|

市場調查報告書

商品編碼

1927656

全球國防3D列印市場(2026-2036)Global Defense 3D Printing Market 2026-2036 |

||||||

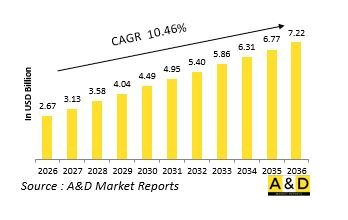

據估計,2026年全球國防3D列印市場規模為26.7億美元,預計到2036年將達到72.2億美元,2026年至2036年的複合年增長率(CAGR)為10.46%。

全球國防3D列印簡介

全球國防3D列印正在成為一種新興的製造方法,它正在改變軍事零件的設計、製造和維護方式。 與傳統生產方法不同,積層製造逐層建造零件,能夠實現使用傳統技術難以或不切實際的複雜幾何形狀。在國防領域,這項技術支援快速原型製作、客製化零件生產以及在作戰環境中按需製造。國防機構越來越重視將 3D 列印作為提高戰備水準和減少對冗長供應鏈依賴的戰略工具。該技術加速了設計迭代,實現了組件測試和改進,同時縮短了開發週期。它還支援輕量化結構的生產,從而在不犧牲強度的前提下提昇平台性能。在空中、陸地和海上領域,3D 列印技術透過實現備件和關鍵作戰組件的本地化生產,為資產維護做出了貢獻。其日益普及反映了向靈活、反應迅速的製造模式的轉變,這種轉變符合現代國防對速度、適應性和作戰韌性的要求。

科技對全球國防領域 3D 列印的影響

技術進步正在擴大 3D 列印在國防應用領域的範圍和可靠性。 金屬積層製造技術的進步使得高強度零件的生產成為可能,這些零件可用於結構和承重應用。列印精度的提高提升了尺寸精度和表面質量,滿足了嚴格的國防規範。材料科學的創新催生了專為嚴苛運作環境設計的特殊合金和複合材料。整合式數位設計工具實現了從建模到生產的無縫過渡,並支援快速修復。諸如製程監控等品質保證技術提高了一致性並降低了缺陷風險。安全的數位化工作流程保護了分散式製造中的敏感設計資料。這些發展使得3D列印從原型製作工具演變為支援作戰部署的生產技術。如今,它在提升性能、減少材料浪費以及快速響應國防平台不斷變化的作戰需求方面發揮著重要作用。

全球國防領域3D列印的關鍵驅動因素

國防領域採用3D列印技術的主要驅動因素是作戰彈性、供應鏈韌性和成本效益。軍事機構需要快速取得替換零件,以最大限度地減少設備停機時間。 現場或附近製造減少了對集中式供應商和長途物流路線的依賴。平台現代化專案促進了先進製造技術的應用,這些技術支援輕量化和最佳化設計。預算效率目標推動了減少模具需求和材料浪費的技術發展。小批量、複雜零件的生產能力與國防採購模式高度契合。勞動力技能發展和數位轉型措施進一步支持了積層製造技術融入國防生態系統。這些驅動因素體現了國防製造對敏捷性、永續性和應變能力的戰略關注。 本報告探索並分析了全球國防3D列印市場,提供了影響該市場的技術資訊、未來十年的預測以及區域趨勢。

目錄

國防3D列印市場報告定義

國防3D列印市場區隔

按應用

按地區

按元件

未來十年國防3D列印市場分析

國防3D列印市場技術

全球國防3D列印市場預測

區域國防3D列印市場趨勢及預測

北美

驅動因素、限制因素與挑戰

PEST分析

市場預測及情境分析

主要公司

供應商層級概覽

公司基準分析

歐洲

中東

亞太地區

南美洲

國防3D列印市場國家分析

美國

國防項目

最新資訊

專利

當前市場技術成熟度

市場預測及情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防3D列印市場機會矩陣

專家對國防3D列印市場的看法

結論

關於航空和國防市場報告

The Global Defense 3D Printing market is estimated at USD 2.67 billion in 2026, projected to grow to USD 7.22 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 10.46% over the forecast period 2026-2036.

Introduction to Global Defense 3D Printing

Global defense three dimensional printing has emerged as a transformative manufacturing approach that reshapes how military components are designed, produced, and sustained. Unlike conventional fabrication methods, additive manufacturing builds parts layer by layer, enabling complex geometries that are difficult or impractical to achieve through traditional techniques. In defense applications, this capability supports rapid prototyping, customized part production, and on-demand manufacturing in operational environments. Defense organizations increasingly view three dimensional printing as a strategic tool for improving readiness and reducing dependency on extended supply chains. The technology enables faster design iteration, allowing engineers to test and refine components with shorter development cycles. It also supports production of lightweight structures that enhance platform performance without compromising strength. Across air, land, and naval domains, three dimensional printing contributes to equipment sustainment by enabling localized manufacturing of spares and mission-critical components. Its growing adoption reflects a shift toward flexible, responsive manufacturing models that align with modern defense requirements for speed, adaptability, and operational resilience.

Technology Impact in Global Defense 3D Printing

Technological progress has expanded the scope and reliability of three dimensional printing within defense applications. Advances in metal additive manufacturing enable production of high-strength components suitable for structural and load-bearing roles. Improved printing precision enhances dimensional accuracy and surface quality, meeting stringent defense specifications. Material science innovation has introduced specialized alloys and composites designed for extreme operating conditions. Integrated digital design tools allow seamless transition from modeling to production while supporting rapid modification. Quality assurance technologies such as in-process monitoring improve consistency and reduce defect risk. Secure digital workflows protect sensitive design data during distributed manufacturing. These developments collectively elevate three dimensional printing from a prototyping tool to a production-capable technology that supports operational deployment. The technology now plays a role in improving performance, reducing material waste, and enabling faster response to evolving mission needs across defense platforms.

Key Drivers in Global Defense 3D Printing

The adoption of three dimensional printing in defense is driven by operational flexibility, supply chain resilience, and cost efficiency objectives. Military organizations seek faster access to replacement parts to minimize equipment downtime. On-site or near-site manufacturing reduces dependence on centralized suppliers and long logistics routes. Platform modernization programs encourage use of advanced manufacturing methods that support lightweight and optimized designs. Budget efficiency goals promote technologies that reduce tooling requirements and material waste. The ability to produce low-volume, high-complexity components aligns well with defense procurement patterns. Workforce skill development and digital transformation initiatives further support integration of additive manufacturing into defense ecosystems. These drivers reflect a strategic emphasis on agility, sustainability, and responsiveness in defense manufacturing.

Regional Trends in Global Defense 3D Printing

Regional trends in defense three dimensional printing reflect differences in industrial maturity and operational focus. Technologically advanced regions invest in large-scale metal printing and qualification standards for mission-critical components. Regions emphasizing expeditionary operations explore deployable printing units for field sustainment. Emerging defense markets adopt three dimensional printing to support indigenous production and reduce import reliance. Collaborative research initiatives between defense agencies and industry are common in regions prioritizing innovation. Naval regions focus on corrosion-resistant materials, while aerospace-oriented regions prioritize weight reduction and performance optimization. These regional patterns demonstrate how additive manufacturing adoption adapts to localized defense strategies while supporting global trends toward flexible production and operational independence.

Key Defense 3D Printing Program:

To overcome manufacturing constraints that have restricted output for a critical U.S. defense weapon system, Velo3D has signed an Other Transaction Agreement with the U.S. Department of War's Defense Innovation Unit. Valued at $32.6 million, the agreement supports an established program under DIU's Foundry for Operational Readiness and Global Effects initiative, referred to as Project FORGE. Project FORGE focuses on identifying and implementing solutions to long-standing production challenges across the U.S. defense industrial base. These challenges, largely stemming from conventional manufacturing processes and legacy platforms, have constrained production capacity and hindered the rapid scaling of a vital Department of War weapon system. Under this agreement, Velo3D will work alongside DIU, the U.S. Navy, and a leading defense prime contractor to develop, test, and qualify additively manufactured components aimed at eliminating these bottlenecks and increasing overall production throughput.

Table of Contents

Defense 3D Printing Market - Table of Contents

Defense 3D Printing Market Report Definition

Defense 3D Printing Market Segmentation

By Application

By Region

By Components

Defense 3D Printing Market Analysis for next 10 Years

The 10-year Defense 3D Printing Market analysis would give a detailed overview of Defense 3D Printing Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense 3D Printing Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense 3D Printing Market Forecast

The 10-year Defense 3D Printing Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense 3D Printing Market Trends & Forecast

The regional Defense 3D Printing Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense 3D Printing Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense 3D Printing Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense 3D Printing Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Application, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Components, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Application, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Components, 2026-2036

List of Figures

- Figure 1: Global Defense 3D Printing Market Forecast, 2026-2036

- Figure 2: Global Defense 3D Printing Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense 3D Printing Market Forecast, By Application, 2026-2036

- Figure 4: Global Defense 3D Printing Market Forecast, By Components, 2026-2036

- Figure 5: North America, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 16: France, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 32: India, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 34: China, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense 3D Printing Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense 3D Printing Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense 3D Printing Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense 3D Printing Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense 3D Printing Market, By Application (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense 3D Printing Market, By Application (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense 3D Printing Market, By Components (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense 3D Printing Market, By Components (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense 3D Printing Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense 3D Printing Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense 3D Printing Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense 3D Printing Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense 3D Printing Market, By Application, 2026-2036

- Figure 59: Scenario 1, Defense 3D Printing Market, By Components, 2026-2036

- Figure 60: Scenario 2, Defense 3D Printing Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense 3D Printing Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense 3D Printing Market, By Application, 2026-2036

- Figure 63: Scenario 2, Defense 3D Printing Market, By Components, 2026-2036

- Figure 64: Company Benchmark, Defense 3D Printing Market, 2026-2036

航太3D列印市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

航太3D列印市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 航太領域3D列印-全球產業規模、佔有率、趨勢、機會及預測(按應用、材料、印表機技術、地區和競爭格局分類,2021-2031年)

航太領域3D列印-全球產業規模、佔有率、趨勢、機會及預測(按應用、材料、印表機技術、地區和競爭格局分類,2021-2031年) 航太3D列印市場規模、佔有率和成長分析(按產品、技術、平台、最終產品、最終用戶、應用和地區分類)-產業預測(2026-2033年)

航太3D列印市場規模、佔有率和成長分析(按產品、技術、平台、最終產品、最終用戶、應用和地區分類)-產業預測(2026-2033年) 不銹鋼填充聚合物長絲市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場預測(2025-2033 年)金屬填充聚合物長絲市場規模、佔有率和趨勢分析報告 - 按金屬、最終用途、地區和細分市場預測:2025-2033年

不銹鋼填充聚合物長絲市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場預測(2025-2033 年)金屬填充聚合物長絲市場規模、佔有率和趨勢分析報告 - 按金屬、最終用途、地區和細分市場預測:2025-2033年 航太和國防市場 3D 列印(按技術、材料、服務模式、軟體和應用)—2025-2032 年全球預測航太領域3D列印市場:依材料、技術、應用、最終用途產業及印表機類型分類-2025-2032年全球預測

航太和國防市場 3D 列印(按技術、材料、服務模式、軟體和應用)—2025-2032 年全球預測航太領域3D列印市場:依材料、技術、應用、最終用途產業及印表機類型分類-2025-2032年全球預測 建築規模 3D 列印聚合物長絲市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測航太和國防領域的 3D 列印:全球預測(2025-2030 年)

建築規模 3D 列印聚合物長絲市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測航太和國防領域的 3D 列印:全球預測(2025-2030 年) 航太3D列印的全球市場的評估:各平台,各用途,各材料類型,各地區,機會,預測(2018年~2032年)

航太3D列印的全球市場的評估:各平台,各用途,各材料類型,各地區,機會,預測(2018年~2032年)