|

市場調查報告書

商品編碼

1666710

管道絕緣市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Pipe Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

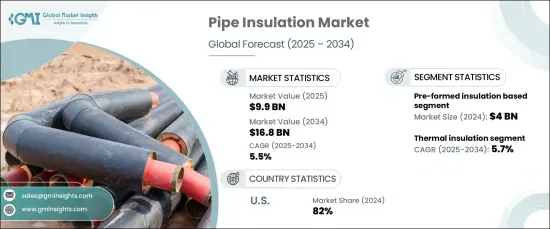

2024 年全球管道絕緣市場價值為 99 億美元,預計 2025 年至 2034 年期間的複合年成長率為 5.5%。絕緣管道可有效減少暖氣和冷氣系統中的能量損失,有助於提高住宅、商業和工業環境的能源效率。

隨著能源成本不斷攀升以及減少碳排放的緊迫性不斷增強,管道保溫作為降低整體能源消耗的實用解決方案越來越受到重視。它有助於維持管道系統的恆定溫度,減少加熱或冷卻所需的能量,從而提供長期成本節約和永續發展效益。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 99億美元 |

| 預測值 | 168億美元 |

| 複合年成長率 | 5.5% |

依產品類型,市場分為預製絕緣材料、硬質板絕緣材料、毯式絕緣材料、捲式絕緣材料、噴塗泡沫絕緣材料等。其中,預製絕緣材料成為領先細分市場,2024 年創造約 40 億美元的收入。預製絕緣材料採用玻璃纖維和礦棉等材料製造,可減少人工成本和安裝時間,使其成為各行業的首選。

依功能,市場分為隔熱、隔音、防火等。 2024 年,隔熱材料將佔據約 40% 的市場佔有率,預計在預測期內的複合年成長率為 5.7%。其主要作用是保持管道內的溫度一致性,從而最大限度地減少能源浪費並最佳化工業流程的性能。此功能對於製造業和能源生產等行業尤其重要,因為效率和降低營運成本是這些行業的首要任務。

從地區來看,美國佔據北美管道絕緣市場的主導地位,佔有約 82% 的佔有率。更嚴格的建築規範和能源效率要求正在推動對先進絕緣解決方案的需求。監管架構旨在減少暖通空調和管道系統的能量損失,並促進高性能絕緣材料的採用。

受人們對節能的日益重視以及對高效、永續基礎設施解決方案的需求的推動,管道絕緣市場有望實現強勁成長。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 增加建築活動

- 不斷成長的產品創新

- 產業陷阱與挑戰

- 市場飽和且競爭激烈

- 永續性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按產品類型,2021-2035 年

- 主要趨勢

- 預成型絕緣材料

- 硬質板保溫

- 毯式隔熱材料

- 捲式絕緣材料

- 噴塗泡棉隔熱材料

- 其他(鬆散填充絕緣等)

第 6 章:市場估計與預測:按材料類型,2021-2035 年

- 主要趨勢

- 玻璃纖維

- 礦棉

- 聚氨酯

- 聚乙烯

- 彈性泡沫

- 橡皮

- 其他(矽酸鈣等)

第 7 章:市場估計與預測:按功能,2021 年至 2035 年

- 主要趨勢

- 隔熱

- 隔音

- 防火

- 其他(結露控制等)

第 8 章:市場估計與預測:依最終用途,2021 年至 2035 年

- 主要趨勢

- 住宅

- 商業的

- 工業的

- 石油和天然氣

- 化學

- 能源與電力

- 海洋

- 其他(醫藥等)

第 9 章:市場估計與預測:按配銷通路,2021-2035 年

- 主要趨勢

- 直接的

- 間接

第 10 章:市場估計與預測:按地區,2021 年至 2035 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第 11 章:公司簡介

- 3M

- Alfa Laval

- Armacell International

- BASF

- Covestro

- Huntsman Corporation

- Insulation Technologies

- Johns Manville

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Rockwool International

- Saint Gobain

- Shenzhen Lanxuan Industrial

- Thermaflex

The Global Pipe Insulation Market was valued at USD 9.9 billion in 2024 and is expected to grow at a CAGR of 5.5% from 2025 to 2034. This growth is largely driven by the increasing focus on energy efficiency, compliance with regulatory standards, and the rising adoption of sustainable construction practices. Insulating pipes effectively minimizes energy loss in heating and cooling systems, contributing to improved energy efficiency in residential, commercial, and industrial settings.

As energy costs continue to climb and the urgency to reduce carbon emissions intensifies, pipe insulation is gaining prominence as a practical solution to lower overall energy consumption. It helps maintain consistent temperatures in piping systems, reducing the energy required for heating or cooling, thus offering long-term cost savings and sustainability benefits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 5.5% |

The market is segmented by product type into pre-formed insulation, rigid board insulation, blanket insulation, roll insulation, spray foam insulation, and others. Among these, pre-formed insulation emerged as a leading segment, generating approximately USD 4 billion in revenue in 2024. This segment is projected to grow steadily, owing to its user-friendly installation process and ability to accommodate various pipe dimensions and configurations. Manufactured using materials such as fiberglass and mineral wool, pre-formed insulation reduces labor costs and installation time, making it a preferred choice across sectors.

By function, the market is categorized into thermal insulation, acoustic insulation, fire protection, and others. Thermal insulation accounted for around 40% of the market share in 2024 and is anticipated to grow at a CAGR of 5.7% over the forecast period. Its primary role is to maintain temperature consistency in pipes, thus minimizing energy waste and optimizing performance in industrial processes. This functionality is particularly important in sectors like manufacturing and energy production, where efficiency and operational cost reduction are priorities.

Regionally, the United States dominates the North America pipe insulation market, holding a substantial share of approximately 82%. Stricter building codes and energy-efficiency mandates are fueling demand for advanced insulation solutions. Regulatory frameworks aim to reduce energy loss in HVAC and plumbing systems, boosting the adoption of high-performance insulation materials.

The pipe insulation market is poised for robust growth, driven by the increasing emphasis on energy conservation and the need for efficient and sustainable infrastructure solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing construction activities

- 3.6.1.2 Growing product innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 5.1 Key trends

- 5.2 Pre-formed insulation

- 5.3 Rigid board insulation

- 5.4 Blanket insulation

- 5.5 Roll insulation

- 5.6 Spray Foam insulation

- 5.7 Others (loose fill insulation, etc.)

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 6.1 Key trends

- 6.2 Fiberglass

- 6.3 Mineral wool

- 6.4 Polyurethane

- 6.5 Polyethylene

- 6.6 Elastomeric foam

- 6.7 Rubber

- 6.8 Others (calcium silicate, etc.)

Chapter 7 Market Estimates & Forecast, By Function, 2021-2035 (USD Million) (Thousand Square Feet)

- 7.1 Key trends

- 7.2 Thermal insulation

- 7.3 Acoustic insulation

- 7.4 Fire protection

- 7.5 Others (condensation control, etc.)

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2035 (USD Million) (Thousand Square Feet)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

- 8.4.1 Oil & gas

- 8.4.2 Chemical

- 8.4.3 Energy & power

- 8.4.4 Marine

- 8.4.5 Others (pharmaceutical, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2035 (USD Million) (Thousand Square Feet)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2035 (USD Million) (Thousand Square Feet)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Alfa Laval

- 11.3 Armacell International

- 11.4 BASF

- 11.5 Covestro

- 11.6 Huntsman Corporation

- 11.7 Insulation Technologies

- 11.8 Johns Manville

- 11.9 Kingspan Group

- 11.10 Knauf Insulation

- 11.11 Owens Corning

- 11.12 Rockwool International

- 11.13 Saint Gobain

- 11.14 Shenzhen Lanxuan Industrial

- 11.15 Thermaflex

管道隔熱材料市場規模、佔有率和成長分析(按材料類型、應用、功能、最終用途、分銷管道和地區)- 2025-2032 年行業預測

管道隔熱材料市場規模、佔有率和成長分析(按材料類型、應用、功能、最終用途、分銷管道和地區)- 2025-2032 年行業預測 2025 年包覆層下腐蝕(CUI) 和噴塗絕緣 (SOI) 塗層全球市場報告

2025 年包覆層下腐蝕(CUI) 和噴塗絕緣 (SOI) 塗層全球市場報告 管道隔熱材料市場:按材料、管道隔熱材料類型、特點和應用分類 - 2025-2030 年全球預測

管道隔熱材料市場:按材料、管道隔熱材料類型、特點和應用分類 - 2025-2030 年全球預測 全球管道隔熱材料市場,2024-2028到 2030 年管道保溫市場預測:按產品類型、最終用戶和地區分類的全球分析

全球管道隔熱材料市場,2024-2028到 2030 年管道保溫市場預測:按產品類型、最終用戶和地區分類的全球分析 包覆層下腐蝕監測市場報告:2030 年趨勢、預測與競爭分析

包覆層下腐蝕監測市場報告:2030 年趨勢、預測與競爭分析 管線隔熱材料市場:各材料,各用途,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測管道隔熱材料市場:按材料、按用途:2023-2032 年全球機會分析與產業預測

管線隔熱材料市場:各材料,各用途,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測管道隔熱材料市場:按材料、按用途:2023-2032 年全球機會分析與產業預測 管道保溫市場、份額、市場規模、趨勢、產業分析報告:按材料、應用、地區、細分市場預測,2023-2032

管道保溫市場、份額、市場規模、趨勢、產業分析報告:按材料、應用、地區、細分市場預測,2023-2032