|

市場調查報告書

商品編碼

1664901

用於引擎冷卻的汽車電動水泵市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Automotive Electric Water Pump for Engine Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

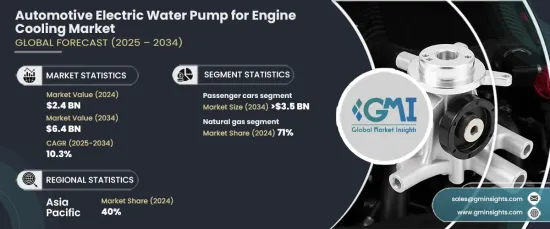

2024 年全球汽車引擎冷卻用電動水泵市場價值為 24 億美元,預計 2025 年至 2034 年期間將以 10.3% 的強勁複合年成長率成長。世界各國政府和消費者越來越重視能源效率,以減少燃料消耗和減輕環境影響,推動了市場大幅擴張。

根據車輛類型,市場分為商用車和乘用車。 2024 年,乘用車市場佔據市場主導地位,佔總佔有率的 65%,預計到 2034 年將達到 35 億美元。這些泵浦對於維持最佳引擎溫度、提高燃油效率、減少引擎壓力和降低排放至關重要(這些都是滿足嚴格的環境標準的關鍵因素)。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 24億美元 |

| 預測值 | 64億美元 |

| 複合年成長率 | 10.3% |

根據推進類型,市場分為內燃機汽車和電動車 (EV)。 2024 年,ICE 市佔率達 71%。隨著消費者對更安靜、更有效率、功能更完善的車輛的需求不斷成長,電動水泵的採用也日益增加。這些幫浦不僅可以提供卓越的引擎冷卻,還可以提高車廂加熱效率,提供更舒適、更無縫的駕駛體驗。

亞太地區成為最大的區域市場,到 2024 年將佔據 40% 的佔有率。該地區的汽車製造商正在將電動水泵整合到 ICE 和 EV 車型中,以滿足汽車性能和效率的全球標準。

政府舉措,包括補貼和基礎建設,正在加速亞太地區電動車的普及。這種激增推動了對電動水泵的需求,而電動水泵對於電動車的有效熱管理至關重要。作為全球最大的電動車生產國,中國在政府激勵措施和快速擴大的電動車消費群體的支持下,在這一成長中發揮關鍵作用。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 原物料供應商

- 零件供應商

- 製造商

- 技術提供者

- 最終用戶

- 供應商格局

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞及舉措

- 監管格局

- 定價分析

- 衝擊力

- 成長動力

- 電動和混合動力車的普及率不斷上升

- 監管重點日益轉向減少車輛排放和提高燃油效率

- 新興經濟體汽車生產的擴張

- 電動水泵設計的技術創新

- 產業陷阱與挑戰

- 依賴電池效能

- 將電動水泵整合到傳統汽車系統中的初始成本高且複雜

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按電壓,2021 - 2034 年

- 主要趨勢

- 12伏

- 24伏

第 6 章:市場估計與預測:按推進方式,2021 - 2034 年

- 主要趨勢

- 冰

- 汽油

- 柴油引擎

- 電的

- 混合動力電動車 (HEV)

- 純電動車 (BEV)

- 燃料電池電動車

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- 掀背車

- SUV

- 其他

- 商用車

- 輕型商用車 (LCV)

- 重型商用車 (HCV)

第 8 章:市場估計與預測:按銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Aisin Seiki

- BLDC Pump

- Bosch

- Carter Fuel Systems

- Continental

- Cummins

- Davies Craig

- Denso

- Gates

- GMB Corporation

- Hanon

- Hitachi Automotive

- Mahle

- Mitsubishi Electric

- Rexroth

- Rheinmetall

- Schaeffler Technologies

- Shandong Boshan

- Valeo

- VOVYO Technology

The Global Automotive Electric Water Pump For Engine Cooling Market was valued at USD 2.4 billion in 2024 and is projected to grow at a robust CAGR of 10.3% from 2025 to 2034. This growth is primarily fueled by the surging demand for fuel-efficient vehicles. Governments and consumers worldwide are increasingly emphasizing energy efficiency to reduce fuel consumption and mitigate environmental impact, driving significant market expansion.

The market is categorized by vehicle type into commercial vehicles and passenger cars. In 2024, the passenger car segment dominated the market, accounting for 65% of the total share, and is projected to reach USD 3.5 billion by 2034. Stricter global emission regulations are compelling automakers to adopt advanced cooling solutions, such as electric water pumps, in internal combustion engine (ICE) vehicles. These pumps are critical for maintaining optimal engine temperatures, enhancing fuel efficiency, reducing engine stress, and lowering emissions-key factors in meeting rigorous environmental standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 10.3% |

Based on propulsion type, the market is divided into ICE and electric vehicles (EVs). In 2024, the ICE segment held a commanding 71% market share. As consumers increasingly demand quieter, more efficient vehicles with improved features, the adoption of electric water pumps has gained momentum. These pumps not only deliver superior engine cooling but also enhance cabin heating efficiency, offering a more comfortable and seamless driving experience.

Asia Pacific emerged as the largest regional market, holding a 40% share in 2024. Countries like China and India, recognized as major automotive manufacturing hubs, are spearheading the demand for advanced engine cooling technologies. Automakers in the region are integrating electric water pumps into both ICE and EV models to meet global standards for vehicle performance and efficiency.

Government initiatives, including subsidies and infrastructure development, are accelerating EV adoption in Asia Pacific. This surge is driving demand for electric water pumps, which are essential for effective thermal management in EVs. As the world's largest EV producer, China is playing a pivotal role in this growth, supported by government incentives and a rapidly expanding consumer base for electric vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of electric and hybrid vehicles

- 3.9.1.2 Increasing regulatory focus on reducing vehicle emissions and improving fuel efficiency

- 3.9.1.3 Expansion of automotive production in emerging economies

- 3.9.1.4 Technological innovations in electric water pump design

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Dependence on battery performance

- 3.9.2.2 High initial costs and complexity in integrating electric water pumps into traditional automotive systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Voltage, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 12V

- 5.3 24V

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.2.1 Gasoline

- 6.2.2 Diesel

- 6.3 Electric

- 6.3.1 Hybrid electric vehicles (HEVs)

- 6.3.2 Battery electric vehicles (BEVs)

- 6.3.3 Fuel cell electric vehicles

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUVs

- 7.2.4 Others

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin Seiki

- 10.2 BLDC Pump

- 10.3 Bosch

- 10.4 Carter Fuel Systems

- 10.5 Continental

- 10.6 Cummins

- 10.7 Davies Craig

- 10.8 Denso

- 10.9 Gates

- 10.10 GMB Corporation

- 10.11 Hanon

- 10.12 Hitachi Automotive

- 10.13 Mahle

- 10.14 Mitsubishi Electric

- 10.15 Rexroth

- 10.16 Rheinmetall

- 10.17 Schaeffler Technologies

- 10.18 Shandong Boshan

- 10.19 Valeo

- 10.20 VOVYO Technology

汽車冷卻液:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

汽車冷卻液:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 汽車冷卻液市場,按產品類型、按技術、按車輛類型、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

汽車冷卻液市場,按產品類型、按技術、按車輛類型、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 全球汽車冷卻液和潤滑油市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球汽車冷卻液和潤滑油市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 汽車冷卻液市場規模、佔有率和成長分析(按產品、類型、車輛類型、技術、分銷管道、最終用戶和地區)- 產業預測 2025-2032

汽車冷卻液市場規模、佔有率和成長分析(按產品、類型、車輛類型、技術、分銷管道、最終用戶和地區)- 產業預測 2025-2032 汽車冷卻液儲罐市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(加壓、非加壓)、應用(乘用車、商用車)、地區和競爭細分,2020-2030F電動冷卻液幫浦市場:各電壓類型,各車輛類型,各用途,各銷售管道,各地區,機會,預測,2018年~2032年

汽車冷卻液儲罐市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(加壓、非加壓)、應用(乘用車、商用車)、地區和競爭細分,2020-2030F電動冷卻液幫浦市場:各電壓類型,各車輛類型,各用途,各銷售管道,各地區,機會,預測,2018年~2032年 電動冷卻液幫浦市場:冷卻液幫浦類型、冷卻液類型、電源、功率範圍、應用 - 2025-2030 年全球預測

電動冷卻液幫浦市場:冷卻液幫浦類型、冷卻液類型、電源、功率範圍、應用 - 2025-2030 年全球預測 2024-2028年全球汽車冷卻液市場汽車冷卻液市場:按化學類型、技術、車輛和最終用戶分類 - 2025-2030 年全球預測

2024-2028年全球汽車冷卻液市場汽車冷卻液市場:按化學類型、技術、車輛和最終用戶分類 - 2025-2030 年全球預測 乘用車電動冷卻液幫浦全球市場,2024-2028

乘用車電動冷卻液幫浦全球市場,2024-2028