|

市場調查報告書

商品編碼

1664834

浸入式冷卻液市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Immersion Cooling Fluids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

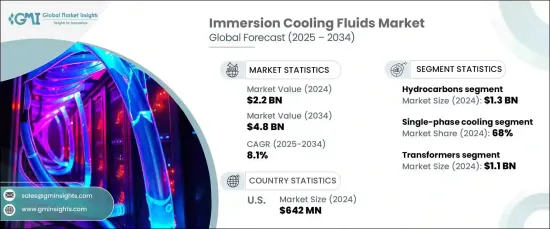

2024 年全球浸入式冷卻液市場價值 22 億美元,預計 2025 年至 2034 年期間的複合年成長率為 8.1%。該技術因其卓越的冷卻性能和能源效率而越來越受到關注。

高效能系統中對節能解決方案的需求不斷增加是推動市場成長的重要因素。由於產業面臨與熱管理相關的挑戰,浸入式冷卻提供了一種比傳統冷卻方法更緊湊、更有效的替代方案。流體技術的進步進一步提高了導熱性和冷卻效率,從而推動了它的採用。這些改進擴大了這些液體在多個行業中的可用性,為永續、高效的冷卻解決方案鋪平了道路。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 22億美元 |

| 預測值 | 48億美元 |

| 複合年成長率 | 8.1% |

市場根據流體類型分為碳氫化合物和氟碳化合物。碳氫化合物(包括礦物油和合成油)在 2024 年創造了 13 億美元的收入,並且由於其出色的傳熱能力和成本優勢仍然是首選。它們與多種系統設計的兼容性以及較低的環境影響促進了它們的廣泛使用。雖然氟碳化合物因其穩定性而受到關注,但碳氫化合物由於其整體性能優勢仍佔據主導地位。

從技術角度來看,市場分為單相冷卻和雙相冷卻。單相冷卻由於其簡單性、可靠性和較低的維護要求,在 2024 年佔據了 68% 的市場佔有率。它在高效能應用中的廣泛使用凸顯了其在解決關鍵冷卻需求方面的有效性。儘管兩相冷卻在管理升高的熱負載方面提供了增強的性能,但由於其已建立的基礎設施,單相系統仍然是首選。

根據應用,市場包括變壓器、資料中心和電池等部分。 2024 年,Transformers 以 11 億美元的營收引領市場。它們的冷卻要求強調了浸沒液在維持最佳功能和延長設備壽命方面的作用。隨著各行各業越來越重視能源效率,預計各類應用對這些流體的需求將會成長。

2024 年,美國領先區域市場,營收達 6.42 億美元。中國對永續性的重視,加上基礎設施的進步和不斷成長的工業需求,使得北美成為推動浸入式冷卻技術應用的關鍵參與者。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 資料中心對節能冷卻解決方案的需求不斷成長

- 電動車 (EV) 電池擴大採用浸入式冷卻技術

- 流體技術的進步提高了傳熱和冷卻效率

- 產業陷阱與挑戰

- 浸入式冷卻系統的初始成本和資本投入較高

- 資料中心和電動車電池以外行業的認知和採用有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場規模及預測:依流體類型,2021-2034 年

- 主要趨勢

- 碳氫化合物

- 礦物

- 合成的

- 氟碳化合物

第 6 章:市場規模與預測:依技術,2021-2034 年

- 主要趨勢

- 單相冷卻

- 兩相冷卻

第 7 章:市場規模與預測:按應用,2021-2034 年

- 主要趨勢

- 變壓器

- 資料中心

- 電動汽車電池

- 其他

第 8 章:市場規模與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 3M

- Cargill

- Chemie

- Chevron

- Dow

- Engineered Fluids

- Ergon

- ExxonMobil Chemical

- Shell

- Soltex

- Valvoline

The Global Immersion Cooling Fluids Market, valued at USD 2.2 billion in 2024, is anticipated to grow at a CAGR of 8.1% between 2025 and 2034. Immersion cooling fluids, designed to submerge electronic components, excel in efficiently dissipating heat from devices such as servers, transformers, and batteries. This technology is gaining traction for its superior cooling performance and energy efficiency.

Increasing demand for energy-efficient solutions in high-performance systems is a significant factor driving market growth. As industries face challenges related to heat management, immersion cooling offers a more compact and effective alternative to conventional cooling methods. Its adoption is further propelled by advancements in fluid technology that enhance thermal conductivity and cooling efficiency. These improvements broaden the usability of these fluids across multiple industries, paving the way for sustainable and efficient cooling solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 8.1% |

The market is categorized by fluid type into hydrocarbons and fluorocarbons. Hydrocarbons, including mineral oils and synthetic variants, generated USD 1.3 billion in 2024 and remain the preferred choice due to their superior heat transfer capabilities and cost advantages. Their compatibility with diverse system designs and lower environmental impact bolster their widespread use. While fluorocarbons are gaining attention for their stability, hydrocarbons maintain dominance due to their overall performance benefits.

From a technological standpoint, the market is divided into single-phase and two-phase cooling. Single-phase cooling captured 68% of the market share in 2024, thanks to its simplicity, reliability, and lower maintenance requirements. Its widespread use in high-performance applications highlights its effectiveness in addressing critical cooling needs. Although two-phase cooling offers enhanced performance for managing elevated heat loads, single-phase systems remain the favored choice due to their established infrastructure.

By application, the market includes segments such as transformers, data centers, and batteries. Transformers led the market in 2024 with USD 1.1 billion in revenue. Their cooling requirements emphasize the role of immersion fluids in maintaining optimal functionality and prolonging equipment life. As industries increasingly prioritize energy efficiency, demand for these fluids is expected to grow across various applications.

In 2024, the US led the regional market, earning USD 642 million in revenue. The country's emphasis on sustainability, coupled with advancements in infrastructure and growing industrial demands, positions North America as a key player in driving the adoption of immersion cooling technology.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for energy-efficient cooling solutions in data centers

- 3.6.1.2 Increasing adoption of immersion cooling technology in electric vehicle (EV) batteries

- 3.6.1.3 Advancements in fluid technology enhancing heat transfer and cooling efficiency

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial cost and capital investment for immersion cooling systems

- 3.6.2.2 Limited awareness and adoption in industries outside data centers and EV batteries

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Fluid Type, 2021-2034 (USD Billion, Metric Tons)

- 5.1 Key trends

- 5.2 Hydrocarbons

- 5.2.1 Mineral

- 5.2.2 Synthetic

- 5.3 Fluorocarbons

Chapter 6 Market Size and Forecast, By Technology, 2021-2034 (USD Billion, Metric Tons)

- 6.1 Key trends

- 6.2 Single-phase cooling

- 6.3 Two-phase cooling

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion, Metric Tons)

- 7.1 Key trends

- 7.2 Transformers

- 7.3 Data centre

- 7.4 EV batteries

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion, Metric Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Cargill

- 9.3 Chemie

- 9.4 Chevron

- 9.5 Dow

- 9.6 Engineered Fluids

- 9.7 Ergon

- 9.8 ExxonMobil Chemical

- 9.9 Shell

- 9.10 Soltex

- 9.11 Valvoline

2025年全球浸入式冷卻液市場報告

2025年全球浸入式冷卻液市場報告 全球浸入式冷卻市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年浸入式冷卻液市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按最終用戶、按地區和競爭細分,2020-2030 年

全球浸入式冷卻市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年浸入式冷卻液市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按最終用戶、按地區和競爭細分,2020-2030 年 浸入式冷卻市場規模、佔有率、趨勢分析報告:按產品、應用、冷卻劑、地區、細分市場預測,2025-2030 年

浸入式冷卻市場規模、佔有率、趨勢分析報告:按產品、應用、冷卻劑、地區、細分市場預測,2025-2030 年 浸入式冷卻市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032)

浸入式冷卻市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032) 全球浸入式冷卻市場:按產品、冷卻劑、應用、地區 - 趨勢分析、競爭格局、預測(2019-2030)

全球浸入式冷卻市場:按產品、冷卻劑、應用、地區 - 趨勢分析、競爭格局、預測(2019-2030) 液浸冷卻市場規模、佔有率、成長分析、按類型、按冷卻液、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年全球浸入式冷卻市場 2024-2031

液浸冷卻市場規模、佔有率、成長分析、按類型、按冷卻液、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年全球浸入式冷卻市場 2024-2031 液浸式冷卻劑市場:按類型、技術和應用分類 - 2025-2030 年全球預測液浸冷卻市場:按冷卻劑、類型、系統和應用分類 - 2025-2030 年全球預測

液浸式冷卻劑市場:按類型、技術和應用分類 - 2025-2030 年全球預測液浸冷卻市場:按冷卻劑、類型、系統和應用分類 - 2025-2030 年全球預測