|

市場調查報告書

商品編碼

1666540

汽車數據線市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Automotive Data Cables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

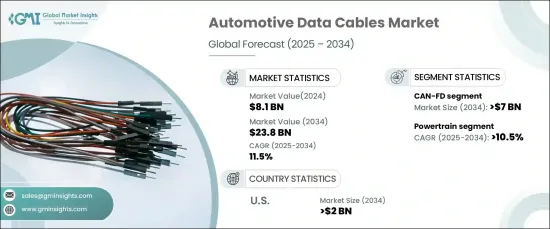

2024 年全球汽車數據線市場價值為 81 億美元,預計 2025 年至 2034 年期間將以 11.5% 的複合年成長率快速成長。這些技術進步導致對車輛高效資料傳輸和連接的需求不斷增加。汽車產業對感測器、攝影機和資訊娛樂系統等電子元件的依賴日益增加,極大地促進了對高品質汽車資料線的需求。此外,在政府支持措施的支持下,車對車(V2V)和車對基礎設施(V2I)技術的擴展正在加速電子系統的開發和應用,進一步推動市場向前發展。

隨著基礎設施不斷改善,特別是對智慧城市和互聯交通的關注,對汽車資料線的需求日益加劇。主要製造商在全球擴大生產設施進一步支持了這一成長。透過最佳化生產流程和縮短交貨時間,公司能夠更好地滿足符合當地偏好和監管標準的車輛日益成長的區域需求。這些努力不僅加強了產業的供應鏈,也促進了電子元件的創新,從而推動了汽車產業對資料線的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 81億美元 |

| 預測值 | 238億美元 |

| 複合年成長率 | 11.5% |

CAN-FD(控制器資料網路靈活資料速率)部門預計到 2034 年將產生 70 億美元的收入。汽車製造商正在大力投資增強 CAN-FD 技術,以支援汽車和工業領域日益複雜的應用。 CAN-FD 解決方案的持續開發對於滿足現代車輛的需求至關重要,因為現代車輛需要更快、更可靠的資料傳輸以實現最佳性能。

此外,動力總成領域也將經歷顯著成長,預計到 2034 年複合年成長率將達到 10.5%。隨著汽車製造商採用先進的電子設備和車載電腦網路來滿足現代動力系統的高資料要求,該領域對汽車資料線的需求持續上升。動力系統日益複雜,再加上尖端電氣技術的整合,為強大的資料線提供了機會,可實現車輛功能的無縫資料交換,支援車輛的整體性能和效率。

預計到 2034 年,美國汽車資料線市場規模將達到資料億美元。美國的原始設備製造商 (OEM) 專注於改進車輛設計以納入更多的電子系統,導致資料線的需求激增。先進電子設備與動力傳動技術整合進一步推動了這一趨勢,以電子控制取代了傳統的機械系統,從而提高了車輛的效率和性能。

目錄

第 1 章:方法論與範圍

- 市場定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

第4章:競爭格局

- 介紹

- 戰略儀表板

- 創新與永續發展格局

第 5 章:市場規模與預測:按電纜,2021 – 2034 年

- 主要趨勢

- 控制器區域網路 (CAN)

- 控制器區域網路靈活資料速率 (CAN-FD)

- FlexRay

- 乙太網路

- 低電壓差分訊號 (LVDS)/高速資料 (HSD)

- 同軸電纜

第6章:市場規模及預測:依車型,2021 – 2034 年

- 主要趨勢

- 搭乘用車

- 商用車

第 7 章:市場規模與預測:按應用,2021 – 2034 年

- 主要趨勢

- 動力傳動系統

- 車身控制與舒適度

- 資訊娛樂與通訊

- 安全性與 ADAS

第 8 章:市場規模與預測:按地區,2021 – 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳新銀行

- 中東和非洲

- 南非

- 海灣合作理事會

- 土耳其

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第9章:公司簡介

- ACOME

- Amphenol

- Aptiv

- Belden

- Champlain

- Coficab

- Condumex

- Coroplast

- Furukawa

- Gebauer

- HUBER+SUHNER

- ITC

- Lear

- Leoni

- Prysmian

- Salcavi

- Sumitomo

- Waytek

- Yazaki

The Global Automotive Data Cables Market, valued at USD 8.1 billion in 2024, is expected to grow rapidly at a CAGR of 11.5% between 2025 and 2034. This surge in demand is driven by the increasing integration of advanced electronic systems into modern vehicles, coupled with the implementation of stricter safety standards and regulations within the automotive sector. These technological advancements have led to the rising need for efficient data transfer and connectivity in vehicles. The automotive industry's growing reliance on electronic components, including sensors, cameras, and infotainment systems, has significantly contributed to the demand for high-quality automotive data cables. Moreover, the expansion of vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) technologies, backed by supportive government initiatives, is accelerating the development and adoption of electronic systems, further pushing the market forward.

As infrastructure continues to improve, especially with the focus on smart cities and connected transportation, the demand for automotive data cables is intensifying. This growth is further supported by key manufacturers expanding their production facilities globally. By optimizing production processes and reducing lead times, companies are better able to cater to the growing regional demand for vehicles that meet local preferences and regulatory standards. These efforts are not only strengthening the industry's supply chain but also fostering innovation in electronic components, boosting the demand for data cables in the automotive sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $23.8 Billion |

| CAGR | 11.5% |

The CAN-FD (Controller Area Network Flexible Data-rate) segment is expected to generate USD 7 billion in revenue by 2034. CAN-FD technology, known for its ability to facilitate rapid and efficient data transfer, has become essential for modern vehicles that require high-speed communication between systems. Automotive manufacturers are investing significantly in the enhancement of CAN-FD technology to support increasingly complex applications within both automotive and industrial sectors. This ongoing development of CAN-FD solutions is critical to meeting the demands of modern vehicles, which require faster, more reliable data transmission for optimal performance.

Additionally, the powertrain segment is set to experience significant growth, with a projected CAGR of 10.5% through 2034. The shift towards electric vehicles (EVs) is playing a major role in this growth. As automotive manufacturers adopt advanced electronics and onboard computer networks to meet the high data requirements of modern powertrains, the need for automotive data cables in this sector continues to rise. The increasing complexity of powertrain systems, coupled with the integration of cutting-edge electric technologies, presents an opportunity for robust data cables to enable seamless data exchange for vehicle functions, supporting overall vehicle performance and efficiency.

The U.S. automotive data cables market is projected to reach USD 2 billion by 2034. The rapid transition toward electric vehicles, driven by growing consumer interest and environmental considerations, has significantly increased the demand for sophisticated electronic components, including automotive data cables. Original equipment manufacturers (OEMs) in the U.S. are focused on advancing vehicle designs to incorporate more electronic systems, creating a surge in demand for data cables. This trend is further fueled by the integration of advanced electronics in powertrain technologies, replacing traditional mechanical systems with electronic controls, thus enhancing vehicle efficiency and performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Cable, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Controller Area Network (CAN)

- 5.3 Controller Area Network Flexible Data-Rate (CAN-FD)

- 5.4 FlexRay

- 5.5 Ethernet

- 5.6 Low Voltage Differential Signaling (LVDS)/High Speed Data (HSD)

- 5.7 Coaxial Cables

Chapter 6 Market Size and Forecast, By Vehicle, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.3 Commercial Vehicles

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Powertrain

- 7.3 Body Control & Comfort

- 7.4 Infotainment & Communication

- 7.5 Safety & ADAS

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 ANZ

- 8.5 Middle East & Africa

- 8.5.1 South Africa

- 8.5.2 GCC

- 8.5.3 Turkey

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ACOME

- 9.2 Amphenol

- 9.3 Aptiv

- 9.4 Belden

- 9.5 Champlain

- 9.6 Coficab

- 9.7 Condumex

- 9.8 Coroplast

- 9.9 Furukawa

- 9.10 Gebauer

- 9.11 HUBER+SUHNER

- 9.12 ITC

- 9.13 Lear

- 9.14 Leoni

- 9.15 Prysmian

- 9.16 Salcavi

- 9.17 Sumitomo

- 9.18 Waytek

- 9.19 Yazaki

汽車資料線市場規模、佔有率及成長分析(按電纜、車輛、應用和地區)- 2025-2032 年產業預測

汽車資料線市場規模、佔有率及成長分析(按電纜、車輛、應用和地區)- 2025-2032 年產業預測 電動車高壓電纜的全球市場機會與策略(截至 2034 年)

電動車高壓電纜的全球市場機會與策略(截至 2034 年) 高壓汽車市場按組件類型、推進系統、車輛類型、用途、應用領域和最終用戶分類 - 2025-2030 年全球預測2025年全球汽車電纜市場報告2025 年全球汽車資料線市場報告

高壓汽車市場按組件類型、推進系統、車輛類型、用途、應用領域和最終用戶分類 - 2025-2030 年全球預測2025年全球汽車電纜市場報告2025 年全球汽車資料線市場報告 汽車數據線市場,按電纜類型、按應用、按材料、按車輛類型、按國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測汽車油門電纜市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、車輛類型、銷售通路類型、地區和競爭細分,2020-2030F汽車電纜市場:按絕緣材料、屏蔽類型、元件、電壓、應用和最終用途分類 - 2025-2030 年全球預測電動車電纜市場:按電動車類型、絕緣材料、屏蔽類型、組件、電壓、應用分類 - 2025-2030 年全球預測電動車高壓電纜市場:按電纜類型、材料、電壓範圍、應用和車輛類型分類 - 2025-2030 年全球預測

汽車數據線市場,按電纜類型、按應用、按材料、按車輛類型、按國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測汽車油門電纜市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、車輛類型、銷售通路類型、地區和競爭細分,2020-2030F汽車電纜市場:按絕緣材料、屏蔽類型、元件、電壓、應用和最終用途分類 - 2025-2030 年全球預測電動車電纜市場:按電動車類型、絕緣材料、屏蔽類型、組件、電壓、應用分類 - 2025-2030 年全球預測電動車高壓電纜市場:按電纜類型、材料、電壓範圍、應用和車輛類型分類 - 2025-2030 年全球預測