|

市場調查報告書

商品編碼

1936608

海底立管市場機會、成長要素、產業趨勢分析及2026年至2035年預測Subsea Risers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

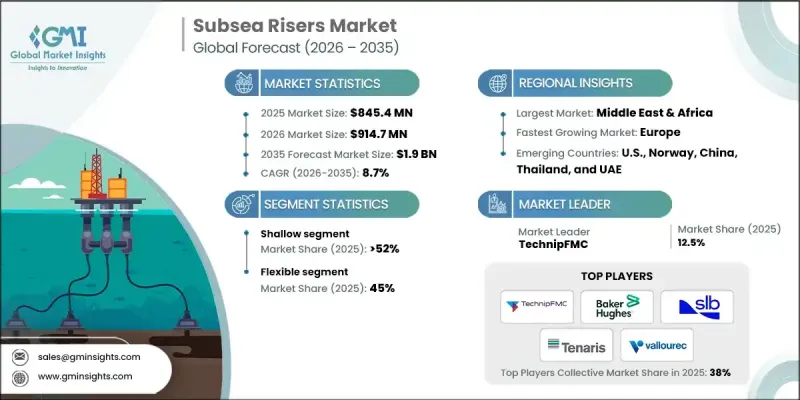

全球海底立管市場預計到 2025 年將達到 8.454 億美元,到 2035 年將達到 19 億美元,年複合成長率為 8.7%。

市場擴張的驅動力來自對海上和深水能源開發資本投入的增加,以及應對在各種海底地質環境下油氣開採相關的營運和技術複雜性的轉變。對深水和超深水蘊藏量開發的日益重視促使營運商重新調整其海上開發策略,尋求技術先進且資本密集的計劃,以彌補陸上和淺水區產量下降的影響。浮體式生產設施的日益普及以及對可靠的油氣運輸解決方案(用於將油氣從海底儲存輸送到陸上設施)的需求不斷成長,進一步推動了市場需求。此外,全球能源消耗的成長、易開採蘊藏量的減少以及旨在降低故障率和縮短維護週期的尖端材料和結構設計政策舉措,都在影響市場走向。製造商在保持安全性和性能標準的同時,透過改進海底生產系統的設計和製造程序,日益重視成本最佳化。持續的技術進步,包括材料創新、耐腐蝕性的提高以及數位化監測和預測性維護工具的整合,正在進一步加速海上開發領域的應用。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 8.454億美元 |

| 預測金額 | 19億美元 |

| 複合年成長率 | 8.7% |

淺水油氣市場在2025年佔據52%的市場佔有率,預計2026年至2035年將以8%的複合年成長率成長。該市場的成長主要得益於老舊海上資產開發活動的重啟以及對經濟效益良好的探勘項目的日益重視。此外,為加強供應安全而增加的近海能源區塊投資、早期生產解決方案的廣泛應用以及分階段的油田擴建,共同支撐著該市場的成長和長期利用率。

預計2035年,鋼製懸索立管市場規模將達3.35億美元。海上石油鑽探活動的增加、深層油氣藏投資的成長以及下游需求的不斷擴大,都是推動鋼製懸鍊式立管市場發展的主要因素。營運商致力於擴大產能以滿足能源需求,同時不斷提高立管設計的效率和耐久性,這也持續推動該市場的成長。

預計到2025年,北美海底立管市場將佔據75.3%的市場佔有率,市場規模達到9,000萬美元。市場成長得益於海上鑽井作業自動化和數位化程度的提高、有利的法規結構以及持續的探勘和生產活動。業內相關人員正在加強合作,以實施先進的海底技術、最佳化海上作業流程,並將海上開發與更廣泛的能源轉型策略相協調。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 影響價值鏈的關鍵因素

- 中斷

- 監管環境

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 海底立管成本結構分析

- 新的機會與趨勢

- 利用物聯網技術實現數位轉型

- 拓展新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 策略舉措

- 重要夥伴關係與合作

- 重大併購活動

- 產品創新與新產品發布

- 市場擴大策略

- 競爭標竿分析

- 戰略儀錶板

- 創新與永續性格局

第5章 依深度分類的市場規模及預測(2022-2035年)

- 淺層

- SCR

- 靈活的

- 其他

- 深層

- SCR

- 靈活的

- 其他

- 超深

- SCR

- 靈活的

- 其他

第6章 2022-2035年依產品分類的市場規模及預測

- SCR

- 靈活的

- 其他

第7章 2022-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 挪威

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 印尼

- 馬來西亞

- 泰國

- 澳洲

- 中東和非洲

- 安哥拉

- 奈及利亞

- 埃及

- 卡達

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 拉丁美洲

- 巴西

第8章 公司簡介

- 2H Offshore Engineering Ltd.

- Alleima

- Aquaterra Energy Limited

- ArcelorMittal

- Baker Hughes Company

- Balmoral Comtec Ltd

- HOHN GROUP

- Hunting PLC

- John Wood Group PLC

- NOV

- OCTALSTEEL

- Oil States

- OneSubsea

- SLB

- Subsea 7

- TechnipFMC plc

- Tenaris

- Vallourec

- Weatherford

- Worldwide Oilfield Machine(WOM)

The Global Subsea Risers Market was valued at USD 845.4 million in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 1.9 billion by 2035.

Market expansion is supported by rising capital allocation toward offshore and deepwater energy developments, alongside a growing shift toward addressing the operational and engineering complexities associated with hydrocarbon extraction across varied subsea geological environments. Increasing focus on unlocking deepwater and ultra-deepwater reserves is reshaping offshore development strategies, as operators pursue technically advanced and capital-intensive projects to offset declining onshore and shallow-water production. The rising deployment of floating production systems and the growing requirement for dependable flow assurance solutions to transport hydrocarbons from seabed reservoirs to surface facilities are strengthening demand. In addition, higher global energy consumption, reduced availability of easily accessible reserves, and policy initiatives promoting advanced materials and structural designs that lower failure rates and maintenance frequency are influencing market direction. Manufacturers are increasingly prioritizing cost optimization by refining designs and manufacturing processes for subsea production systems while maintaining safety and performance standards. Ongoing technological progress, including material innovation, improved corrosion resistance, and the integration of digital monitoring and predictive maintenance tools, is further accelerating adoption across offshore developments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $845.4 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 8.7% |

The shallow-water segment accounted for 52% share in 2025 and is forecast to grow at a CAGR of 8% from 2026 to 2035. Growth in this segment is driven by renewed development activity in aging offshore assets and a growing emphasis on economically viable exploration programs. Increased investments in nearshore energy blocks to enhance supply stability, combined with rising adoption of early-production solutions and incremental field expansions, continue to support segment performance and long-term utilization.

The steel catenary riser segment is expected to reach USD 335 million by 2035. Rising offshore oil and gas extraction activity, increasing investment in deeper hydrocarbon fields, and growing downstream demand are driving adoption. Operators are focusing on expanding production capacity to meet energy demand while advancing riser design efficiency and durability, which continues to support segment expansion.

North America Subsea Risers Market held 75.3% share in 2025 and generated USD 90 million. Market growth is supported by increased automation and digital integration across offshore drilling operations, favorable regulatory frameworks, and sustained exploration and production activity. Industry participants are increasingly collaborating to deploy advanced subsea technologies, optimize offshore processes, and align offshore developments with broader energy transition strategies.

Key companies active in the Global Subsea Risers Market include TechnipFMC plc, SLB, Subsea 7, Baker Hughes Company, NOV, OneSubsea, Vallourec, Tenaris, ArcelorMittal, John Wood Group PLC, Weatherford, Oil States, Hunting PLC, Alleima, Aquaterra Energy Limited, Balmoral Comtec Ltd, 2H Offshore Engineering Ltd., Worldwide Oilfield Machine (WOM), OCTALSTEEL, and HOHN GROUP. Companies operating in the Subsea Risers Market are strengthening their market position through continuous technology innovation, strategic partnerships, and expansion of engineering capabilities. Leading players are investing in advanced materials, digital monitoring systems, and predictive maintenance technologies to enhance reliability and lifecycle performance. Collaboration with offshore operators enables customized riser solutions for complex field conditions. Firms are also focusing on cost-efficient manufacturing, modular designs, and localized production to remain competitive.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Depth trends

- 2.4 Product trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of subsea risers

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Depth, 2022 - 2035 (‘000 Feet & USD Million)

- 5.1 Key trends

- 5.2 Shallow

- 5.2.1 SCR

- 5.2.2 Flexible

- 5.2.3 Others

- 5.3 Deep

- 5.3.1 SCR

- 5.3.2 Flexible

- 5.3.3 Others

- 5.4 Ultra-Deep

- 5.4.1 SCR

- 5.4.2 Flexible

- 5.4.3 Others

Chapter 6 Market Size and Forecast, By Product, 2022 - 2035 (‘000 Feet & USD Million)

- 6.1 Key trends

- 6.2 SCR

- 6.3 Flexible

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (‘000 Feet & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Norway

- 7.3.3 Netherlands

- 7.3.4 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Indonesia

- 7.4.4 Malaysia

- 7.4.5 Thailand

- 7.4.6 Australia

- 7.5 Middle East & Africa

- 7.5.1 Angola

- 7.5.2 Nigeria

- 7.5.3 Egypt

- 7.5.4 Qatar

- 7.5.5 Saudi Arabia

- 7.5.6 UAE

- 7.6 Latin America

- 7.6.1 Brazil

Chapter 8 Company Profiles

- 8.1 2H Offshore Engineering Ltd.

- 8.2 Alleima

- 8.3 Aquaterra Energy Limited

- 8.4 ArcelorMittal

- 8.5 Baker Hughes Company

- 8.6 Balmoral Comtec Ltd

- 8.7 HOHN GROUP

- 8.8 Hunting PLC

- 8.9 John Wood Group PLC

- 8.10 NOV

- 8.11 OCTALSTEEL

- 8.12 Oil States

- 8.13 OneSubsea

- 8.14 SLB

- 8.15 Subsea 7

- 8.16 TechnipFMC plc

- 8.17 Tenaris

- 8.18 Vallourec

- 8.19 Weatherford

- 8.20 Worldwide Oilfield Machine (WOM)

油氣海底臍帶供應連系管、立管及輸油管市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、類型、地區及競爭格局分類,2021-2031年)海底儲槽市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年海底生產和處理系統市場-全球產業規模、佔有率、趨勢、機會及預測(依生產系統元件組件、處理系統類型、水深、地區及競爭格局分類,2021-2031年)

油氣海底臍帶供應連系管、立管及輸油管市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、類型、地區及競爭格局分類,2021-2031年)海底儲槽市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年海底生產和處理系統市場-全球產業規模、佔有率、趨勢、機會及預測(依生產系統元件組件、處理系統類型、水深、地區及競爭格局分類,2021-2031年) 全球深海臍帶供應連系管、立管及輸油管市場立管市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按類型(立管、立管套管和其他)、按水深(淺水、深水)、按地區和競爭,2020-2030F

全球深海臍帶供應連系管、立管及輸油管市場立管市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按類型(立管、立管套管和其他)、按水深(淺水、深水)、按地區和競爭,2020-2030F 海底生產與處理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)SURF 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型(海底、臍帶纜、立管、出油管)、深度(淺水、深水、超深水)、地區和競爭細分,2019 年- 2029F

海底生產與處理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)SURF 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型(海底、臍帶纜、立管、出油管)、深度(淺水、深水、超深水)、地區和競爭細分,2019 年- 2029F 臍帶市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

臍帶市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 海底臍帶供應連系管、立管和流線(衝浪)的全球市場 2024-2028淺水衝浪市場 - 按產品(臍帶纜、立管 {SCR、軟性管、其他}、管線)和預測,2024 年 - 2032 年

海底臍帶供應連系管、立管和流線(衝浪)的全球市場 2024-2028淺水衝浪市場 - 按產品(臍帶纜、立管 {SCR、軟性管、其他}、管線)和預測,2024 年 - 2032 年