|

市場調查報告書

商品編碼

1665034

汽車前後實體數位化防護罩市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Front and Rear Phygital Shield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

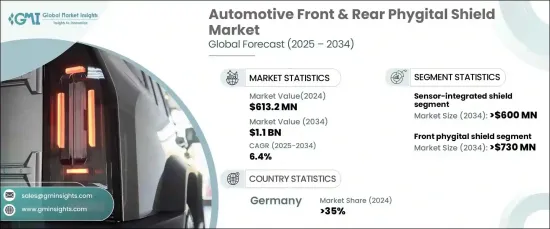

2024 年全球汽車前後實體數位化防護罩市場價值為 6.132 億美元,預計 2025 年至 2034 年期間將以 6.4% 的強勁複合年成長率成長。這些防護罩經過精心設計,融入了這些先進技術,同時保持了車輛的美觀度,滿足了功能和風格要求。

市場按產品類型細分為前實體數位防護罩和後實體數位防護罩。 2024 年,前部實體數位化防護板將佔據最大佔有率,佔據 65% 的市場。隨著電動車和豪華車擴大採用 LED 和顯示前擋風玻璃,預計到 2034 年該細分市場的規模將達到 7.3 億美元。這些先進的防護罩融合了自適應照明系統和數位顯示器等功能,可提供動態品牌標識、訊號和增強的通訊功能,這是現代汽車設計的關鍵差異化因素。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 6.132億美元 |

| 預測值 | 11億美元 |

| 複合年成長率 | 6.4% |

在技術方面,市場分為感測器整合防護罩、LED/顯示器防護罩和空氣動力學防護罩。預計到 2034 年,整合感測器的屏蔽罩將產生 6 億美元的收入,這展示了智慧屏蔽罩技術的快速進步。這些防護罩現在具有預處理功能,可以在感測器資料到達車輛的中央系統之前對其進行處理。透過實現分散式處理,它們顯著減少了延遲並增強了自動駕駛功能的即時決策。此外,支援無線(OTA)更新的能力與對邊緣運算的日益重視相一致,使汽車製造商能夠遠端改進感測器演算法並確保持續的性能提升。

2024 年,德國佔據了相當大的市場佔有率,佔全球需求的 35%。作為汽車創新的領先中心,該國擁有眾多高階汽車製造商,正在推動先進實體數位化防護罩的採用。這些防護罩在容納高級駕駛輔助系統 (ADAS) 必不可少的感測器和攝影機方面發揮著不可或缺的作用,ADAS 為車道維持輔助、防撞和行人偵測等功能提供動力。汽車產業對車輛安全性和自主性的日益關注持續推動了對這些技術先進的防護罩的需求。

報告內容

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 零件製造商

- 一級供應商

- 汽車OEM

- 技術整合商

- 最終用戶

- 利潤率分析

- 技術差異化

- 感測器整合

- LED 照明和顯示系統

- 空氣動力學設計增強

- 其他

- 重要新聞及舉措

- 專利分析

- 監管格局

- 衝擊力

- 成長動力

- 電動車普及率上升

- 自動駕駛和連網汽車的成長

- 消費者對車輛個人化的需求日益成長

- 車身空氣動力學越來越受關注

- 產業陷阱與挑戰

- 開發成本高

- 複雜的製造程序

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 前部物理防護罩

- 後部物理防護罩

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車 (LCV)

- 重型商用車 (HCV)

第 7 章:市場估計與預測:按技術,2021 - 2032 年

- 主要趨勢

- 感測器整合防護罩

- LED/顯示器

- 空氣動力學

第 8 章:市場估計與預測:按材料,2021 - 2032 年

- 主要趨勢

- 塑膠/聚合物基

- 金屬基

- 合成的

第 9 章:市場估計與預測:按銷售管道,2021 - 2032 年

- 主要趨勢

- OEM

- 售後市場

第 10 章:市場估計與預測:按地區,2021 - 2032 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- Covestro

- Forvia Hella

- Harman

- Hyundai Mobis

- Infineon

- Intops

- Kia

- Magna

- Marelli

- Motherson

- Niebling

- Plastic Omnium

- Prolim

- Texas Instruments

- Valeo

The Global Automotive Front And Rear Phygital Shield Market was valued at USD 613.2 million in 2024 and is projected to grow at a robust CAGR of 6.4% from 2025 to 2034. Phygital shields have emerged as a critical component in the integration of cutting-edge sensor systems such as LiDAR, radar, and cameras, which are pivotal for the navigation, communication, and safety of autonomous and connected vehicles. These shields are meticulously designed to incorporate these advanced technologies while maintaining the vehicle's aesthetic appeal, meeting both functional and stylistic demands.

The market is segmented by product type into front phygital shields and rear phygital shields. In 2024, front phygital shields held the lion's share, accounting for 65% of the market. This segment is anticipated to reach USD 730 million by 2034, driven by the growing adoption of LED and display-enabled front shields in electric and luxury vehicles. These advanced shields incorporate features such as adaptive lighting systems and digital displays, which provide dynamic branding, signaling, and enhanced communication capabilities-key differentiators in modern automotive design.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $613.2 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.4% |

On the technology front, the market is categorized into sensor-integrated shields, LED/display shields, and aerodynamic shields. Sensor-integrated shields are forecasted to generate USD 600 million by 2034, showcasing rapid advancements in smart shield technology. These shields now feature preprocessing capabilities that handle sensor data before it reaches the vehicle's central systems. By enabling distributed processing, they significantly reduce latency and enhance real-time decision-making for autonomous driving features. Furthermore, the ability to support over-the-air (OTA) updates aligns with the growing emphasis on edge computing, enabling automakers to refine sensor algorithms remotely and ensure continuous performance enhancements.

Germany represented a significant share of the market in 2024, accounting for 35% of the global demand. As a leading hub for automotive innovation, the country is home to numerous premium automotive manufacturers driving the adoption of advanced phygital shields. These shields play an integral role in housing sensors and cameras essential for Advanced Driver Assistance Systems (ADAS), which power features like lane-keeping assistance, collision avoidance, and pedestrian detection. The rising focus on vehicle safety and autonomy in the automotive sector continues to fuel the demand for these technologically sophisticated shields.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component manufacturers

- 3.2.2 Tier-1 suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Technology integrators

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology differentiators

- 3.4.1 Sensor integration

- 3.4.2 LED lighting and display systems

- 3.4.3 Aerodynamic design enhancements

- 3.4.4 Others

- 3.5 Key news & initiatives

- 3.6 Patent analysis

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rise in electric vehicle adoption

- 3.8.1.2 Growth of autonomous and connected vehicles

- 3.8.1.3 Growing consumer demand for vehicle personalization

- 3.8.1.4 Growing focus on aerodynamics of vehicle body

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development costs

- 3.8.2.2 Complex manufacturing process

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front phygital shield

- 5.3 Rear phygital shield

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 Sensor-integrated shield

- 7.3 LED/display

- 7.4 Aerodynamic

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2032 ($Bn, Units)

- 8.1 Key trends

- 8.2 Plastic/polymer-based

- 8.3 Metal-based

- 8.4 Composite

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2032 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Covestro

- 11.2 Forvia Hella

- 11.3 Harman

- 11.4 Hyundai Mobis

- 11.5 Infineon

- 11.6 Intops

- 11.7 Kia

- 11.8 Magna

- 11.9 Marelli

- 11.10 Motherson

- 11.11 Niebling

- 11.12 Plastic Omnium

- 11.13 Prolim

- 11.14 Texas Instruments

- 11.15 Valeo

全球汽車安全氣囊電控系統(ECU) 市場 2025-2029

全球汽車安全氣囊電控系統(ECU) 市場 2025-2029 全球雪崩安全氣囊市場

全球雪崩安全氣囊市場 汽車安全氣囊織物市場規模、佔有率和成長分析(按安全氣囊類型、車輛類型、塗層類型、紗線類型和地區)- 2025-2032 年產業預測

汽車安全氣囊織物市場規模、佔有率和成長分析(按安全氣囊類型、車輛類型、塗層類型、紗線類型和地區)- 2025-2032 年產業預測 安全氣囊系統啟動器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

安全氣囊系統啟動器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 汽車側氣簾市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車側氣簾市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 汽車簾式安全氣囊市場規模、佔有率、成長分析(按車型、按材料、按應用、按最終用戶、按地區)-按行業預測,2024-2031

汽車簾式安全氣囊市場規模、佔有率、成長分析(按車型、按材料、按應用、按最終用戶、按地區)-按行業預測,2024-2031 汽車安全氣囊控制器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車安全氣囊控制器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 汽車簾式安全氣囊市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、車輛類型、需求類別、地區和競爭細分,2019-2029F

汽車簾式安全氣囊市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、車輛類型、需求類別、地區和競爭細分,2019-2029F 汽車安全氣囊市場規模、佔有率、成長分析(按類型、車輛類型、零件、地區)- 產業預測,2024-2031 年

汽車安全氣囊市場規模、佔有率、成長分析(按類型、車輛類型、零件、地區)- 產業預測,2024-2031 年 全球安全氣囊市場 - 2024-2031

全球安全氣囊市場 - 2024-2031