5.2. Market size and forecast, by End-Use

- 6.3.4.6. Rest of Europe

- 6.3.4.6.1. Market size and forecast, by Infrastructure Type

- 6.3.4.6.2. Market size and forecast, by End-Use

- 6.4. Asia-Pacific

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by Infrastructure Type

- 6.4.3. Market size and forecast, by End-Use

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Market size and forecast, by Infrastructure Type

- 6.4.4.1.2. Market size and forecast, by End-Use

- 6.4.4.2. Japan

- 6.4.4.2.1. Market size and forecast, by Infrastructure Type

- 6.4.4.2.2. Market size and forecast, by End-Use

- 6.4.4.3. India

- 6.4.4.3.1. Market size and forecast, by Infrastructure Type

- 6.4.4.3.2. Market size and forecast, by End-Use

- 6.4.4.4. South Korea

- 6.4.4.4.1. Market size and forecast, by Infrastructure Type

- 6.4.4.4.2. Market size and forecast, by End-Use

- 6.4.4.5. Australia

- 6.4.4.5.1. Market size and forecast, by Infrastructure Type

- 6.4.4.5.2. Market size and forecast, by End-Use

- 6.4.4.6. Rest of Asia-Pacific

- 6.4.4.6.1. Market size and forecast, by Infrastructure Type

- 6.4.4.6.2. Market size and forecast, by End-Use

- 6.5. LAMEA

- 6.5.1. Key market trends, growth factors and opportunities

- 6.5.2. Market size and forecast, by Infrastructure Type

- 6.5.3. Market size and forecast, by End-Use

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Market size and forecast, by Infrastructure Type

- 6.5.4.1.2. Market size and forecast, by End-Use

- 6.5.4.2. South Africa

- 6.5.4.2.1. Market size and forecast, by Infrastructure Type

- 6.5.4.2.2. Market size and forecast, by End-Use

- 6.5.4.3. Saudi Arabia

- 6.5.4.3.1. Market size and forecast, by Infrastructure Type

- 6.5.4.3.2. Market size and forecast, by End-Use

- 6.5.4.4. Rest of LAMEA

- 6.5.4.4.1. Market size and forecast, by Infrastructure Type

- 6.5.4.4.2. Market size and forecast, by End-Use

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product mapping of top 10 player

- 7.4. Competitive dashboard

- 7.5. Competitive heatmap

- 7.6. Top player positioning, 2023

CHAPTER 8: COMPANY PROFILES

- 8.1. NextEra Energy, Inc.

- 8.1.1. Company overview

- 8.1.2. Key executives

- 8.1.3. Company snapshot

- 8.1.4. Operating business segments

- 8.1.5. Product portfolio

- 8.1.6. Business performance

- 8.1.7. Key strategic moves and developments

- 8.2. Enel Spa

- 8.2.1. Company overview

- 8.2.2. Key executives

- 8.2.3. Company snapshot

- 8.2.4. Operating business segments

- 8.2.5. Product portfolio

- 8.2.6. Business performance

- 8.2.7. Key strategic moves and developments

- 8.3. Iberdrola S.A.

- 8.3.1. Company overview

- 8.3.2. Key executives

- 8.3.3. Company snapshot

- 8.3.4. Operating business segments

- 8.3.5. Product portfolio

- 8.3.6. Business performance

- 8.3.7. Key strategic moves and developments

- 8.4. Canadian Solar

- 8.4.1. Company overview

- 8.4.2. Key executives

- 8.4.3. Company snapshot

- 8.4.4. Operating business segments

- 8.4.5. Product portfolio

- 8.4.6. Business performance

- 8.4.7. Key strategic moves and developments

- 8.5. First Solar, Inc.

- 8.5.1. Company overview

- 8.5.2. Key executives

- 8.5.3. Company snapshot

- 8.5.4. Operating business segments

- 8.5.5. Product portfolio

- 8.5.6. Business performance

- 8.5.7. Key strategic moves and developments

- 8.6. SunPower Corporation

- 8.6.1. Company overview

- 8.6.2. Key executives

- 8.6.3. Company snapshot

- 8.6.4. Operating business segments

- 8.6.5. Product portfolio

- 8.6.6. Business performance

- 8.7. ACCIONA Energia

- 8.7.1. Company overview

- 8.7.2. Key executives

- 8.7.3. Company snapshot

- 8.7.4. Operating business segments

- 8.7.5. Product portfolio

- 8.7.6. Business performance

- 8.8. Suzlon Energy Limited

- 8.8.1. Company overview

- 8.8.2. Key executives

- 8.8.3. Company snapshot

- 8.8.4. Operating business segments

- 8.8.5. Product portfolio

- 8.8.6. Business performance

- 8.8.7. Key strategic moves and developments

- 8.9. Adani Group.

- 8.9.1. Company overview

- 8.9.2. Key executives

- 8.9.3. Company snapshot

- 8.9.4. Operating business segments

- 8.9.5. Product portfolio

- 8.9.6. Business performance

- 8.10. Tata Power Renewable Energy Limited

- 8.10.1. Company overview

- 8.10.2. Key executives

- 8.10.3. Company snapshot

- 8.10.4. Operating business segments

- 8.10.5. Product portfolio

- 8.10.6. Business performance

- 8.10.7. Key strategic moves and developments

2025年清潔能源技術全球市場報告

2025年清潔能源技術全球市場報告 清潔能源市場:2033 年市場分析與預測 - 按類型、按產品、按服務、按技術、按組件、按應用、按部署、按最終用戶、按安裝類型、按解決方案火管冷凝低溫工業鍋爐市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測冷卻儀表市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測2025年至2034年冷凝式火管低溫工業鍋爐市場機會、成長動力、產業趨勢分析與預測商用冷卻表市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年冷凝式火管化學鍋爐市場機會、成長動力、產業趨勢分析及2024年至2032年預測超音波冷卻表市場、機會、成長動力、產業趨勢分析與預測,2024-2032

清潔能源市場:2033 年市場分析與預測 - 按類型、按產品、按服務、按技術、按組件、按應用、按部署、按最終用戶、按安裝類型、按解決方案火管冷凝低溫工業鍋爐市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測冷卻儀表市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測2025年至2034年冷凝式火管低溫工業鍋爐市場機會、成長動力、產業趨勢分析與預測商用冷卻表市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年冷凝式火管化學鍋爐市場機會、成長動力、產業趨勢分析及2024年至2032年預測超音波冷卻表市場、機會、成長動力、產業趨勢分析與預測,2024-2032 全球清潔能源技術市場,2024-2028

全球清潔能源技術市場,2024-2028 2030 年清潔能源市場預測:按類型、技術、應用、最終用戶和地區分類的全球分析

2030 年清潔能源市場預測:按類型、技術、應用、最終用戶和地區分類的全球分析