|

市場調查報告書

商品編碼

1665402

汽車皮帶起動發電機市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Automotive Belt Starter Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

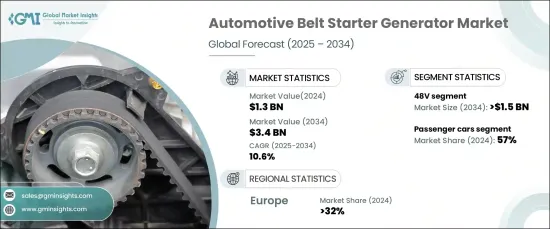

2024 年全球汽車皮帶起動發電機市場價值為 13 億美元,預計 2025 年至 2034 年的複合年成長率為 10.6%。這些系統透過提供更高的功率輸出,表現優於傳統的 12V 系統,從而提高了輕度混合動力系統的效率。它們還增強了再生煞車能力,在煞車過程中捕獲和儲存更多能量以最佳化燃油效率。透過減少引擎的工作負荷並實現更好的能源管理,這些系統對交通的永續性做出了重大貢獻。

向混合動力車和電動車的轉變也在推動 BSG 市場發展方面發揮關鍵作用。汽車製造商正在整合這些系統以符合更嚴格的排放法規並滿足對環保行動解決方案日益成長的需求。 BSG 系統結合了起動馬達和發電機功能,是混合動力和電動動力系統的重要組成部分。它們提高了能源利用率,支持再生煞車並增強了車輛的整體性能,使其成為向更環保的汽車技術轉型的關鍵創新。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 34億美元 |

| 複合年成長率 | 10.6% |

市場按產品細分為 12V 和 48V 系統。 2024 年,48V 市場佔據了 58% 以上的市場佔有率,預計到 2034 年將超過 15 億美元。它們可確保更平穩的加速、更高的燃油經濟性和更有效的能量回收,成為汽車製造商應對嚴格排放標準的理想選擇。

就車輛類型而言,市場分為乘用車、非公路用車和商用車。 2024 年,乘用車約佔 57% 的市場佔有率。啟動停止功能、再生煞車和內燃機附加扭力等特性使這些系統對乘用車領域極具吸引力,進一步推動了其市場滲透。

歐洲成為領先地區,到 2024 年將佔據全球 32% 以上的市場佔有率,其中德國貢獻巨大。印度汽車產業發展強勁,主要參與者大力投資混合動力和電動車技術,支撐了其主導地位。嚴格的二氧化碳排放限制法規和對永續交通的關注,使得汽車製造商廣泛採用 48V BSG 系統,鞏固了德國在市場上的領導地位。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 汽車原廠設備製造商

- 技術提供者

- 售後市場和服務提供商

- 最終用戶

- 利潤率分析

- 成本明細分析

- 技術與創新格局

- 重要新聞及舉措

- 定價分析

- 監管格局

- 衝擊力

- 成長動力

- 排放法規執行日益嚴格

- 對燃油效率的需求日益成長

- 混合動力汽車和電動車的普及率不斷提高

- 成長動力

3.9.1.4.提高 48 V 系統的性能和成本效益

- 皮帶起動發電機設計的技術進步

- 產業陷阱與挑戰

- 技術和整合挑戰

- 全混合動力和電動動力系統的競爭

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 輕度混合動力

- 微混合動力

第 6 章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 12伏

- 48伏

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- 越野車

- 掀背車

- 商用車

- 輕型商用車

- 丙型肝炎病毒

- 越野車

第 8 章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 電動機/發電機

- 電力電子

- 機械耦合

- 控制系統

第 9 章:市場估計與預測:按冷卻類型,2021 - 2034 年

- 主要趨勢

- 空氣冷卻

- 液冷

- 混合冷卻

第 10 章:市場估計與預測:按銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第 11 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 12 章:公司簡介

- Bosch

- Continental

- Dayco

- Hyundai

- Infineon

- Magneti Marelli

- MTA

- Nexteer

- Onsemi

- Schaeffler Group

- SEG Automotive

- Sona Comstar

- Syensqo

- Valeo

- Vitesco Technologies

- ZF Friedrichshafen

The Global Automotive Belt Starter Generator Market was valued at USD 1.3 billion in 2024 and is anticipated to grow at a CAGR of 10.6% from 2025 to 2034. The increasing demand for 48V systems, known for their superior performance and affordability, is propelling the adoption of BSG systems, particularly in mild-hybrid vehicles. These systems outperform traditional 12V counterparts by delivering higher power output, which boosts the efficiency of mild-hybrid powertrains. They also enhance regenerative braking capabilities, capturing and storing more energy during braking to optimize fuel efficiency. By reducing the engine's workload and enabling better energy management, these systems contribute significantly to sustainability in transportation.

The shift towards hybrid and electric vehicles also plays a critical role in driving the BSG market. Automakers are integrating these systems to align with stricter emissions regulations and meet the growing demand for eco-friendly mobility solutions. BSG systems, which combine starter motor and generator functions, are vital components in hybrid and electric powertrains. They improve energy utilization, support regenerative braking, and enhance overall vehicle performance, making them a key innovation in the transition to greener automotive technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 10.6% |

The market is segmented by product into 12V and 48V systems. In 2024, the 48V segment accounted for over 58% of the market share and is projected to surpass USD 1.5 billion by 2034. These systems are preferred due to their ability to deliver additional electrical power for critical vehicle functions like electric power steering, air conditioning, and regenerative braking. They ensure smoother acceleration, improved fuel economy, and more effective energy recovery, positioning themselves as the ideal choice for automakers addressing stringent emissions standards.

In terms of vehicle type, the market is categorized into passenger cars, off-highway vehicles, and commercial vehicles. Passenger cars held approximately 57% of the market share in 2024. These vehicles leverage 48V BSG systems to achieve better fuel efficiency and reduced emissions, catering to consumers seeking cost-effective solutions without transitioning fully to electric vehicles. Features like start-stop functionality, regenerative braking, and additional torque for internal combustion engines make these systems highly attractive for the passenger car segment, further driving their market penetration.

Europe emerged as the leading region, capturing more than 32% of the global market share in 2024, with Germany being a significant contributor. The country's robust automotive sector, featuring key players heavily investing in hybrid and electric vehicle technologies, supports this dominance. Strict regulations to curb CO2 emissions and a focus on sustainable transportation have led to widespread adoption of 48V BSG systems among automakers, reinforcing Germany's leadership in the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Automotive OEMs

- 3.2.2 Technology providers

- 3.2.3 Aftermarket and service providers

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Pricing analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising implementation of stringent emission regulations

- 3.9.1.2 Growing demand for fuel efficiency

- 3.9.1.3 Increasing adoption of hybrid and electric vehicles

- 3.9.1 Growth drivers

3.9.1.4. Improved performance and cost-effectiveness of 48 V systems

- 3.9.1.5 Technological advancements in belt starter generator design

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Technological and integration challenges

- 3.9.2.2 Competition from full hybrid and electric powertrains

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Mild hybrid

- 5.3 Micro hybrid

Chapter 6 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 12V

- 6.3 48V

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 HCV

- 7.4 Off highway vehicle

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Motor/generator

- 8.3 Power electronics

- 8.4 Mechanical coupling

- 8.5 Control systems

Chapter 9 Market Estimates & Forecast, By Cooling Type, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Air-cooled

- 9.3 Liquid-cooled

- 9.4 Hybrid-cooled

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Bosch

- 12.2 Continental

- 12.3 Dayco

- 12.4 Hyundai

- 12.5 Infineon

- 12.6 Magneti Marelli

- 12.7 MTA

- 12.8 Nexteer

- 12.9 Onsemi

- 12.10 Schaeffler Group

- 12.11 SEG Automotive

- 12.12 Sona Comstar

- 12.13 Syensqo

- 12.14 Valeo

- 12.15 Vitesco Technologies

- 12.16 ZF Friedrichshafen

汽車皮帶和軟管市場-全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、皮帶類型、軟管類型、地區和競爭細分,2020-2030 年

汽車皮帶和軟管市場-全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、皮帶類型、軟管類型、地區和競爭細分,2020-2030 年 汽車引擎皮帶和軟管市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年)

汽車引擎皮帶和軟管市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年) 汽車皮帶市場:按材料、特性和應用分類 - 2025-2030 年全球預測非汽車橡膠傳動帶市場、佔有率、規模、趨勢、產業分析報告:依產品、應用、地區、細分市場預測,2024-2032

汽車皮帶市場:按材料、特性和應用分類 - 2025-2030 年全球預測非汽車橡膠傳動帶市場、佔有率、規模、趨勢、產業分析報告:依產品、應用、地區、細分市場預測,2024-2032 橡膠傳動帶市場 - 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測

橡膠傳動帶市場 - 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測 輸送帶布料市場:趨勢,機會,競爭分析【2023-2028年】

輸送帶布料市場:趨勢,機會,競爭分析【2023-2028年】