|

市場調查報告書

商品編碼

1665335

汽車熱電發電機市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Automotive Thermoelectric Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

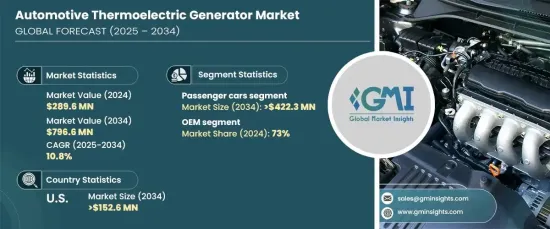

2024 年全球汽車熱電發電機市場價值為 2.896 億美元,將經歷強勁成長,預計 2025 年至 2034 年的複合年成長率為 10.8%。 這一成長是由燃料成本的上升和旨在減少汽車排放的政府法規日益嚴格所推動的。因此,對提高燃油效率和減少環境影響的技術的需求正在激增。

推動這一市場擴張的一個重要因素是電動和混合動力汽車的日益普及。這些先進的車輛依靠能源管理系統來最佳化電池性能和行駛里程。 ATEG 將排氣系統產生的廢熱轉化為可用電能,在這項最佳化過程中發揮關鍵作用。透過為輔助系統供電並支援電池充電,這些發電機有助於提高現代車輛的能源效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.896 億美元 |

| 預測值 | 7.966 億美元 |

| 複合年成長率 | 10.8% |

就車輛類型而言,市場分為乘用車、商用車、混合動力和電動車。 2024年,乘用車將引領市場,佔57%的市佔率。受乘用車大規模生產和燃油效率技術需求不斷成長的推動,預計到 2034 年,該領域將創收 4.223 億美元。 ATEG 在乘用車中的廣泛應用為能量回收系統的創新和整合創造了巨大的機會,確保了該領域的持續成長。

根據銷售管道,市場進一步分為原始設備製造商 (OEM) 和售後市場。到 2024 年,OEM 將佔據 73% 的佔有率,預計這一趨勢將在整個預測期內持續下去。 OEM 擅長在製造過程中將 ATEG 無縫整合到車輛中,確保相容性和最佳化性能。透過滿足汽車製造商的大量訂單,原始設備製造商實現了成本效率,同時加速了這些技術的採用。此外,他們的技術專長使他們能夠設計適合特定車輛架構的系統,從而提高整體效率和可靠性。

在美國,汽車熱電發電機市場在 2024 年佔據了令人印象深刻的 86% 的佔有率,預計到 2034 年將達到 1.526 億美元。美國市場也受惠於對高檔和豪華汽車的高需求,這些汽車擴大採用先進的節油系統。此外,大量研發投入,加上領先的 ATEG 製造商的存在,促進了創新並支持了市場的成長軌跡。

報告內容

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 技術提供者

- 零件供應商

- 製造商

- 原始設備製造商

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 對燃油效率的需求不斷增加

- 嚴格的排放法規

- 電動和混合動力車的普及率不斷提高

- 熱電材料的技術進步

- 產業陷阱與挑戰

- 技術初始成本高

- 消費者認知度有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 碲化鉍

- 碲化鉛

- 矽鍺

- 其他

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 商用車

- 混合動力和電動車

第 7 章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 廢熱回收

- 發電

- 電池管理

第 8 章:市場估計與預測:按銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Alphabet Energy

- European Thermodynamics

- Faurecia

- Ferrotec Holdings Corporation

- Gentherm Incorporated

- Hi-Z Technology, Inc.

- II-VI Marlow

- KELK Ltd.

- Komatsu Ltd.

- Laird Thermal Systems

- SANGO Co., Ltd.

- Tenneco Inc.

- Thermonamic Electronics (Jiangxi) Corp., Ltd.

- Valeo

- Yamaha Motor Co., Ltd.

The Global Automotive Thermoelectric Generator Market, valued at USD 289.6 million in 2024, is set to experience robust growth, projected at a CAGR of 10.8% from 2025 to 2034. This growth is driven by the rising costs of fuel and increasingly stringent government regulations aimed at reducing vehicle emissions. As a result, the demand for technologies that enhance fuel efficiency and minimize environmental impact is surging.

A significant driver of this market expansion is the growing popularity of electric and hybrid vehicles. These advanced vehicles rely on energy management systems to optimize battery performance and driving range. ATEGs, which convert waste heat from exhaust systems into usable electricity, play a pivotal role in this optimization. By powering auxiliary systems and supporting battery charging, these generators contribute to enhanced energy efficiency in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $289.6 Million |

| Forecast Value | $796.6 Million |

| CAGR | 10.8% |

In terms of vehicle type, the market is segmented into passenger cars, commercial vehicles, and hybrid and electric vehicles. Passenger cars led the market in 2024, commanding 57% of the market share. This segment is forecasted to generate USD 422.3 million by 2034, fueled by the mass production of passenger vehicles and the increasing demand for fuel-efficient technologies. The widespread adoption of ATEGs in passenger cars creates substantial opportunities for innovation and integration of energy recovery systems, ensuring continuous growth in this segment.

The market is further categorized based on sales channels into original equipment manufacturers (OEMs) and aftermarket. In 2024, OEMs dominated with a 73% share, a trend expected to persist throughout the forecast period. OEMs excel in seamlessly incorporating ATEGs into vehicles during the manufacturing process, ensuring compatibility and optimized performance. By fulfilling bulk orders for automakers, OEMs achieve cost efficiencies while accelerating the adoption of these technologies. Additionally, their technical expertise enables them to design systems tailored to specific vehicle architectures, enhancing overall efficiency and reliability.

In the United States, the automotive thermoelectric generator market held an impressive 86% share in 2024 and is projected to reach USD 152.6 million by 2034. Stringent fuel efficiency and emissions regulations, including the Corporate Average Fuel Economy (CAFE) standards, are key drivers of this demand. The U.S. market also benefits from a high demand for premium and luxury vehicles, which increasingly incorporate advanced fuel-saving systems. Furthermore, significant investments in research and development, coupled with the presence of leading ATEG manufacturers, foster innovation and support the market's growth trajectory.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing demand for fuel efficiency

- 3.7.1.2 Stringent emission regulations

- 3.7.1.3 Growing adoption of electric and hybrid vehicles

- 3.7.1.4 Technological advancements in thermoelectric materials

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial cost of technology

- 3.7.2.2 Limited awareness among consumers

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Bismuth telluride

- 5.3 Lead telluride

- 5.4 Silicon germanium

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

- 6.4 Hybrid and electric vehicles

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Waste heat recovery

- 7.3 Power generation

- 7.4 Battery management

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alphabet Energy

- 10.2 European Thermodynamics

- 10.3 Faurecia

- 10.4 Ferrotec Holdings Corporation

- 10.5 Gentherm Incorporated

- 10.6 Hi-Z Technology, Inc.

- 10.7 II-VI Marlow

- 10.8 KELK Ltd.

- 10.9 Komatsu Ltd.

- 10.10 Laird Thermal Systems

- 10.11 SANGO Co., Ltd.

- 10.12 Tenneco Inc.

- 10.13 Thermonamic Electronics (Jiangxi) Corp., Ltd.

- 10.14 Valeo

- 10.15 Yamaha Motor Co., Ltd.

全球熱電半導體發電機市場分析與預測(至2033年):類型、產品、服務、技術、組件、應用、材料類型、最終用戶、功能、安裝類型

全球熱電半導體發電機市場分析與預測(至2033年):類型、產品、服務、技術、組件、應用、材料類型、最終用戶、功能、安裝類型 熱電發電機市場:依應用、溫度範圍、行業、地區

熱電發電機市場:依應用、溫度範圍、行業、地區 汽車熱電發電機市場:按組件、材料、溫度、應用、車輛類型分類 - 2025-2030 年全球預測

汽車熱電發電機市場:按組件、材料、溫度、應用、車輛類型分類 - 2025-2030 年全球預測 熱電發電機市場規模、佔有率、成長分析,按組件、類型、材料、應用、溫度、功率、最終用戶、地區 - 產業預測,2024-2031

熱電發電機市場規模、佔有率、成長分析,按組件、類型、材料、應用、溫度、功率、最終用戶、地區 - 產業預測,2024-2031 熱電發電機市場:現狀分析與未來預測 (2024年~2032年)

熱電發電機市場:現狀分析與未來預測 (2024年~2032年) 熱電發電機市場:按組件、溫度、材料、應用、產業分類 - 全球預測 20

熱電發電機市場:按組件、溫度、材料、應用、產業分類 - 全球預測 20 全球熱電發電機市場

全球熱電發電機市場 2024-2032 年按組件、材料(矽化鎂、碲化鉍、碲化鉛、方鈷礦)、車輛類型、應用和地區分類的汽車熱電發電機市場報告

2024-2032 年按組件、材料(矽化鎂、碲化鉍、碲化鉛、方鈷礦)、車輛類型、應用和地區分類的汽車熱電發電機市場報告 2022-2029年全球汽車熱電發馬達市場規模研究與預測,按類型(冷卻板、熱電模組、熱交換器、其他)按應用(乘用車、商用車)和區域分析

2022-2029年全球汽車熱電發馬達市場規模研究與預測,按類型(冷卻板、熱電模組、熱交換器、其他)按應用(乘用車、商用車)和區域分析![熱電發電機市場:趨勢、機遇、競爭分析 [2023-2028]](/sample/img/cover/42/1284987.png) 熱電發電機市場:趨勢、機遇、競爭分析 [2023-2028]

熱電發電機市場:趨勢、機遇、競爭分析 [2023-2028]