|

市場調查報告書

商品編碼

1664843

遠距工作工具/軟體市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Remote Working Tools/Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

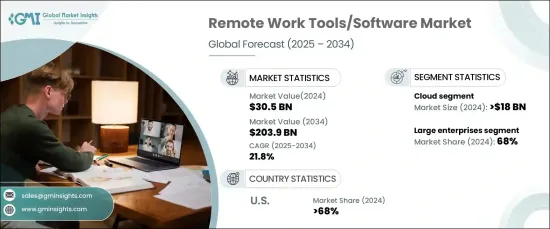

2024 年全球遠距工作工具/軟體市場估值達到 305 億美元,預計 2025 年至 2034 年期間複合年成長率為 21.8%。即時語言翻譯、自動排程、預測分析和智慧任務優先等創新功能可提高生產力,同時減少手動工作量。各行業的企業擴大採用人工智慧驅動的解決方案來簡化工作流程並適應不斷變化的營運需求,特別是在混合和遠端工作環境中。

人們也越來越關注旨在促進工作與生活平衡的工具。整合壓力管理和心理健康支援等健康和保健功能的軟體越來越受歡迎。企業逐漸意識到員工健康對於提高生產力的重要性,這有望推動這些專業解決方案的需求。這為軟體供應商滿足這一不斷擴大的細分市場需求創造了重大機會。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 305億美元 |

| 預測值 | 2039億美元 |

| 複合年成長率 | 21.8% |

根據部署模式,市場分為基於雲端的解決方案和內部部署的解決方案。 2024 年,基於雲端的工具價值超過 190 億美元,憑藉其靈活性、成本效益和易於訪問性佔據市場主導地位。雲端平台支援跨不同地點的無縫業務營運,無需大量硬體。自動更新、資料備份和協作框架等功能對於支援遠端團隊至關重要。隨著雲端安全的進步和混合工作模式的廣泛採用,對這些工具的需求持續上升。越來越多的組織選擇雲端解決方案來提高效率、降低成本並維持營運連續性。

根據組織規模,市場分為中小型企業 (SME) 和大型企業。大型組織需要可擴展且強大的工具來管理大量勞動力,因此在 2024 年佔據了 68% 的市場佔有率。這些企業優先考慮安全性,採用具有先進加密和合規功能的軟體。與現有系統的整合以及高級解決方案的更高預算進一步推動了採用,使企業能夠最佳化生產力並簡化全球營運。

由於早期採用混合工作模式、強大的數位基礎設施和精通技術的勞動力,美國市場將在 2024 年佔據超過 68% 的收入佔有率。支持性政策和國家以創新為中心的文化繼續加速市場的成長。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 軟體/工具供應商

- 技術提供者

- 雲端服務供應商

- 系統整合商

- 最終用途

- 利潤率分析

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 混合工作模式的採用日益增多

- 安全協作工具的需求不斷增加

- 全球廣泛採用基於雲端的軟體

- 對自動化遠距工作流程的偏好日益成長

- 產業陷阱與挑戰

- 基於雲端的解決方案中的安全漏洞

- 發展中地區數位基礎設施不足

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 軟體/工具

- 協作工具

- 通訊工具

- 生產力工具

- 人力資源和薪資工具

- 安全工具

- 服務

- 專業的

- 託管

第6章:市場估計與預測:依部署模式,2021 - 2034 年

- 主要趨勢

- 雲

- 本地

第 7 章:市場估計與預測:按組織規模,2021 - 2034 年

- 主要趨勢

- 中小企業

- 大型企業

第 8 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 金融保險業協會

- 衛生保健

- 資訊科技和電信

- 政府

- 製造業

- 教育

- 其他

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東南亞

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東及非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- Adobe

- Asana

- Atlassian

- Basecamp

- Cisco Webex

- ClickUp

- Dropbox

- GitHub

- HubSpot

- Microsoft

- Miro

- Monday.com

- Notion

- RingCentral

- Salesforce

- Smartsheet

- Trello

- Zoho

- Zoom Video Communications

The Global Remote Working Tools/Software Market reached a valuation of USD 30.5 billion in 2024 and is forecasted to grow at a CAGR of 21.8% from 2025 to 2034. AI-powered tools are transforming how teams collaborate and communicate in remote settings. Innovative features such as real-time language translation, automated scheduling, predictive analytics, and intelligent task prioritization boost productivity while reducing manual workload. Businesses across various sectors are increasingly adopting AI-driven solutions to streamline workflows and adapt to changing operational demands, particularly in hybrid and remote work environments.

There is also a growing focus on tools designed to promote work-life balance. Software with integrated health and wellness features, such as stress management and mental well-being support, is gaining popularity. Organizations are recognizing the importance of employee health in driving productivity, which is expected to fuel demand for these specialized solutions. This creates significant opportunities for software providers to cater to this expanding market segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.5 Billion |

| Forecast Value | $203.9 Billion |

| CAGR | 21.8% |

The market is categorized by deployment mode into cloud-based and on-premise solutions. In 2024, cloud-based tools accounted for over USD 19 billion, dominating the market due to their flexibility, cost-effectiveness, and ease of access. Cloud platforms enable seamless business operations across various locations, eliminating the need for extensive hardware. Features like automatic updates, data backup, and collaborative frameworks are essential for supporting remote teams. With advancements in cloud security and the widespread adoption of hybrid work models, demand for these tools continues to rise. Organizations increasingly opt for cloud solutions to enhance efficiency, cut costs, and maintain operational continuity.

By organization size, the market is divided into small and medium-sized enterprises (SME) and large enterprises. Large organizations held 68% of the market share in 2024 due to their need for scalable and robust tools to manage extensive workforces. These enterprises prioritize security, adopting software with advanced encryption and compliance capabilities. Integration with existing systems and higher budgets for premium solutions further drive adoption, enabling businesses to optimize productivity and streamline global operations.

The US market led with over 68% of the revenue share in 2024, driven by early adoption of hybrid work models, a strong digital infrastructure, and a tech-savvy workforce. Supportive policies and the nation's innovation-focused culture continue to accelerate the market's growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Software/tool provider

- 3.2.2 Technology provider

- 3.2.3 Cloud service provider

- 3.2.4 System Integrators

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising adoption of hybrid work models

- 3.7.1.2 Increasing demand for secure collaboration tools

- 3.7.1.3 Widespread adoption of cloud-based software globally

- 3.7.1.4 Growing preference for automated remote workflows

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Security vulnerabilities in cloud-based solutions

- 3.7.2.2 Inadequate digital infrastructure in developing regions

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Software/Tools

- 5.2.1 Collaboration tools

- 5.2.2 Communication tools

- 5.2.3 Productivity tools

- 5.2.4 HR and payroll tools

- 5.2.5 Security tools

- 5.3 Services

- 5.3.1 Professional

- 5.3.2 Managed

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premise

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By End-Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Healthcare

- 8.4 IT & Telecom

- 8.5 Government

- 8.6 Manufacturing

- 8.7 Education

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Adobe

- 10.2 Asana

- 10.3 Atlassian

- 10.4 Basecamp

- 10.5 Cisco Webex

- 10.6 ClickUp

- 10.7 Dropbox

- 10.8 GitHub

- 10.9 Google

- 10.10 HubSpot

- 10.11 Microsoft

- 10.12 Miro

- 10.13 Monday.com

- 10.14 Notion

- 10.15 RingCentral

- 10.16 Salesforce

- 10.17 Smartsheet

- 10.18 Trello

- 10.19 Zoho

- 10.20 Zoom Video Communications

2025年全球遠距工作場所服務市場報告

2025年全球遠距工作場所服務市場報告 遠距工作場所服務市場規模、佔有率和成長分析(按組件、組織規模、部署類型、垂直和地區)- 2025-2032 年產業預測

遠距工作場所服務市場規模、佔有率和成長分析(按組件、組織規模、部署類型、垂直和地區)- 2025-2032 年產業預測 遠距工作場所服務市場:按組成部分、組織規模、部署類型、產業 - 2025-2030 年全球預測遠距工作安全市場:按提供的服務、按安全類型、按遠端工作模式、按部署模組、按最終用戶 - 2025-2030 年全球預測

遠距工作場所服務市場:按組成部分、組織規模、部署類型、產業 - 2025-2030 年全球預測遠距工作安全市場:按提供的服務、按安全類型、按遠端工作模式、按部署模組、按最終用戶 - 2025-2030 年全球預測 全球遠距工作安全市場規模、佔有率、趨勢分析報告(按產品、工作模式、安全類型、最終用戶、地區、前景和預測,2024-2031)

全球遠距工作安全市場規模、佔有率、趨勢分析報告(按產品、工作模式、安全類型、最終用戶、地區、前景和預測,2024-2031) 遠距工作安全市場:按服務提供、安全類型、工作模式和最終用戶分類:2024-2032 年全球機會分析和產業預測遠距工作軟體市場:按組件、按部署模式、按類型、按公司規模、按最終用戶:2024-2032 年全球機會分析和行業預測

遠距工作安全市場:按服務提供、安全類型、工作模式和最終用戶分類:2024-2032 年全球機會分析和產業預測遠距工作軟體市場:按組件、按部署模式、按類型、按公司規模、按最終用戶:2024-2032 年全球機會分析和行業預測 遠距工作安全市場、佔有率、規模、趨勢、行業分析報告、依提供的服務、依安全類型、依遠端工作模式、依行業、依地區、依細分市場預測,2024-2032 年

遠距工作安全市場、佔有率、規模、趨勢、行業分析報告、依提供的服務、依安全類型、依遠端工作模式、依行業、依地區、依細分市場預測,2024-2032 年 全球遠距工作安全市場(~2028 年):提供者: ,安全型 ,遠距工作模式 ,產業 ,按地區

全球遠距工作安全市場(~2028 年):提供者: ,安全型 ,遠距工作模式 ,產業 ,按地區