|

市場調查報告書

商品編碼

1666580

重型卡車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Heavy Duty Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

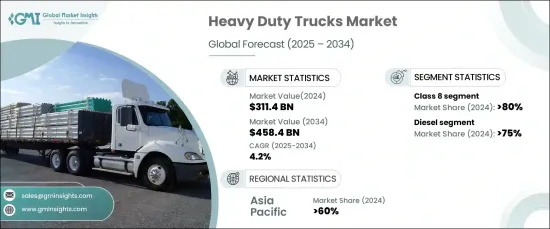

2024 年全球重型卡車市場價值為 3,114 億美元,預計 2025 年至 2034 年期間的複合年成長率為 4.2%。跨境貿易發展勢頭強勁,需要能夠長距離處理大量貨物的先進重型車輛。各地區為簡化貿易物流和改善基礎設施而進行的合作努力,正在促進重型卡車,特別是 8 級車輛的普及。

技術創新正在重塑市場格局,提高車輛性能、安全性和營運效率。自動駕駛、遠端資訊處理和連接解決方案等先進功能擴大整合到重型卡車中,使其對車隊營運商更具吸引力。這些技術最佳化了車隊管理,提高了駕駛員安全性,降低了營運成本,從而促進了對現代化卡車車型的需求。隨著車隊營運商優先考慮性能和成本效率,全球採用技術先進的重型卡車的現象正在增加。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3114億美元 |

| 預測值 | 4584億美元 |

| 複合年成長率 | 4.2% |

市場按車輛等級細分,其中 8 級卡車佔據主導地位,到 2024 年佔據 80% 以上的市場佔有率。他們高效長距離運輸重物的能力鞏固了他們在全球供應鏈中的地位。此外,節油引擎和智慧系統等尖端功能的結合使其成為車隊營運商的首選。

燃料類型細分顯示柴油卡車佔據主導地位,到 2024 年,柴油卡車佔據了 75% 以上的市場佔有率。其持續的突出地位得益於完善的加油基礎設施,確保了無縫運作。儘管人們逐漸轉向替代燃料,但柴油卡車憑藉其久經考驗的性能和多功能性仍然是重型運輸的基石。

亞太地區引領重型卡車市場,到 2023 年將貢獻 60% 的收入佔有率。電子商務行業的蓬勃發展和物流網路的不斷擴大進一步增加了對重型卡車的需求。此外,政府主導的基礎設施計劃和經濟發展策略繼續推動該地區的市場成長。隨著亞太地區作為全球經濟中心的地位不斷加強,重型卡車市場預計將保持強勁勢頭。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 原物料供應商

- 零件供應商

- 製造商

- 技術提供者

- 經銷商

- 最終用途

- 利潤率分析

- 技術與創新格局

- 專利分析

- 監管格局

- 定價分析

- 衝擊力

- 成長動力

- 自動駕駛技術需求不斷成長

- 長途貨運活動增加,重型卡車利用率提高

- 由於法規嚴格,引進先進的排放控制系統

- 全球物流網路與電子商務的擴張

- 卡車運輸效率和安全性能的技術進步

- 產業陷阱與挑戰

- 先進技術整合成本高

- 經濟放緩影響貨運需求

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按類別,2021 - 2034 年

- 主要趨勢

- 第七類

- 車軸類型

- 4X2

- 6X2

- 6X4

- 車軸類型

- 第八類

- 車軸類型

- 4X2

- 6X2

- 6X4

- 駕駛室類型

- 日間計程車

- 臥舖司機室

- 車軸類型

第6章:市場估計與預測:按燃料,2021 - 2034 年

- 主要趨勢

- 柴油引擎

- 天然氣

- 油電混合

- 汽油

第7章:市場估計與預測:按馬力,2021 - 2034 年

- 主要趨勢

- 300HP以下

- 300馬力至400馬力

- 400馬力至500馬力

- 500HP以上

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 貨運配送

- 實用程式服務

- 建築和採礦

- 其他

第 9 章:市場估計與預測:按所有權分類,2021 - 2034 年

- 主要趨勢

- 車隊營運商

- 獨立營運商

第 10 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 俄羅斯

- 比利時

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- BYD Auto

- Daimler Trucks

- Dongfeng

- Freightliner

- Hino Motors

- Isuzu Motors

- Kenworth

- MAN

- Navistar

- PACCAR Inc

- Peterbilt

- SCANIA

- SINOTRUK

- TRATON GROUP

- Volvo

The Global Heavy Duty Trucks Market was valued at USD 311.4 billion in 2024 and is expected to grow at a CAGR of 4.2% from 2025 to 2034. This growth is largely attributed to the increasing global need for efficient goods transportation, driven by thriving commerce and expanding trade activities. Cross-border trade has gained momentum, necessitating advanced heavy-duty vehicles capable of handling substantial cargo volumes over long distances. Collaborative efforts among regions to streamline trade logistics and improve infrastructure are bolstering the adoption of heavy-duty trucks, particularly Class 8 vehicles.

Technological innovations are reshaping the market landscape, enhancing vehicle performance, safety, and operational efficiency. Advanced features like autonomous driving, telematics, and connectivity solutions are increasingly being integrated into heavy-duty trucks, making them more appealing to fleet operators. These technologies optimize fleet management, improve driver safety, and reduce operating costs, fostering demand for modernized truck models. With fleet operators prioritizing performance and cost efficiency, the adoption of technologically advanced heavy-duty trucks is on the rise globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $311.4 Billion |

| Forecast Value | $458.4 Billion |

| CAGR | 4.2% |

The market is segmented by vehicle class, with Class 8 trucks dominating the sector, accounting for over 80% of the market share in 2024. Known for their robust design and high gross vehicle weight rating (GVWR) exceeding 33,000 pounds, Class 8 trucks are indispensable for industries like logistics, construction, and agriculture. Their ability to transport heavy loads efficiently over long distances has solidified their position in global supply chains. Additionally, the incorporation of cutting-edge features such as fuel-efficient engines and smart systems makes them a preferred choice for fleet operators.

Fuel type segmentation reveals the dominance of diesel-powered trucks, which held over 75% of the market share in 2024. Diesel trucks are renowned for their unmatched power, reliability, and extensive range, making them essential for long-haul transportation and heavy-duty applications. Their continued prominence is supported by a well-established refueling infrastructure, ensuring seamless operations. Despite the gradual shift toward alternative fuels, diesel trucks remain a cornerstone of heavy-duty transportation due to their proven performance and versatility.

Asia Pacific leads the heavy-duty trucks market, contributing 60% of the revenue share in 2023. Rapid industrialization and urbanization across countries like China and India have heightened the demand for efficient transportation solutions. The booming e-commerce sector and expanding logistics networks further amplify the need for heavy-duty trucks. Additionally, government-led infrastructure initiatives and economic development strategies continue to propel market growth in the region. As Asia Pacific strengthens its position as a global economic hub, the heavy-duty trucks market is expected to maintain strong momentum.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component suppliers

- 3.2.3 Manufacturers

- 3.2.4 Technology providers

- 3.2.5 Distributors

- 3.2.6 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Escalating demand for autonomous driving technologies

- 3.8.1.2 Increasing long-haul freight activities bolstering heavy duty truck utilization

- 3.8.1.3 Introduction of advanced emission control systems due to strict regulations

- 3.8.1.4 Expansion of logistic networks and e-commerce globally

- 3.8.1.5 Technological advancements in trucking efficiency and safety features

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced technology integration

- 3.8.2.2 Economic slowdown affecting freight demand

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Class, 2021 - 2034 ($Bn, Unit)

- 5.1 Key trends

- 5.2 Class 7

- 5.2.1 Axle type

- 5.2.1.1 4X2

- 5.2.1.2 6X2

- 5.2.1.3 6X4

- 5.2.1 Axle type

- 5.3 Class 8

- 5.3.1 Axle type

- 5.3.1.1 4X2

- 5.3.1.2 6X2

- 5.3.1.3 6X4

- 5.3.2 Cab type

- 5.3.2.1 Day cab

- 5.3.2.2 Sleeper cab

- 5.3.1 Axle type

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Unit)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Natural gas

- 6.4 Hybrid electric

- 6.5 Gasoline

Chapter 7 Market Estimates & Forecast, By Horsepower, 2021 - 2034 ($Bn, Unit)

- 7.1 Key trends

- 7.2 Below 300HP

- 7.3 300HP-400HP

- 7.4 400HP-500HP

- 7.5 Above 500HP

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Unit)

- 8.1 Key trends

- 8.2 Freight delivery

- 8.3 Utility services

- 8.4 Construction & mining

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Ownership, 2021 - 2034 ($Bn, Unit)

- 9.1 Key trends

- 9.2 Fleet operator

- 9.3 Independent operator

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Unit)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Russia

- 10.3.6 Belgium

- 10.3.7 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 BYD Auto

- 11.2 Daimler Trucks

- 11.3 Dongfeng

- 11.4 Freightliner

- 11.5 Hino Motors

- 11.6 Isuzu Motors

- 11.7 Kenworth

- 11.8 MAN

- 11.9 Navistar

- 11.10 PACCAR Inc

- 11.11 Peterbilt

- 11.12 SCANIA

- 11.13 SINOTRUK

- 11.14 TRATON GROUP

- 11.15 Volvo

重型卡車市場規模、佔有率及成長分析(按類型、重量限制、卡車等級、燃料類型、應用和地區)-2025-2032 年產業預測

重型卡車市場規模、佔有率及成長分析(按類型、重量限制、卡車等級、燃料類型、應用和地區)-2025-2032 年產業預測 2025年全球重型卡車市場報告2025年全球重型卡車市場報告

2025年全球重型卡車市場報告2025年全球重型卡車市場報告 重型車輛租賃市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測全球重型卡車市場

重型車輛租賃市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測全球重型卡車市場 重型車輛市場:按類型、產能、使用者分類 - 2025-2030 年全球預測中型卡車轉向系統市場機會、成長促進因素、產業趨勢分析和 2024 年至 2032 年預測

重型車輛市場:按類型、產能、使用者分類 - 2025-2030 年全球預測中型卡車轉向系統市場機會、成長促進因素、產業趨勢分析和 2024 年至 2032 年預測 全球重型卡車市場規模研究,按重量限制、卡車類別、應用、燃料類型和區域預測 2024-2032全球重型卡車市場 2024-2031全球重卡市場:2033年機會與策略

全球重型卡車市場規模研究,按重量限制、卡車類別、應用、燃料類型和區域預測 2024-2032全球重型卡車市場 2024-2031全球重卡市場:2033年機會與策略