|

市場調查報告書

商品編碼

1665077

醫療保健電子資料交換市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Healthcare Electronic Data Interchange Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

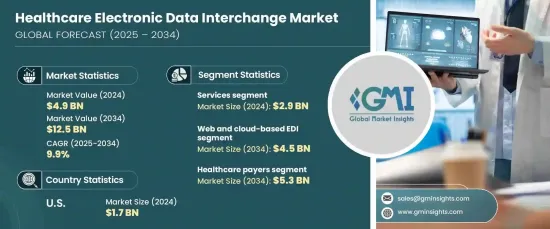

全球醫療保健電子資料交換市場在 2024 年的價值為 49 億美元,將經歷顯著成長,預計 2025 年至 2034 年期間的複合年成長率為 9.9%。

隨著醫療保健產業擁抱數位轉型,EDI 平台成為付款人、提供者和利害關係人之間安全、標準化和高效資料交換不可或缺的工具。這些平台消除了手動流程的低效率,確保遵守不斷變化的法規並保護敏感的患者資訊。此外,雲端運算和人工智慧分析的進步引入了先進、經濟高效的解決方案,擴大了 EDI 系統對各種規模組織的吸引力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 49億美元 |

| 預測值 | 125億美元 |

| 複合年成長率 | 9.9% |

政府法規和行業標準在加速醫療保健 EDI 系統的採用方面發揮關鍵作用。監管框架強調了安全資料交換的必要性,促使醫療保健組織實現工作流程的現代化。自動化 EDI 解決方案可確保無縫遵守隱私和安全標準,同時促進整個醫療保健生態系統的有效溝通。在醫療保健提供者努力應對最佳化性能和降低成本日益增大的壓力之際,數位化的推動尤為重要,從而進一步推動了市場的擴張。

從組件方面來看,醫療保健 EDI 市場分為服務和解決方案,其中服務在創造收入方面佔據主導地位。 2024 年服務業規模將達到 29 億美元,反映了該行業對系統整合、客製化、培訓和技術支援的依賴。隨著組織從傳統系統過渡到現代化 EDI 平台,這些服務可確保順利、高效的整合流程。對專業服務的需求不斷成長,凸顯了醫療保健產業對實現互通性和遵守嚴格的合規性要求的重視。預計這一趨勢將獲得發展動力,與醫療保健提供者對卓越營運的優先事項保持一致。

市場還根據部署類型進行細分,包括 EDI 增值網路 (VAN)、直接(點對點)EDI、基於 Web 和雲端的 EDI 以及行動 EDI。其中,基於網路和雲端的 EDI 解決方案在 2024 年佔據主導地位,預計到 2034 年該領域將產生 45 億美元的收入。這些系統對於尋求使用先進工具但又無需承擔維護內部基礎設施負擔的中小型供應商尤其有吸引力。基於雲端的 EDI 的靈活性、可靠性和可負擔性使其成為市場成長軌蹟的基石。

2024 年,北美佔據了 17 億美元的醫療保健 EDI 市場,這得益於嚴格的監管要求(要求標準化交易)和美國強勁的醫療保健支出。隨著產業優先考慮數據驅動的創新,對數位基礎設施和人工智慧驅動的分析的投資繼續推動先進 EDI 解決方案的採用,從而重塑醫療保健資料交換的全球格局。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 監管支持和合規要求

- 互通性需求不斷成長

- 技術進步

- 降低成本、提高效率

- 產業陷阱與挑戰

- 實施成本高

- 成長動力

- 成長潛力分析

- 監管格局

- 美國

- 歐洲

- 技術格局

- 未來市場趨勢

- 創新格局

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按組件,2021 年至 2034 年

- 主要趨勢

- 服務

- 解決方案

第 6 章:市場估計與預測:按部署類型,2021 年至 2034 年

- 主要趨勢

- 基於 Web 和雲端的 EDI

- EDI加值網路(VAN)

- 直接(點對點)EDI

- 移動EDI

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫療支付者

- 醫療保健提供者

- 製藥和醫療器材產業

- 其他最終用戶

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Boomi

- Cleo

- DataTrans Solutions

- Effective Data

- Epicor Software Corporation

- GE Healthcare

- MCKESSON CORPORATION

- NXGN Management

- OpenText

- Optum

- Oracle

- OSP

- SPS Commerce

- SSI Group

- TrueCommerce

The Global Healthcare Electronic Data Interchange Market, valued at USD 4.9 billion in 2024, is set to experience remarkable growth with a projected CAGR of 9.9% between 2025 and 2034. This expansion is driven by the increasing adoption of automated EDI solutions, propelled by stringent regulatory mandates, growing demand for seamless interoperability, and the rising need to streamline administrative operations in healthcare systems.

As the healthcare industry embraces digital transformation, EDI platforms emerge as indispensable tools for secure, standardized, and efficient data exchange between payers, providers, and stakeholders. These platforms eliminate the inefficiencies of manual processes, ensuring compliance with evolving regulations and safeguarding sensitive patient information. Furthermore, advancements in cloud computing and AI-powered analytics have introduced sophisticated, cost-effective solutions, broadening the appeal of EDI systems to organizations of all sizes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 9.9% |

Government regulations and industry standards play a pivotal role in accelerating the adoption of healthcare EDI systems. Regulatory frameworks emphasize the necessity for secure data exchange, prompting healthcare organizations to modernize their workflows. Automated EDI solutions ensure seamless compliance with privacy and security standards while fostering efficient communication across the healthcare ecosystem. This push toward digitization is particularly significant as healthcare providers grapple with mounting pressures to optimize performance and reduce costs, further driving the market's expansion.

In terms of components, the healthcare EDI market is segmented into services and solutions, with services leading the charge in revenue generation. Services reached USD 2.9 billion in 2024, reflecting the industry's reliance on system integration, customization, training, and technical support. As organizations transition from legacy systems to modern EDI platforms, these services ensure a smooth and efficient integration process. The rising demand for professional services underscores the healthcare sector's focus on achieving interoperability and adhering to stringent compliance requirements. This trend is expected to gain momentum, aligning with healthcare providers' priorities for operational excellence.

The market also segments based on deployment type, including EDI value-added networks (VANs), direct (point-to-point) EDI, web and cloud-based EDI, and mobile EDI. Among these, web and cloud-based EDI solutions dominated in 2024, and this segment is forecasted to generate USD 4.5 billion by 2034. Cloud-based solutions offer unmatched scalability and cost-efficiency, allowing healthcare organizations to expand operations without heavy hardware investments. These systems are particularly attractive to small and medium-sized providers seeking access to advanced tools without the burden of maintaining on-premises infrastructure. The flexibility, reliability, and affordability of cloud-based EDI make it a cornerstone of the market's growth trajectory.

North America accounted for USD 1.7 billion of the healthcare EDI market in 2024, fueled by strict regulatory requirements mandating standardized transactions and robust healthcare spending in the United States. As the industry prioritizes data-driven innovations, investments in digital infrastructure and AI-driven analytics continue to drive the adoption of advanced EDI solutions, reshaping the global landscape of healthcare data exchange.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory support and compliance requirements

- 3.2.1.2 Rising demand for interoperability

- 3.2.1.3 Technological advancements

- 3.2.1.4 Cost reduction and efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Innovation landscape

- 3.8 Gap analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Solutions

Chapter 6 Market Estimates and Forecast, By Deployment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Web and cloud-based EDI

- 6.3 EDI value added network (VAN)

- 6.4 Direct (point-to-point) EDI

- 6.5 Mobile EDI

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare payers

- 7.3 Healthcare providers

- 7.4 Pharmaceutical and medical device industries

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Boomi

- 9.2 Cleo

- 9.3 DataTrans Solutions

- 9.4 Effective Data

- 9.5 Epicor Software Corporation

- 9.6 GE Healthcare

- 9.7 MCKESSON CORPORATION

- 9.8 NXGN Management

- 9.9 OpenText

- 9.10 Optum

- 9.11 Oracle

- 9.12 OSP

- 9.13 SPS Commerce

- 9.14 SSI Group

- 9.15 TrueCommerce

全球醫療保健電子資料交換 (EDI) 市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球醫療保健電子資料交換 (EDI) 市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 全球醫療保健 EDI 市場(至 2029 年):按傳輸(加值網路和點對點)、軟體、供應(採購和庫存)、服務、最終用戶(醫院、ASC、付款人)和地區分類

全球醫療保健 EDI 市場(至 2029 年):按傳輸(加值網路和點對點)、軟體、供應(採購和庫存)、服務、最終用戶(醫院、ASC、付款人)和地區分類 2025 年醫療保健 EDI 全球市場報告

2025 年醫療保健 EDI 全球市場報告 2025 年醫療保健電子資料交換全球市場報告

2025 年醫療保健電子資料交換全球市場報告 醫療保健電子資料交換市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按交付模式、按最終用戶、按地區和按競爭進行細分,2020-2030 年預測

醫療保健電子資料交換市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按交付模式、按最終用戶、按地區和按競爭進行細分,2020-2030 年預測 醫療保健電子資料交換市場規模、佔有率、成長分析,按組件、按交付、按最終用途、按地區 - 行業預測,2024-2031 年

醫療保健電子資料交換市場規模、佔有率、成長分析,按組件、按交付、按最終用途、按地區 - 行業預測,2024-2031 年 醫療保健 EDI 市場:按組成部分、交易類型、交付模式和最終用戶 - 2025-2030 年全球預測

醫療保健 EDI 市場:按組成部分、交易類型、交付模式和最終用戶 - 2025-2030 年全球預測 醫療保健電子資料交換 (EDI) 市場,按產品類型、交易類型、交付模式、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

醫療保健電子資料交換 (EDI) 市場,按產品類型、交易類型、交付模式、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 全球醫療保健電子資料交換 (EDI) 市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測

全球醫療保健電子資料交換 (EDI) 市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測 亞太地區醫療保健電子資料交換市場規模和預測、區域佔有率、趨勢和成長機會分析報告範圍:按組件、交付模式、應用程式、最終用戶和區域分析

亞太地區醫療保健電子資料交換市場規模和預測、區域佔有率、趨勢和成長機會分析報告範圍:按組件、交付模式、應用程式、最終用戶和區域分析