|

市場調查報告書

商品編碼

1665177

持針器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Needle Holders Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

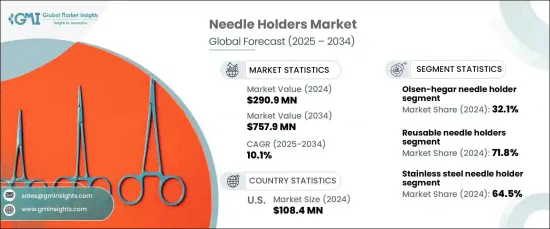

2024 年全球持針器市場價值為 2.909 億美元,將經歷強勁的成長軌跡,預計 2025 年至 2034 年的複合年成長率為 10.1%。此外,機器人輔助手術的進步也推動了對這些儀器的需求,因為它們為複雜的手術提供了必要的靈活性和穩定性。心血管疾病、糖尿病和癌症等需要手術介入的慢性病的增加也促進了市場的擴大。外科醫生越來越依賴持針器等先進、高品質的儀器在手術過程中執行精細的任務,這使得它們在現代手術室中不可或缺。此外,生物相容性材料的創新提高了持針器的安全性和效率,並持續推動市場成長。

持針器市場多種多樣,其類型多種多樣,旨在滿足不同外科專業的獨特需求。其中,Olsen-Hegar 持針器佔據領先地位,2024 年佔據 32.1% 的市場佔有率。這種組合可以使程式更加高效,特別是在速度和準確性至關重要的環境中。外科醫生欣賞該工具的易用性、成本效益和多功能設計,這有助於其廣泛採用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.909 億美元 |

| 預測值 | 7.579 億美元 |

| 複合年成長率 | 10.1% |

在應用方面,心血管領域脫穎而出,到 2024 年將佔據 22.6% 的市場佔有率。隨著心血管手術需求的增加,包括持針器在內的高品質精密器械市場也正在成長。這些手術要求極高的精確度,進一步刺激了對支持精細手術的持針器市場的需求。

美國仍然是全球持針器市場最大的貢獻者之一,2024 年的市場規模為 1.084 億美元。隨著美國醫療保健產業採用更先進的技術,對持針器等專用儀器的需求持續激增,特別是那些設計用於需要高精度的機器人系統儀器的需求。全國持續採用尖端手術解決方案預計將進一步推動市場擴張。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 微創手術需求不斷成長

- 機器人輔助手術的出現

- 生物相容性和專用材料的進展

- 需要手術介入的慢性病數量成長

- 產業陷阱與挑戰

- 存在嚴格的規定

- 仿冒品的供應

- 成長動力

- 成長潛力分析

- 專利分析

- 差距分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- Olsen-Hegar持針器

- Mayo-hegar持針器

- 韋伯斯特持針器

- Mathieu 持針器

- Halsey 持針器

- 克里爾伍德持針器

- Derf 持針器

- 其他類型

第 6 章:市場估計與預測:按用途,2021 年至 2034 年

- 主要趨勢

- 可重複使用持針器

- 免洗持針器

第 7 章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 不銹鋼持針器

- 碳化鎢持針器

- 其他材料

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 心血管

- 胃腸道

- 胸椎

- 骨科

- 牙科

- 眼科

- 泌尿科

- 婦科

- 其他應用

第 9 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用途

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- A. Schweickhardt

- August Reuchlen

- B. Braun Melsungen

- Baxter International

- Becton, Dickinson and Company

- Hologic (Somatex Medical Technologies)

- Hu-Friedy Mfg

- Johnson & Johnson

- KLS Martin Group

- MedGyn Products

- Medline Industries

- Nordent Manufacturing

- Olympus Corporation

- Sklar Instruments

- Towne Brothers

The Global Needle Holders Market, valued at USD 290.9 million in 2024, is set to experience a robust growth trajectory, with a projected CAGR of 10.1% from 2025 to 2034. The demand for needle holders is being significantly driven by the growing preference for minimally invasive surgeries, which require specialized tools to ensure precision and safety. Additionally, advancements in robotic-assisted procedures are fueling the need for these instruments, as they offer the necessary dexterity and stability for complex surgeries. The rise in chronic conditions that require surgical intervention, such as cardiovascular diseases, diabetes, and cancer, also contributes to the expanding market. Surgeons increasingly rely on advanced, high-quality instruments like needle holders to perform delicate tasks during procedures, making them indispensable in modern operating rooms. Furthermore, innovations in biocompatible materials, enhancing both the safety and efficiency of needle holders, continue to propel market growth.

The market for needle holders is diverse, with a wide array of types designed to meet the unique demands of different surgical specialties. Among these, the Olsen-Hegar needle holder is the leader, commanding a 32.1% share of the market in 2024. Its dual functionality, combining both a needle holder and scissors, makes it a popular choice for surgeries requiring precise suturing and cutting. This combination allows for more efficient procedures, especially in settings where speed and accuracy are crucial. Surgeons appreciate the tool's ease of use, cost-effectiveness, and versatile design, which contributes to its broad adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $290.9 Million |

| Forecast Value | $757.9 Million |

| CAGR | 10.1% |

In terms of application, the cardiovascular segment stands out, holding a notable 22.6% share of the market in 2024. The surge in global cardiovascular diseases, such as heart disease and hypertension, directly impacts the demand for needle holders designed for these specialized surgeries. As the need for cardiovascular surgeries increases, the market for high-quality, precision instruments, including needle holders, also rises. These surgeries demand the utmost accuracy, further bolstering the market for needle holders that can support delicate operations.

The U.S. remains one of the largest contributors to the global needle holders market, generating USD 108.4 million in 2024. This growth is largely attributed to the rise in minimally invasive surgery and the increasing use of robotic-assisted surgical techniques. As the healthcare sector in the U.S. embraces more advanced technologies, the demand for specialized instruments like needle holders continues to surge, particularly those designed for use with robotic systems that require exceptional precision. The ongoing adoption of cutting-edge surgical solutions across the country is expected to further drive market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for minimally invasive surgeries

- 3.2.1.2 Emergence of robot-assisted surgical procedures

- 3.2.1.3 Advancements in biocompatible and specialized materials

- 3.2.1.4 Growth in chronic diseases requiring surgical interventions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Presence of stringent regulations

- 3.2.2.2 Availability of counterfeit products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Gap analysis

- 3.6 Regulatory landscape

- 3.7 Technological landscape

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Olsen-hegar needle holder

- 5.3 Mayo-hegar needle holder

- 5.4 Webster needle holder

- 5.5 Mathieu needle holder

- 5.6 Halsey needle holder

- 5.7 Crilewood needle holder

- 5.8 Derf needle holder

- 5.9 Other types

Chapter 6 Market Estimates and Forecast, By Usage, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Reusable needle holder

- 6.3 Single-use needle holder

Chapter 7 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Stainless steel needle holder

- 7.3 Tungsten carbide needle holder

- 7.4 Other materials

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Cardiovascular

- 8.3 Gastrointestinal

- 8.4 Thoracic

- 8.5 Orthopedic

- 8.6 Dental

- 8.7 Ophthalmic

- 8.8 Urology

- 8.9 Gynecology

- 8.10 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 A. Schweickhardt

- 11.2 August Reuchlen

- 11.3 B. Braun Melsungen

- 11.4 Baxter International

- 11.5 Becton, Dickinson and Company

- 11.6 Hologic (Somatex Medical Technologies)

- 11.7 Hu-Friedy Mfg

- 11.8 Johnson & Johnson

- 11.9 KLS Martin Group

- 11.10 MedGyn Products

- 11.11 Medline Industries

- 11.12 Nordent Manufacturing

- 11.13 Olympus Corporation

- 11.14 Sklar Instruments

- 11.15 Towne Brothers

持針器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、最終用途、地區和競爭細分,2020-2030 年預測2025 年全球電動手術器械市場報告

持針器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、最終用途、地區和競爭細分,2020-2030 年預測2025 年全球電動手術器械市場報告 電動手術器械市場按產品類型、應用、最終用戶和地區分類2025 年手持式手術器械全球市場報告手持式手術器械市場規模、佔有率、成長分析、按產品、按應用、按最終用途、按地區 - 行業預測,2025-2032 年2024年食道擴張器全球市場報告

電動手術器械市場按產品類型、應用、最終用戶和地區分類2025 年手持式手術器械全球市場報告手持式手術器械市場規模、佔有率、成長分析、按產品、按應用、按最終用途、按地區 - 行業預測,2025-2032 年2024年食道擴張器全球市場報告 手持式手術器材市場規模、佔有率、趨勢分析報告:按產品、按應用、按最終用途、按地區、細分市場預測,2025-2030 年

手持式手術器材市場規模、佔有率、趨勢分析報告:按產品、按應用、按最終用途、按地區、細分市場預測,2025-2030 年 全球手持式微創手術器材市場 - 2024-2031

全球手持式微創手術器材市場 - 2024-2031 手持式手術器械市場報告:2030 年趨勢、預測與競爭分析

手持式手術器械市場報告:2030 年趨勢、預測與競爭分析 動力手術器材市場:按產品和應用分類的全球預測 - 2025-2030

動力手術器材市場:按產品和應用分類的全球預測 - 2025-2030