|

市場調查報告書

商品編碼

1716597

前列腺癌治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Prostate Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

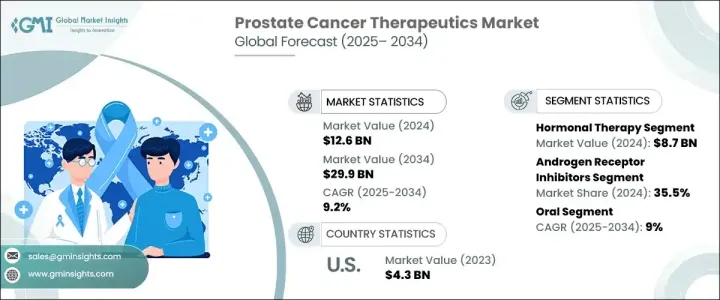

2024 年全球前列腺癌治療市場規模達 126 億美元,預計 2025 年至 2034 年的複合年成長率為 9.2%。市場正經歷顯著的發展勢頭,主要原因是全球前列腺癌發病率不斷上升,加上人們對早期診斷和有效治療方案的認知不斷提高。前列腺癌是男性最常見的癌症之一,醫療保健系統正致力於採用先進的治療方法來改善患者的治療效果。男性人口老化、發病率上升以及透過政府主導的措施和癌症倡導團體提高的患者意識繼續促進市場成長。

此外,精準醫療的創新以及基因組檢測、生物標記識別和人工智慧成像等先進診斷工具的整合正在徹底改變前列腺癌的檢測和治療計劃。製藥巨頭正大力投資研發,推出能夠有效針對抗藥性前列腺癌的新型藥物和個人化療法,為晚期患者帶來新的希望。此外,對聯合療法的重視和免疫療法的採用正在改變治療格局,為更安全、更有效的治療方式鋪平道路。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 126億美元 |

| 預測值 | 299億美元 |

| 複合年成長率 | 9.2% |

市場根據不同的治療方法進行細分,包括荷爾蒙療法、化學療法、免疫療法、標靶療法和其他治療方案。 2024年,荷爾蒙療法引領市場,創造87億美元的收入。荷爾蒙療法仍然是前列腺癌治療的基石,因為它透過降低雄性激素水平在控制疾病進展中發揮著至關重要的作用。眾所周知,這些激素,尤其是睪酮,會促進前列腺癌的生長。透過針對和抑制睪酮的產生,荷爾蒙療法可以顯著縮小腫瘤大小並緩解症狀,有助於提高患者的存活率。對晚期和抗藥性病例更有效的下一代荷爾蒙藥物的日益普及進一步鞏固了這一治療領域在全球市場的主導地位。

根據藥物類別,雄性激素受體抑制劑 (ARI) 在 2024 年佔據了 35.5% 的市場。 ARI 已成為晚期前列腺癌患者的重要治療選擇,尤其是那些對傳統雄性激素剝奪療法 (ADT) 不再有反應的患者。這些抑制劑透過阻斷雄激素受體訊號路徑發揮作用,從而阻止癌細胞利用雄激素生長。 ARI 在早期和晚期前列腺癌治療中的使用增加已顯示出改善的臨床結果,使其成為當前治療手段中不可或缺的一部分。預計,具有增強功效和安全性的新型 ARI 的推出也將在未來幾年推動其採用。

2024 年,北美佔據全球前列腺癌治療市場的 39.2% 佔有率。該地區的領導地位主要歸功於其先進的醫療保健基礎設施、尖端的癌症護理中心以及對腫瘤學研究的高度重視。高水準的公共和私人投資,以及製藥公司和研究機構之間的合作努力,正在不斷推動整個地區前列腺癌治療的創新。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 攝護腺癌盛行率不斷上升

- 技術進步

- 提高認知和篩檢項目

- 產業陷阱與挑戰

- 治療費用高昂

- 與治療相關的副作用

- 成長動力

- 成長潛力分析

- 監管格局

- 報銷場景

- 管道分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

- 差距分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按療法,2021 - 2034 年

- 主要趨勢

- 荷爾蒙療法

- 化療

- 免疫療法

- 標靶治療

- 其他療法

第6章:市場估計與預測:按藥物類別,2021 - 2034 年

- 主要趨勢

- 雄性激素受體抑制劑

- GnRH受體拮抗劑

- PARP抑制劑

- 免疫檢查點抑制劑

- 其他藥物類別

第7章:市場估計與預測:按管理路線,2021 - 2034 年

- 主要趨勢

- 口服

- 注射劑

第8章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 醫院藥房

- 實體店面

- 電子商務

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Astellas Pharma

- AstraZeneca

- Bayer

- Dendreon Pharmaceuticals

- Exelixis

- Ferring

- GlaxoSmithKline

- Ipsen Pharma

- Johnson & Johnson

- Novartis

- Pfizer

- Sanofi

- Sumitomo Pharma America

- Takeda Pharmaceutical

- Tolmar

The Global Prostate Cancer Therapeutics Market generated USD 12.6 billion in 2024 and is projected to expand at a CAGR of 9.2% from 2025 to 2034. The market is witnessing significant momentum, primarily driven by the growing prevalence of prostate cancer worldwide, coupled with increasing awareness around early diagnosis and effective treatment options. With prostate cancer ranking among the most common cancers in men, healthcare systems are focusing on adopting advanced therapeutics to improve patient outcomes. The aging male population, rising incidence rates, and a surge in patient awareness through government-led initiatives and cancer advocacy groups continue to foster market growth.

Moreover, innovations in precision medicine and the integration of advanced diagnostic tools like genomic testing, biomarker identification, and AI-powered imaging are revolutionizing prostate cancer detection and treatment planning. Pharmaceutical giants are heavily investing in research and development to introduce novel drugs and personalized therapies that can effectively target resistant forms of prostate cancer, offering renewed hope for patients with advanced disease stages. Additionally, the increased emphasis on combination therapies and the adoption of immunotherapies are transforming the therapeutic landscape, making way for safer and more efficient treatment modalities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.6 Billion |

| Forecast Value | $29.9 Billion |

| CAGR | 9.2% |

The market is segmented based on different therapeutic approaches, including hormonal therapy, chemotherapy, immunotherapy, targeted therapy, and other treatment options. In 2024, hormonal therapy led the market, generating USD 8.7 billion in revenue. Hormonal therapy remains a cornerstone in prostate cancer management as it plays a crucial role in controlling the disease's progression by lowering androgen hormone levels. These hormones, especially testosterone, are known to fuel prostate cancer growth. By targeting and suppressing testosterone production, hormonal therapies significantly reduce tumor size and alleviate symptoms, which contributes to improved patient survival rates. The growing adoption of next-generation hormonal agents that are more effective in advanced and resistant cases has further cemented the dominance of this therapeutic segment in the global market.

Based on drug classes, androgen receptor inhibitors (ARIs) accounted for 35.5% of the market share in 2024. ARIs have emerged as a vital treatment option for patients with advanced prostate cancer, especially those who no longer respond to traditional androgen deprivation therapy (ADT). These inhibitors work by blocking the androgen receptor signaling pathway, thereby preventing cancer cells from utilizing androgens for growth. The increased use of ARIs in both early and late-stage prostate cancer treatment has shown improved clinical outcomes, making them indispensable in the current therapeutic arsenal. The introduction of new ARIs with enhanced efficacy and safety profiles is also expected to boost their adoption over the coming years.

North America dominated the global prostate cancer therapeutics market with a 39.2% share in 2024. The region's leadership position is largely attributed to its advanced healthcare infrastructure, cutting-edge cancer care centers, and strong focus on oncology research. High levels of public and private investments, along with collaborative efforts between pharmaceutical companies and research institutions, are continuously propelling innovation in prostate cancer treatment across the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of prostate cancer

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects associated with treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hormonal therapy

- 5.3 Chemotherapy

- 5.4 Immunotherapy

- 5.5 Targeted therapy

- 5.6 Other therapies

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Androgen receptor inhibitors

- 6.3 GnRH receptor antagonists

- 6.4 PARP inhibitors

- 6.5 Immune checkpoint inhibitors

- 6.6 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Brick and mortar

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Astellas Pharma

- 10.2 AstraZeneca

- 10.3 Bayer

- 10.4 Dendreon Pharmaceuticals

- 10.5 Exelixis

- 10.6 Ferring

- 10.7 GlaxoSmithKline

- 10.8 Ipsen Pharma

- 10.9 Johnson & Johnson

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sumitomo Pharma America

- 10.14 Takeda Pharmaceutical

- 10.15 Tolmar

前列腺癌藥物市場:按藥物類型、通路和地區分類

前列腺癌藥物市場:按藥物類型、通路和地區分類 前列腺癌治療市場:依作用機制、治療線、劑型、通路和最終用戶分類-2026-2032年全球市場預測

前列腺癌治療市場:依作用機制、治療線、劑型、通路和最終用戶分類-2026-2032年全球市場預測 前列腺癌治療市場報告:按藥物類型、分銷管道和地區分類(2026-2034 年)Enzalutamide錠市場依治療階段、最終用戶、適應症、通路和劑量分類,全球預測,2026-2032年

前列腺癌治療市場報告:按藥物類型、分銷管道和地區分類(2026-2034 年)Enzalutamide錠市場依治療階段、最終用戶、適應症、通路和劑量分類,全球預測,2026-2032年 經尿道切除術(TURP) 市場規模、佔有率和成長分析:按產品類型、技術、應用、最終用戶和地區分類-2026-2033 年產業預測

經尿道切除術(TURP) 市場規模、佔有率和成長分析:按產品類型、技術、應用、最終用戶和地區分類-2026-2033 年產業預測 全球前列腺癌治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球微創前列腺癌手術市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球前列腺癌治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球微創前列腺癌手術市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 轉移性去勢抗性前列腺癌(mCRPC):新型療法、未滿足的需求和TPP洞察報告,2026年

轉移性去勢抗性前列腺癌(mCRPC):新型療法、未滿足的需求和TPP洞察報告,2026年 轉移性去勢敏感性前列腺癌 (mCSPC) 市場 - 全球和區域分析:按治療方法類型、按地區分類 - 分析和預測 (2025-2035)Enzalutamide藥品市場依品牌類型、適應症、劑型、劑量強度、最終用戶及通路分類-2026-2032年全球預測

轉移性去勢敏感性前列腺癌 (mCSPC) 市場 - 全球和區域分析:按治療方法類型、按地區分類 - 分析和預測 (2025-2035)Enzalutamide藥品市場依品牌類型、適應症、劑型、劑量強度、最終用戶及通路分類-2026-2032年全球預測