|

市場調查報告書

商品編碼

1667018

纖維水泥市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Fiber Cement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

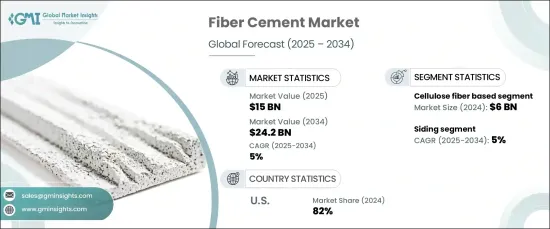

2024 年全球纖維水泥市場價值 150 億美元,將大幅成長,預計 2025 年至 2034 年的複合年成長率為 5%。纖維水泥因其強度高、多功能性和低環境影響而聞名,已在住宅、商業和工業建築等各個領域中廣泛應用。隨著消費者和建築專業人士繼續優先考慮綠色建築實踐,纖維水泥的受歡迎程度飆升。它能夠將成本效益與惡劣天氣條件下的卓越性能相結合,使其成為現代建築專案的首選解決方案。除了耐用之外,纖維水泥還具有維護成本低、持久防風雨等顯著優點,鞏固了其作為環保意識強的建築商的首選地位。

市場按產品類型分類,主要類別包括纖維素纖維基、合成纖維基、礦物纖維基和其他。其中,纖維素纖維基市場預計將佔據領先地位,到 2024 年將產生約 60 億美元的收入。纖維素基纖維水泥由植物纖維製成,由於其環保特性而越來越受到關注,在永續性成為建築業首要任務的時代尤其具有吸引力。隨著建築業尋求減少碳足跡,纖維素纖維的可回收性、可生物分解性和可再生特性繼續促進該領域的成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 150億美元 |

| 預測值 | 242億美元 |

| 複合年成長率 | 5% |

在應用方面,纖維水泥用於牆板、屋頂、裝飾線條、地板等。其中,壁板部分最為突出,佔 2024 年總市場佔有率的約 40%。纖維水泥壁板以其耐用性和抗腐爛、抗白蟻和防潮性能而聞名,是需要經常維護和處理的傳統木材的絕佳替代品。由於纖維水泥壁板使用壽命長、維護需求低,越來越多的建築商和屋主選擇使用纖維水泥壁板,使其成為永續、耐候建築實踐的理想解決方案。

美國纖維水泥市場是最大的市場之一,到 2024 年將佔高達 82% 的佔有率。纖維水泥由沙子、水泥和纖維素纖維等天然材料組成,被視為木材和乙烯基等含碳量高的材料的更環保的替代品。該材料的可回收性、生產過程中對環境的較小影響以及長壽命是綠色建築日益流行的關鍵賣點。預計環保建築的推動將繼續推動纖維水泥的需求,確保其在未來幾年持續成長和廣泛應用。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 增加建築活動

- 不斷成長的產品創新

- 產業陷阱與挑戰

- 市場飽和且競爭激烈

- 永續性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按產品類型,2021-2034 年

- 主要趨勢

- 纖維素纖維基

- 合成纖維基

- 礦物纖維基

- 其他(天然纖維等)

第 6 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 壁板

- 屋頂

- 造型和裝飾

- 地板

- 其他

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 住宅

- 商業的

- 工業的

第 8 章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 直接的

- 間接

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- ArcelorMittal

- Boral Limited

- China National Building Material

- CSR Limited

- Etex Group

- Everest Industries Limited

- Finolex Industries

- Hume Cement

- James Hardie Industries

- Mahaphant Fibre Cement Public

- Nichiha Corporation

- Pioneer Cement Limited

- Saint-Gobain

- Siam Cement Group

- Toray Industries

The Global Fiber Cement Market, valued at USD 15 billion in 2024, is set for substantial growth with an anticipated CAGR of 5% from 2025 to 2034. This positive trajectory is being driven by the increasing demand for sustainable, durable construction materials, especially as industries shift toward eco-friendly alternatives. Fiber cement, recognized for its strength, versatility, and low environmental impact, has garnered widespread adoption across diverse sectors, including residential, commercial, and industrial construction. As consumers and construction professionals continue to prioritize green building practices, fiber cement's popularity has surged. Its ability to combine cost-effectiveness with exceptional performance in harsh weather conditions makes it a go-to solution for modern construction projects. In addition to being durable, fiber cement also offers significant advantages, such as low maintenance and long-lasting protection against the elements, solidifying its position as a prime choice for eco-conscious builders.

The market is divided by product type, with key categories including cellulose fiber-based, synthetic fiber-based, mineral fiber-based, and others. Among these, the cellulose fiber-based segment is expected to lead, generating approximately USD 6 billion in 2024. This segment is projected to grow at a CAGR of 5.2% over the forecast period, benefiting from the rising demand for renewable and biodegradable materials. Made from plant-derived fibers, cellulose-based fiber cement is gaining traction due to its eco-friendly nature, making it particularly appealing in an age when sustainability is becoming a top priority in construction. The cellulose fibers' recyclability, biodegradability, and renewable properties continue to contribute to the segment's growth as the building industry looks to reduce its carbon footprint.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 5% |

When it comes to applications, fiber cement is used in siding, roofing, molding and trim, flooring, and more. Of these, the siding segment is the most prominent, accounting for approximately 40% of the total market share in 2024. With a growth rate expected to match the overall market at a CAGR of 5%, fiber cement siding is becoming the preferred option in areas prone to extreme weather conditions. Renowned for its durability and resistance to rot, termites, and moisture, fiber cement siding provides an excellent alternative to traditional wood, which requires frequent maintenance and treatment. Builders and homeowners are increasingly opting for fiber cement siding due to its long lifespan and low maintenance needs, making it an ideal solution for sustainable, weather-resistant building practices.

The U.S. market for fiber cement is one of the largest, holding an impressive 82% share in 2024. This strong market presence is attributed to the rising demand for green building materials as more projects aim for sustainability certifications. Fiber cement is seen as a more eco-friendly alternative to carbon-heavy materials like wood and vinyl, thanks to its composition of natural materials such as sand, cement, and cellulose fibers. The material's recyclability, lower environmental impact during production, and longevity are key selling points in the growing trend of green construction. The push for eco-conscious construction is expected to keep driving demand for fiber cement, ensuring its continued growth and widespread adoption in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing construction activities

- 3.6.1.2 Growing product innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cellulose fiber based

- 5.3 Synthetic fiber based

- 5.4 Mineral fiber based

- 5.5 Others (natural fiber based, etc.)

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Siding

- 6.3 Roofing

- 6.4 Molding & trim

- 6.5 Flooring

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 ArcelorMittal

- 10.2 Boral Limited

- 10.3 China National Building Material

- 10.4 CSR Limited

- 10.5 Etex Group

- 10.6 Everest Industries Limited

- 10.7 Finolex Industries

- 10.8 Hume Cement

- 10.9 James Hardie Industries

- 10.10 Mahaphant Fibre Cement Public

- 10.11 Nichiha Corporation

- 10.12 Pioneer Cement Limited

- 10.13 Saint-Gobain

- 10.14 Siam Cement Group

- 10.15 Toray Industries

纖維水泥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

纖維水泥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 纖維水泥市場規模、佔有率及成長分析(按材料、應用、最終用戶和地區)-2025-2032 年產業預測

纖維水泥市場規模、佔有率及成長分析(按材料、應用、最終用戶和地區)-2025-2032 年產業預測 2025年纖維水泥全球市場報告

2025年纖維水泥全球市場報告 纖維水泥市場按產品類型、應用和地區分類

纖維水泥市場按產品類型、應用和地區分類 全球纖維水泥市場:原料、固化製程、應用、產業用途和地區分析、規模、趨勢、COVID-19 的影響以及 2030 年預測

全球纖維水泥市場:原料、固化製程、應用、產業用途和地區分析、規模、趨勢、COVID-19 的影響以及 2030 年預測 纖維水泥牆板市場規模、佔有率、按材料類型、安裝方法、產品類型、應用和地區分類的成長分析 - 2025-2032 年產業預測

纖維水泥牆板市場規模、佔有率、按材料類型、安裝方法、產品類型、應用和地區分類的成長分析 - 2025-2032 年產業預測 全球纖維水泥板市場:依產品類型(高密度板、中密度板、低密度板)、原材料、應用、生產流程、最終用戶和地區預測(~2032年)

全球纖維水泥板市場:依產品類型(高密度板、中密度板、低密度板)、原材料、應用、生產流程、最終用戶和地區預測(~2032年) 纖維水泥市場:按材料、應用和最終用戶分類 - 全球預測 2025-2030

纖維水泥市場:按材料、應用和最終用戶分類 - 全球預測 2025-2030 纖維水泥板市場:按類型、厚度、最終用途、應用分類 - 2025-2030 年全球預測

纖維水泥板市場:按類型、厚度、最終用途、應用分類 - 2025-2030 年全球預測 纖維水泥雨幕板市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭細分,2019-2029F

纖維水泥雨幕板市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭細分,2019-2029F