|

市場調查報告書

商品編碼

1665103

數位射線成像市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測Digital Radiography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

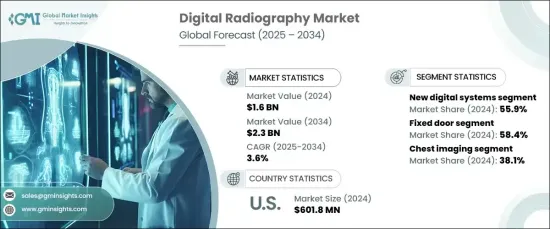

2024 年全球數位放射市場規模達到 16 億美元,預計將呈現穩定成長的軌跡,2025 年至 2034 年的複合年成長率為 3.6%。隨著醫院和診斷中心面臨越來越大的壓力,需要提供更快、更準確的診斷結果,對數位放射系統的需求顯著增加。這些系統提高了成像品質並減少了產生結果所需的時間,使得它們在快節奏的醫療保健環境中不可或缺。此外,隨著對以患者為中心的護理和簡化的工作流程的日益重視,醫療保健提供者正在轉向能夠實現更高效和更精確診斷的數位放射解決方案。

從傳統的基於膠片的放射線照相術向數位系統的轉變是該市場成長的最重要驅動力之一。醫療保健提供者正在大力投資對其成像基礎設施進行現代化改造,以提高營運效率、增強診斷準確性並在日益技術驅動的行業中保持競爭力。這種轉變在那些尋求採用最新技術來滿足不斷變化的醫療保健需求的機構中尤其明顯。作為這種轉變的一部分,數位放射系統提供了廣泛的好處,從更快的影像處理時間到與電子健康記錄 (EHR) 和醫院管理系統更好地整合。隨著醫療保健需求的不斷發展,數位放射成像將在推動診斷成像的未來發展中發揮關鍵作用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 16億美元 |

| 預測值 | 23億美元 |

| 複合年成長率 | 3.6% |

根據產品,市場分為固定門和攜帶式數位放射成像系統。固定門系統佔據市場主導地位,到 2024 年將佔據 58.4% 的佔有率。攜帶式數位放射成像系統(如行動和手持設備)也因其在不同醫療保健環境中的便利性和多功能性而越來越受歡迎。

就系統類型而言,市場分為新數位系統和改造系統。 2024 年,新型數位系統將佔據 55.9% 的市場佔有率,這得益於先進平板探測器、人工智慧成像工具以及與醫院管理系統的無縫整合等尖端技術。這些先進技術以具有競爭力的價格提供,再加上對醫療設備製造商的支持性補貼,促進了該領域的成長。

2024 年,北美數位放射學市場創收 6.018 億美元,這得益於公共和私營部門對醫療保健基礎設施的大量投資。旨在增強診斷成像能力和整合健康 IT 系統的政策持續推動市場成長。美國憑藉其完善的醫療保健網路和快速採用創新醫療技術,仍然是區域市場擴張的關鍵參與者。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 診斷領域數位化趨勢日益增強

- 數位放射攝影系統的技術進步

- 醫療機構對降低營運成本的需求日益增加

- 診斷環境中的負擔不斷增加

- 產業陷阱與挑戰

- 數位放射成像系統成本高

- 與資料隱私和安全相關的擔憂

- 成長動力

- 成長潛力分析

- 專利分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望

第 5 章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 固定門數位射線攝影系統

- 天花板安裝系統

- 落地式安裝系統

- 攜帶式數位放射攝影系統

- 移動系統

- 手持系統

第6章:市場估計與預測:按類型,2021 – 2034 年

- 主要趨勢

- 新的數位系統

- 改造數位系統

第 7 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 胸部影像學

- 心血管影像

- 骨科成像

- 兒科影像

- 其他應用

第 8 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 診斷影像中心

- 骨科診所

- 其他最終用戶

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AGFA- Gevaert Group

- BPL Medical Technologies

- Canon

- Carestream Health

- Fujifilm Holdings Corporation

- GE Healthcare

- Konica Minolta

- Koninklijke Phillips NV

- MinXray

- Samsung Medison

- Shanghai United Imaging Healthcare

- Shenzhen Mindray Bio-medical Electronics

- Shimadzu Corporation

- Siemens Healthineers AG

- SternMed GmbH

The Global Digital Radiography Market reached USD 1.6 billion in 2024 and is projected to experience a steady growth trajectory, expanding at a CAGR of 3.6% from 2025 to 2034. Several critical factors are contributing to this growth, including the rapid adoption of digital technologies in diagnostic settings, continuous advancements in imaging technologies, and the drive to reduce operational costs within healthcare facilities. With hospitals and diagnostic centers under increasing pressure to provide faster, more accurate diagnostic results, the demand for digital radiography systems has risen significantly. These systems enhance imaging quality and reduce the time needed to produce results, making them indispensable in a fast-paced healthcare environment. Furthermore, with an increasing emphasis on patient-centered care and streamlined workflows, healthcare providers are turning to digital radiography solutions that enable more efficient and precise diagnoses.

The transition from traditional film-based radiography to digital systems represents one of the most significant drivers of growth in this market. Healthcare providers are investing heavily in modernizing their imaging infrastructure to improve operational efficiency, enhance diagnostic accuracy, and stay competitive in an increasingly technology-driven industry. This shift is particularly evident in facilities that seek to embrace the latest technologies to address evolving healthcare demands. As part of this transformation, digital radiography systems offer a wide range of benefits, from faster image processing times to better integration with electronic health records (EHR) and hospital management systems. As healthcare needs continue to evolve, digital radiography will play a pivotal role in driving the future of diagnostic imaging.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 3.6% |

By product, the market is divided into fixed-door and portable digital radiography systems. Fixed-door systems dominate the market, accounting for a substantial share of 58.4% in 2024. This is largely due to their widespread use in large hospitals, imaging centers, and trauma care units, where they handle high patient volumes and enable rapid image processing. Portable digital radiography systems, such as mobile and handheld devices, are also gaining traction for their convenience and versatility in diverse healthcare environments.

In terms of system type, the market is segmented into new digital systems and retrofit systems. New digital systems made up 55.9% of the market in 2024, driven by cutting-edge technologies like advanced flat-panel detectors, artificial intelligence-powered imaging tools, and seamless integration with hospital management systems. The availability of these advanced technologies at competitive prices, coupled with supportive subsidies for medical equipment manufacturers, has contributed to the growth of this segment.

North America digital radiography market generated USD 601.8 million in 2024, fueled by substantial investments in healthcare infrastructure from both the public and private sectors. Policies aimed at enhancing diagnostic imaging capabilities and integrating health IT systems continue to bolster market growth. The United States, with its well-established healthcare network and rapid adoption of innovative medical technologies, remains a key player in regional market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing digitalization trends across diagnostic settings

- 3.2.1.2 Technological advancements in digital radiography systems

- 3.2.1.3 Rising demand for reducing operational cost across healthcare facilities

- 3.2.1.4 Growing burden across diagnostic settings

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of digital radiography systems

- 3.2.2.2 Concerns related to data privacy and security

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Fixed door digital radiography systems

- 5.2.1 Ceiling-mounted systems

- 5.2.2 Floor-to-ceiling mounted systems

- 5.3 Portable digital radiography systems

- 5.3.1 Mobile systems

- 5.3.2 Handheld systems

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 New digital systems

- 6.3 Retrofit digital systems

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chest imaging

- 7.3 Cardiovascular imaging

- 7.4 Orthopedic imaging

- 7.5 Pediatric imaging

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic imaging centers

- 8.4 Orthopedic clinics

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AGFA- Gevaert Group

- 10.2 BPL Medical Technologies

- 10.3 Canon

- 10.4 Carestream Health

- 10.5 Fujifilm Holdings Corporation

- 10.6 GE Healthcare

- 10.7 Konica Minolta

- 10.8 Koninklijke Phillips N.V.

- 10.9 MinXray

- 10.10 Samsung Medison

- 10.11 Shanghai United Imaging Healthcare

- 10.12 Shenzhen Mindray Bio-medical Electronics

- 10.13 Shimadzu Corporation

- 10.14 Siemens Healthineers AG

- 10.15 SternMed GmbH

2025 年至 2033 年數位 X 光設備市場報告(按便攜性、系統、應用、最終用途和地區分類)

2025 年至 2033 年數位 X 光設備市場報告(按便攜性、系統、應用、最終用途和地區分類) 動態數位射線照相市場,按應用、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

動態數位射線照相市場,按應用、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 醫療數位影像系統市場規模、佔有率和成長分析(按類型、技術和地區)- 產業預測 2025-2032

醫療數位影像系統市場規模、佔有率和成長分析(按類型、技術和地區)- 產業預測 2025-2032 醫療數位影像系統市場規模、佔有率、趨勢分析報告:按組件、模式、部署模式、應用、最終用途、地區和細分市場分類,預測至 2025-2030 年

醫療數位影像系統市場規模、佔有率、趨勢分析報告:按組件、模式、部署模式、應用、最終用途、地區和細分市場分類,預測至 2025-2030 年 2024 年醫療數位影像系統全球市場報告

2024 年醫療數位影像系統全球市場報告 數位 X 光市場規模、佔有率、成長分析,按類型、技術、便攜性、系統、價格分佈、應用、最終用戶、地區 - 行業預測,2024-2031 年

數位 X 光市場規模、佔有率、成長分析,按類型、技術、便攜性、系統、價格分佈、應用、最終用戶、地區 - 行業預測,2024-2031 年 數位 X 光市場:按技術、便攜性、應用和最終用戶分類 - 2025-2030 年全球預測

數位 X 光市場:按技術、便攜性、應用和最終用戶分類 - 2025-2030 年全球預測 數位 X 光設備市場、規模、佔有率、趨勢、行業分析報告(按產品、類型、應用、最終用戶和地區)- 市場預測,2025-2034 年

數位 X 光設備市場、規模、佔有率、趨勢、行業分析報告(按產品、類型、應用、最終用戶和地區)- 市場預測,2025-2034 年 數位乳房X光攝影市場報告:2030 年趨勢、預測與競爭分析

數位乳房X光攝影市場報告:2030 年趨勢、預測與競爭分析 數位X光市場,佔有率,規模,趨勢,產業分析報告:各類型,各技術,攜帶,各系統,各種價格,各用途,各終端用戶,各地區 - 市場預測 2025年~2034年

數位X光市場,佔有率,規模,趨勢,產業分析報告:各類型,各技術,攜帶,各系統,各種價格,各用途,各終端用戶,各地區 - 市場預測 2025年~2034年