|

市場調查報告書

商品編碼

1665414

石油和天然氣檢查無人機市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測Inspection Drone in Oil and Gas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

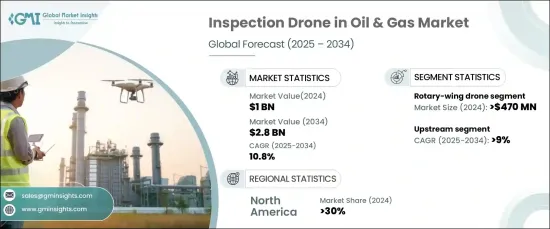

2024 年全球石油和天然氣檢查無人機市場價值為 10 億美元,預計 2025 年至 2034 年期間的複合年成長率為 10.8%。公司正在優先開發創新的檢查系統以改善營運、降低風險和提高安全性。無人機擴大用於進行例行檢查、評估基礎設施和監控營運,大大改變了該領域的傳統檢查實踐。更嚴格的安全和環境合規監管要求也推動了無人機技術的採用,因為無人機技術比傳統方法提供了更快、更可靠的替代方案。此外,將人工智慧和機器學習融入無人機系統正在徹底改變資料分析,以實現即時洞察並簡化決策流程。對自動化和營運效率的關注繼續影響著市場的發展軌跡。

市場依無人機類型分為旋翼無人機、固定翼無人機和混合無人機。旋翼無人機在 2024 年佔據了相當大的市場佔有率,價值超過 4.7 億美元。這些無人機因其能夠在狹小空間內懸停和機動的能力而受到廣泛青睞,使其成為檢查管道和海上平台等固定資產的理想選擇。它們的使用提高了安全性和效率,同時減少了傳統檢查方法所需的時間和成本。隨著公司擴大融入人工智慧技術,對旋翼無人機的需求預計將進一步成長,以提供基於即時資料的更好決策能力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 10億美元 |

| 預測值 | 28億美元 |

| 複合年成長率 | 10.8% |

根據營運類型,市場也分為上游、中游和下游部分。預計 2025 年至 2034 年間,上游產業將實現超過 9% 的強勁複合年成長率。無人機透過提高安全性、最大限度地減少檢查時間並最佳化營運成本,正在成為上游運作不可或缺的工具。對探勘活動的投資增加和對永續性的關注進一步擴大了該領域對巡檢無人機的需求。

2024 年,北美引領全球市場,佔超過 30% 的營收佔有率。尤其是美國,由於重視營運效率和遵守嚴格的安全法規,取得了顯著的成長。人工智慧和機器學習等先進技術融入無人機系統,可實現即時資料分析,幫助公司簡化流程、快速識別潛在問題並減少停機時間。該地區對創新和效率的高度重視繼續推動市場成長。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 組件提供者

- 製造商

- 經銷商

- 最終用途

- 利潤率分析

- 技術與創新格局

- 專利分析

- 監管格局

- 使用案例

- 使用案例1

- 好處

- 投資報酬率

- 使用案例2

- 好處

- 投資報酬率

- 使用案例1

- 案例研究

- 案例研究 1

- 消費者姓名

- 挑戰

- 解決方案

- 影響

- 案例研究 2

- 消費者姓名

- 挑戰

- 解決方案

- 影響

- 案例研究 1

- 衝擊力

- 成長動力

- 即時監控需求日益增加

- 無人機技術進步

- 資產管理解決方案需求不斷成長

- 增強遠端檢查的安全協議

- 產業陷阱與挑戰

- 資料整合和分析面臨的挑戰

- 實施先進無人機系統成本高昂

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按無人機,2021 - 2034 年

- 主要趨勢

- 固定翼無人機

- 旋翼無人機

- 混合無人機

第6章:市場估計與預測:依酬載,2021 - 2034 年

- 主要趨勢

- 相機

- LiDAR

- 氣體探測器

- 其他

第 7 章:市場估計與預測:按營運,2021 - 2034 年

- 主要趨勢

- 上游

- 中游

- 下游

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 管道檢查

- 火炬塔檢查

- 油罐檢查

- 環境監測

- 井場檢查

- 其他

第 9 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 國家石油公司 (NOC)

- 獨立石油公司 (IOC)

第 10 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- 3D Robotics

- Airobotics

- Autel Robotics

- Cyberhawk

- DJI Enterprise

- DroneBase

- DroneDeploy

- FLIR Systems

- Flyability

- GRIFF Aviation

- IdeaForge

- InspecTech Aero Services

- Kespry

- Percepto

- PrecisionHawk

- Quantum Systems

- senseFly

- Sky-Futures (ICR Group)

- Terra Drone

- Vantage Robotics

The Global Inspection Drone In Oil And Gas Market was valued at USD 1 billion in 2024 and is projected to grow at a CAGR of 10.8% from 2025 to 2034. This growth is fueled by the rising demand for efficient monitoring solutions and the rapid advancements in drone technology. Companies are prioritizing the development of innovative inspection systems to improve operations, reduce risks, and enhance safety. The increasing use of drones to conduct routine checks, assess infrastructure, and monitor operations has significantly transformed traditional inspection practices in the sector. Stricter regulatory requirements for safety and environmental compliance are also driving the adoption of drone technologies, which offer a faster and more reliable alternative to conventional methods. Additionally, incorporating AI and machine learning into drone systems is revolutionizing data analysis, enabling real-time insights and streamlined decision-making processes. The focus on automation and operational efficiency continues to shape the market's trajectory.

The market is segmented by drone type into rotary-wing, fixed-wing, and hybrid drones. Rotary-wing drones held a substantial market share in 2024, exceeding USD 470 million in value. These drones are widely preferred due to their ability to hover and maneuver in confined spaces, making them ideal for inspecting stationary assets like pipelines and offshore platforms. Their use enhances safety and efficiency while reducing the time and cost associated with traditional inspection methods. As companies increasingly integrate AI-enabled technologies, the demand for rotary-wing drones is expected to grow further, offering improved decision-making capabilities based on real-time data.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 10.8% |

The market is also categorized by operation type into upstream, midstream, and downstream segments. The upstream segment is forecasted to witness a robust CAGR of over 9% between 2025 and 2034. This growth is attributed to the rising need for advanced monitoring of exploration sites, drilling operations, and pipelines, especially in remote and challenging locations. Drones are becoming an indispensable tool for upstream operations by enhancing safety, minimizing inspection times, and optimizing operational costs. Increased investments in exploration activities and a focus on sustainability further amplify the demand for inspection drones in this segment.

North America led the global market in 2024, capturing over 30% of the revenue share. The United States, in particular, has seen significant growth due to its emphasis on operational efficiency and compliance with stringent safety regulations. The integration of advanced technologies like AI and machine learning into drone systems is enabling real-time data analysis, helping companies streamline processes, identify potential issues quickly, and reduce downtime. The region's strong focus on innovation and efficiency continues to bolster market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturer

- 3.2.3 Distributors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Used cases

- 3.7.1 Used case 1

- 3.7.1.1 Benefits

- 3.7.1.2 ROI

- 3.7.2 Used case 2

- 3.7.2.1 Benefits

- 3.7.2.2 ROI

- 3.7.1 Used case 1

- 3.8 Case study

- 3.8.1 Case study 1

- 3.8.1.1 Consumer name

- 3.8.1.2 Challenge

- 3.8.1.3 Solution

- 3.8.1.4 Impact

- 3.8.2 Case study 2

- 3.8.2.1 Consumer name

- 3.8.2.2 Challenge

- 3.8.2.3 Solution

- 3.8.2.4 Impact

- 3.8.1 Case study 1

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for real-time monitoring

- 3.9.1.2 Technological advancements in drone capabilities

- 3.9.1.3 Rising demand for asset management solutions

- 3.9.1.4 Enhanced safety protocols for remote inspections

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Challenges in data integration and analysis

- 3.9.2.2 High costs associated with implementing advanced drone systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Drone, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Fixed-wing drone

- 5.3 Rotary-wing drone

- 5.4 Hybrid drone

Chapter 6 Market Estimates & Forecast, By Payload, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Cameras

- 6.3 LiDAR

- 6.4 Gas detectors

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Upstream

- 7.3 Midstream

- 7.4 Downstream

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Pipeline inspection

- 8.3 Flare stack inspection

- 8.4 Tank inspection

- 8.5 Environmental monitoring

- 8.6 Well site inspection

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 National Oil Companies (NOCs)

- 9.3 Independent Oil Companies (IOCs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 3D Robotics

- 11.2 Airobotics

- 11.3 Autel Robotics

- 11.4 Cyberhawk

- 11.5 DJI Enterprise

- 11.6 DroneBase

- 11.7 DroneDeploy

- 11.8 FLIR Systems

- 11.9 Flyability

- 11.10 GRIFF Aviation

- 11.11 IdeaForge

- 11.12 InspecTech Aero Services

- 11.13 Kespry

- 11.14 Percepto

- 11.15 PrecisionHawk

- 11.16 Quantum Systems

- 11.17 senseFly

- 11.18 Sky-Futures (ICR Group)

- 11.19 Terra Drone

- 11.20 Vantage Robotics