|

市場調查報告書

商品編碼

1665297

神經痛治療市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Neuralgia Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

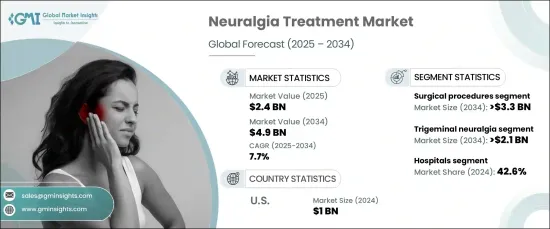

2024 年全球神經痛治療市場價值為 24 億美元,將經歷大幅成長,預計 2025 年至 2034 年的複合年成長率為 7.7%。

神經系統疾病,特別是各種形式的神經痛發生率的上升是推動市場擴張的關鍵因素。隨著對這些疾病的認知不斷提高,越來越多的人開始尋求早期診斷和治療。公眾意識運動和改進的診斷能力在早期發現神經痛方面發揮了重要作用,推動了針對三叉神經痛、帶狀皰疹後神經痛和其他形式的神經相關疼痛的治療需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 24億美元 |

| 預測值 | 49億美元 |

| 複合年成長率 | 7.7% |

市場依各種神經痛病症進行細分,包括三叉神經痛、帶狀皰疹後神經痛、枕神經痛等。其中,三叉神經痛預計成長最快,預計複合年成長率為 7.9%,到 2034 年將達到 21 億美元。這導致對更好治療方案的需求增加,進一步推動市場成長。

從最終用戶的角度來看,醫院預計將推動神經痛治療市場的大幅成長。憑藉 MRI 和 CT 掃描等先進的診斷工具,醫院仍然是進行全面診斷和治療的首選場所。這些尖端技術使醫療保健提供者能夠準確識別不同類型的神經痛,確保患者接受最有效和最有針對性的治療。提供精準診斷能力的能力使醫院成為治療複雜神經系統疾病最值得信賴和最可靠的環境,從而確保了其在市場上的主導地位。

在美國,神經痛治療市場預計將在預測期內實現強勁成長。該國先進的醫療保健基礎設施,包括最先進的影像技術、手術技術和藥理創新,繼續支持其市場領導地位。隨著人口老化,人們特別容易患上三叉神經痛和帶狀皰疹後神經痛等疾病,對有效治療的需求日益增加。此外,優惠的報銷政策和主要製藥公司在研發方面的大量投入也促進了市場的擴張,確保美國在全球神經痛治療領域仍佔有重要地位。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 神經系統疾病盛行率上升

- 疼痛管理技術的進步

- 提高認知和診斷率

- 產業陷阱與挑戰

- 先進療法成本高昂

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 報銷場景

- 差距分析

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按治療類型,2021 - 2034 年

- 主要趨勢

- 外科手術

- 射頻熱損傷

- 立體定位放射外科

- 顯微血管減壓術

- 其他外科手術

- 藥物

- 抗驚厥藥

- 抗憂鬱藥

- 其他藥物

第 6 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 三叉神經痛

- 帶狀皰疹後神經痛

- 枕神經痛

- 其他應用

第 7 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 診所

- 門診手術中心

- 其他最終用戶

第 8 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- AA pharma

- astellas

- Biogen

- Eli Lilly

- Johnson & Johnson

- Medtronic

- NOVARTIS

- PACIRA BIOSCIENCES

- Pfizer

- Siemens Healthineers

The Global Neuralgia Treatment Market, valued at USD 2.4 billion in 2024, is set to experience substantial growth, with a projected CAGR of 7.7% from 2025 to 2034. This growth is primarily driven by the increasing prevalence of neurological disorders and advancements in awareness, diagnosis, and treatment options.

The rising incidence of neurological conditions, particularly various forms of neuralgia, is a key factor fueling market expansion. As awareness surrounding these disorders grows, more individuals are seeking early diagnosis and treatment. Public awareness campaigns and improved diagnostic capabilities have played a significant role in detecting neuralgia at earlier stages, driving demand for therapies that target conditions like trigeminal neuralgia, postherpetic neuralgia, and other forms of nerve-related pain.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 7.7% |

The market is segmented by various neuralgia conditions, including trigeminal neuralgia, postherpetic neuralgia, occipital neuralgia, and others. Among these, trigeminal neuralgia is expected to see the highest growth, with a projected CAGR of 7.9%, reaching USD 2.1 billion by 2034. Trigeminal neuralgia, one of the most common types of neuralgia, especially affects older populations and can severely impact daily activities and overall quality of life. This has led to increased demand for better treatment options, further propelling market growth.

From the perspective of end-users, hospitals are projected to drive substantial growth in the neuralgia treatment market. With advanced diagnostic tools like MRI and CT scans, hospitals remain the preferred setting for comprehensive diagnosis and treatment. These cutting-edge technologies enable healthcare providers to accurately identify different types of neuralgia, ensuring that patients receive the most effective and targeted treatments. The ability to offer precise diagnostic capabilities makes hospitals the most trusted and reliable environments for treating complex neurological conditions, thus securing their dominance in the market.

In the U.S., the neuralgia treatment market is expected to see robust growth during the forecast period. The country's advanced healthcare infrastructure, featuring state-of-the-art imaging technologies, surgical techniques, and pharmacological innovations, continues to support its market leadership. With an aging population that is particularly vulnerable to conditions like trigeminal and postherpetic neuralgia, the demand for effective treatments is escalating. Furthermore, favorable reimbursement policies and significant investments in research and development by major pharmaceutical companies are contributing to the market's expansion, ensuring that the U.S. remains a key player in the global neuralgia treatment landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of neurological disorders

- 3.2.1.2 Advancements in pain management technologies

- 3.2.1.3 Increase in awareness and diagnosis rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical procedures

- 5.2.1 Radiofrequency thermal lesioning

- 5.2.2 Stereotactic radiosurgery

- 5.2.3 Microvascular decompression

- 5.2.4 Other surgical procedures

- 5.3 Medications

- 5.3.1 Anticonvulsants

- 5.3.2 Antidepressants

- 5.3.3 Other medications

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Trigeminal neuralgia

- 6.3 Postherpetic neuralgia

- 6.4 Occipital neuralgia

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AA pharma

- 9.2 astellas

- 9.3 Biogen

- 9.4 Eli Lilly

- 9.5 Johnson & Johnson

- 9.6 Medtronic

- 9.7 NOVARTIS

- 9.8 PACIRA BIOSCIENCES

- 9.9 Pfizer

- 9.10 Siemens Healthineers

神經痛治療市場-全球產業規模、佔有率、趨勢、機會和預測,按治療、適應症、配銷通路、地區和競爭細分,2020-2030 年

神經痛治療市場-全球產業規模、佔有率、趨勢、機會和預測,按治療、適應症、配銷通路、地區和競爭細分,2020-2030 年 糖尿病神經性疼痛市場-全球產業規模、佔有率、趨勢、機會和預測,按神經病變類型、藥物類別、配銷通路、地區和競爭情況細分,2020 年至 2030 年

糖尿病神經性疼痛市場-全球產業規模、佔有率、趨勢、機會和預測,按神經病變類型、藥物類別、配銷通路、地區和競爭情況細分,2020 年至 2030 年 2030 年神經病變疼痛市場預測:按藥物類別、適應症、患者類型、給藥途徑、分銷管道和地區進行的全球分析

2030 年神經病變疼痛市場預測:按藥物類別、適應症、患者類型、給藥途徑、分銷管道和地區進行的全球分析 黏液囊炎治療市場:按類型、藥物類型、最終用戶分類 - 全球預測 2025-2030

黏液囊炎治療市場:按類型、藥物類型、最終用戶分類 - 全球預測 2025-2030 神經痛治療藥物市場:依藥物類型、給藥途徑、嚴重程度、通路及地區分類

神經痛治療藥物市場:依藥物類型、給藥途徑、嚴重程度、通路及地區分類 神經痛治療市場規模、佔有率、趨勢分析報告:按治療、按最終用途、按地區、細分市場預測,2025-2030 年

神經痛治療市場規模、佔有率、趨勢分析報告:按治療、按最終用途、按地區、細分市場預測,2025-2030 年 三叉神經痛治療藥物市場:按產品,按最終用戶 - 全球預測 2025-2030

三叉神經痛治療藥物市場:按產品,按最終用戶 - 全球預測 2025-2030 神經疼痛治療藥物市場:按治療方法、適應症、分銷管道 - 全球預測 2025-2030

神經疼痛治療藥物市場:按治療方法、適應症、分銷管道 - 全球預測 2025-2030 神經病變疼痛治療市場:按疼痛類型、適應症、治療方法、分銷管道和最終用戶分類 - 2025-2030 年全球預測

神經病變疼痛治療市場:按疼痛類型、適應症、治療方法、分銷管道和最終用戶分類 - 2025-2030 年全球預測 神經病變疼痛治療市場:按類型、治療方法、適應症、分佈、最終用戶 - 全球預測 2025-2030

神經病變疼痛治療市場:按類型、治療方法、適應症、分佈、最終用戶 - 全球預測 2025-2030