|

市場調查報告書

商品編碼

1665240

單極電外科器械市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測Monopolar Electrosurgery Instrument Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

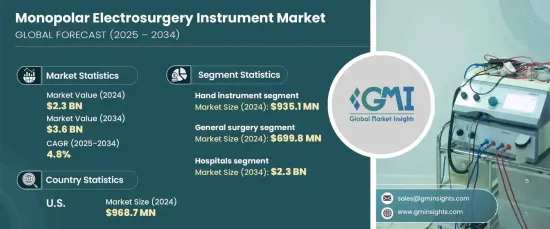

2024 年全球單極電外科器械市場規模達到 23 億美元,預計將經歷強勁成長,2025 年至 2034 年的複合年成長率預計為 4.8%。這一成長是由全球對微創手術的需求不斷成長、慢性病患病率擴大以及醫療保健投資不斷上升所推動的。此外,技術進步和對精密手術器械日益成長的需求正在推動市場上漲。

微創手術已成為一般外科、婦科、泌尿科和胃腸病學等各醫學專業的標準做法。單極電外科器械因其精確度、效率以及在手術過程中最大限度減少組織損傷的能力而在這些領域發揮著至關重要的作用。它們在切割、凝固和乾燥組織方面的多功能性使其成為常規和複雜手術中不可或缺的工具。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 23億美元 |

| 預測值 | 36億美元 |

| 複合年成長率 | 4.8% |

市場按產品類型細分,包括手動器械、電外科發生器、分散電極和配件。手動器械部分在 2024 年以 9.351 億美元的收入領先市場。它們對開放性手術和微創手術的適應性確保它們仍然佔據主導地位,滿足廣泛的醫療需求。

根據應用,市場分為一般外科、心血管外科、婦科、神經外科和其他。 2024 年一般外科手術收入為 6.998 億美元,預計預測期內複合年成長率為 4.6%。單極電外科器械因其在處理軟組織、止血和減少手術時間方面的效率而在該領域受到高度評價。它們能夠改善手術效果並促進患者更快康復,從而繼續推動醫院和外科中心的需求。

2024 年,美國單極電外科器械市場產值達 9.687 億美元。慢性病的日益普及和微創手術的日益普及導致了對這些儀器的持續需求。此外,先進的醫療培訓和專業知識進一步加速了單極電外科器械的採用,鞏固了美國在全球市場的領導地位。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 微創手術需求不斷成長

- 電外科技術的進步

- 慢性病盛行率不斷上升

- 全球醫療支出不斷上漲

- 產業陷阱與挑戰

- 熱傷害風險高

- 成長動力

- 成長潛力分析

- 監管格局

- 報銷場景

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按產品類型,2021 年至 2034 年

- 主要趨勢

- 手用儀器

- 電外科發電機

- 分散電極

- 配件

第 6 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 一般外科

- 心血管外科

- 婦科手術

- 神經外科

- 其他應用

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用戶

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Apyx Medical

- B.Braun

- BOWA MEDICAL

- CONMED

- Encision

- Erbe Elektromedizin

- Johnson & Johnson

- KLS Martin Group

- Medtronic

- Meyer-Haake

- Olympus

- Stryker

The Global Monopolar Electrosurgery Instrument Market reached USD 2.3 billion in 2024 and is expected to experience strong growth, with a projected CAGR of 4.8% from 2025 to 2034. This growth is driven by the increasing demand for minimally invasive procedures, the rising prevalence of chronic diseases, and expanding healthcare investments around the world. Additionally, technological advancements and the growing need for precise surgical instruments are fueling the market's upward trajectory.

Minimally invasive procedures have become standard practice across various medical specialties such as general surgery, gynecology, urology, and gastroenterology. Monopolar electrosurgery instruments play a crucial role in these fields due to their precision, efficiency, and ability to minimize tissue damage during surgical procedures. Their versatility in cutting, coagulating, and desiccating tissues makes them indispensable for both routine and complex surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.8% |

The market is segmented into product types, including hand instruments, electrosurgical generators, dispersive electrodes, and accessories. The hand instrument segment led the market with a revenue of USD 935.1 million in 2024. These instruments are widely used across numerous surgical disciplines, offering the precision and control required for delicate procedures. Their adaptability to both open and minimally invasive surgeries ensures they remain the dominant segment, addressing a wide array of medical needs.

In terms of application, the market is divided into general surgery, cardiovascular surgery, gynecology, neurosurgery, and others. General surgery accounted for USD 699.8 million in 2024 and is projected to grow at a CAGR of 4.6% during the forecast period. Monopolar electrosurgery instruments are highly regarded in this segment for their efficiency in managing soft tissues, providing hemostasis, and reducing surgical time. Their ability to enhance surgical outcomes and promote faster patient recovery continues to drive demand across hospitals and surgical centers.

The U.S. monopolar electrosurgery instrument market generated USD 968.7 million in 2024. This market is expected to grow at a CAGR of 4.2% through 2034, supported by the presence of leading manufacturers and a well-established healthcare infrastructure. The growing prevalence of chronic conditions and the increasing adoption of minimally invasive procedures contribute to sustained demand for these instruments. Additionally, the availability of advanced medical training and expertise further accelerates the adoption of monopolar electrosurgery instruments, reinforcing the U.S.'s leadership position in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for minimally invasive procedures

- 3.2.1.2 Advancements in electrosurgical technologies

- 3.2.1.3 Growing prevalence of chronic diseases

- 3.2.1.4 Rising global healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of thermal injuries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hand instrument

- 5.3 Electrosurgical generators

- 5.4 Dispersive electrodes

- 5.5 Accessories

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Cardiovascular surgery

- 6.4 Gynecology surgery

- 6.5 Neurosurgery

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Apyx Medical

- 9.2 B.Braun

- 9.3 BOWA MEDICAL

- 9.4 CONMED

- 9.5 Encision

- 9.6 Erbe Elektromedizin

- 9.7 Johnson & Johnson

- 9.8 KLS Martin Group

- 9.9 Medtronic

- 9.10 Meyer-Haake

- 9.11 Olympus

- 9.12 Stryker

單極電外科器械市場,按手術類型、按功率輸出、按電極類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

單極電外科器械市場,按手術類型、按功率輸出、按電極類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 2025年全球電外科增強輸送系統市場報告2025年全球電外科發電機市場報告

2025年全球電外科增強輸送系統市場報告2025年全球電外科發電機市場報告 電外科設備市場按產品類型、應用、最終用戶和地區分類

電外科設備市場按產品類型、應用、最終用戶和地區分類 全球電外科發電機市場:市場規模、佔有率、趨勢分析(按類型、產品、應用、最終用途和地區)、細分市場預測(2025-2030 年)雙極電外科設備市場規模、佔有率、趨勢分析報告(按產品、應用、最終用途、地區、細分市場預測),2025 年至 2030 年

全球電外科發電機市場:市場規模、佔有率、趨勢分析(按類型、產品、應用、最終用途和地區)、細分市場預測(2025-2030 年)雙極電外科設備市場規模、佔有率、趨勢分析報告(按產品、應用、最終用途、地區、細分市場預測),2025 年至 2030 年 全球電外科設備市場 - 2025 - 2033電外科市場規模、佔有率、成長分析、按產品、按手術、按地區 - 產業預測,2025-2032 年

全球電外科設備市場 - 2025 - 2033電外科市場規模、佔有率、成長分析、按產品、按手術、按地區 - 產業預測,2025-2032 年 單極電外科設備的全球市場:成長,未來展望,競爭分析 (2025年~2033年)電外科設備市場規模、佔有率、成長分析、按產品類型、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年

單極電外科設備的全球市場:成長,未來展望,競爭分析 (2025年~2033年)電外科設備市場規模、佔有率、成長分析、按產品類型、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年