|

市場調查報告書

商品編碼

1750587

備用往復式發電引擎市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Backup Reciprocating Power Generating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

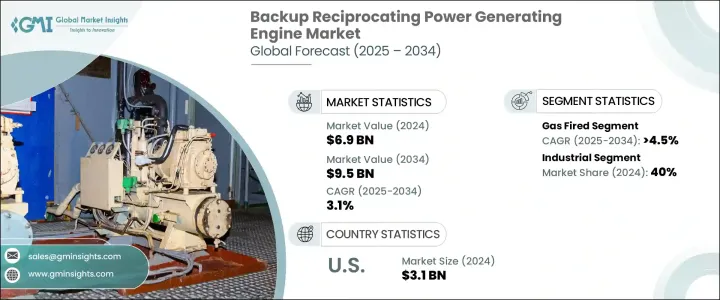

2024年,全球備用往復式發電引擎市值為69億美元,預計到2034年將以3.1%的複合年成長率成長,達到95億美元,這主要得益於對可靠備用電源系統的需求。向分散式能源發電的轉變,尤其是在偏遠地區,正在進一步擴大市場規模。這些引擎對於確保易受電力中斷影響的地區(尤其是偏遠或電力脆弱地區)的穩定供電至關重要。除了提供緊急電源外,備用往復式引擎對於在電力可靠性至關重要的行業中維持營運連續性也變得越來越重要。

發展中經濟體電力供應波動性加劇,災害頻傳地區能源需求不斷成長,預計將推動備用電源系統的普及。此外,物聯網 (IoT) 引擎的整合正在增強系統智慧,促進預測性維護,從而提升關鍵和遠端應用的效能。更嚴格的排放法規以及工業領域對備用電源日益成長的需求也促進了市場擴張。不斷變化的監管環境,包括對進口零件徵收關稅,可能會影響國際貿易,並增加備用發電引擎的生產成本。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 69億美元 |

| 預測值 | 95億美元 |

| 複合年成長率 | 3.1% |

預計到2034年,燃氣備用往復式發電引擎市場將以4.5%的複合年成長率強勁成長,這得益於更嚴格的環境法規和天然氣價格日益親民的推動,使其成為傳統發電方式的可行且永續的替代方案。與傳統的化石燃料發電機相比,燃氣備用往復式發電引擎效率更高、排放更低,具有顯著優勢,因此成為尋求減少碳足跡同時保持可靠電力供應的行業的首選。

此外,預計熱電聯產 (CHP) 系統將實現顯著成長,到 2034 年的複合年成長率將達到 4.5%。對節能解決方案的需求不斷成長,以及企業降低燃料消耗和營運成本的動力是推動這一趨勢的關鍵因素。熱電聯產系統尤其受到重視,因為它能夠同時發電並收集餘熱用於供暖,從而提高能源效率並降低整體營運成本。

2024年,美國備用往復式發電機市場規模達31億美元,反映出對可靠電力日益成長的需求。這一成長主要歸因於美國老化電網基礎設施的現代化改造,以及對備用系統的需求,以確保在停電期間持續供電。此外,各行各業對節能技術的日益普及,加上商業和工業活動的擴張,預計將推動市場進一步成長。

全球備用往復式發電引擎市場的主要參與者正專注於產品創新和市場擴張,以鞏固其市場地位。勞斯萊斯、曼恩能源解決方案和瓦錫蘭等公司正加大研發投入,以提高引擎性能和燃油效率。他們還利用策略合作夥伴關係和收購來進入新的區域市場並增強產品供應。此外,各公司正致力於永續發展,開發符合嚴格排放標準的引擎。這些策略正被用於滿足各行各業對可靠、環保的動力解決方案日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:依燃料類型,2021 - 2034

- 主要趨勢

- 瓦斯

- 柴油引擎

- 雙燃料

- 其他

第6章:市場規模及預測:依額定功率,2021 - 2034

- 主要趨勢

- 0.5 兆瓦 - 1 兆瓦

- > 1 兆瓦 - 2 兆瓦

- > 2 兆瓦 - 3.5 兆瓦

- > 3.5 兆瓦 - 5 兆瓦

- > 5 兆瓦 - 7.5 兆瓦

- > 7.5 兆瓦

第7章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 工業的

- 熱電聯產

- 能源與公用事業

- 垃圾掩埋場和沼氣

- 其他

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 俄羅斯

- 義大利

- 西班牙

- 荷蘭

- 丹麥

- 挪威

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 泰國

- 新加坡

- 印尼

- 馬來西亞

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 卡達

- 阿曼

- 科威特

- 伊朗

- 埃及

- 土耳其

- 約旦

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 秘魯

第9章:公司簡介

- AB Volvo Penta

- Atlas Copco

- Caterpillar

- Clarke Energy

- GE Vernova

- HIMOINSA

- Kirloskar

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Motorenfabrik Hatz

- Rehlko

- Rolls-Royce

- Scania

- Wartsilä

- Yamaha Motor

- Yuchai International

The Global Backup Reciprocating Power Generating Engine Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 3.1% to reach USD 9.5 billion by 2034, driven by the demand for reliable backup power systems. The shift toward decentralized energy generation, particularly in remote areas, is further expanding the market. These engines are vital for ensuring a consistent power supply in areas prone to electrical disruptions, especially in isolated or vulnerable locations. In addition to providing emergency power, backup reciprocating engines are becoming increasingly important for maintaining operational continuity in industries where power reliability is critical.

The growing volatility of electricity supply in developing economies and the increasing need for energy in disaster-prone regions are expected to fuel the adoption of backup power systems. Furthermore, the integration of Internet of Things (IoT)-enabled engines is enhancing system intelligence and facilitating predictive maintenance, thus improving the performance of critical and remote applications. Stricter emission regulations and the rising demand for standby power in industrial sectors also contribute to market expansion. The evolving regulatory landscape, including tariffs on imported parts, may impact international trade and increase production costs for backup power-generating engines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $9.5 Billion |

| CAGR | 3.1% |

The gas-fired backup reciprocating power generating engine market is projected to grow at a robust CAGR of 4.5% through 2034, driven by stricter environmental regulations and the increasing affordability of natural gas, making it a viable and sustainable alternative to traditional power generation methods. These engines offer a compelling advantage due to their higher efficiency and lower emissions compared to conventional fossil-fuel-powered generators, making them a preferred choice for industries looking to reduce their carbon footprint while maintaining a reliable power supply.

In addition to this, Combined Heat and Power (CHP) systems are expected to see notable growth, with an anticipated CAGR of 4.5% through 2034. The rising demand for energy-efficient solutions and the push for businesses to lower their fuel consumption and operating costs are key factors contributing to this trend. CHP systems are particularly valued for their ability to simultaneously generate electricity and capture waste heat for use in heating, thereby improving energy efficiency and reducing overall operational costs.

United States Backup Reciprocating Power Generating Engine Market was valued at USD 3.1 billion in 2024, reflecting the increasing demand for dependable electricity. This surge is largely attributed to the modernization of the nation's aging grid infrastructure and the need for backup systems to ensure continuous power during outages. Additionally, the growing adoption of energy-efficient technologies across various sectors, coupled with the expansion of commercial and industrial activities, is expected to drive further growth in the market.

Key players in the Global Backup Reciprocating Power Generating Engine Market are focusing on product innovation and market expansion to strengthen their positions. Companies like Rolls-Royce, MAN Energy Solutions, and Wartsila are increasingly investing in research and development to improve engine performance and fuel efficiency. Strategic partnerships and acquisitions are also being utilized to enter new regional markets and enhance product offerings. Additionally, firms are focusing on sustainability by developing engines that comply with stringent emission standards. These strategies are being adopted to meet the growing demand for reliable, environmentally friendly power solutions across various industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel Type, 2021 - 2034 (USD Million, MW & Units)

- 5.1 Key trends

- 5.2 Gas-fired

- 5.3 Diesel-fired

- 5.4 Dual fuel

- 5.5 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 - 2034 (USD Million, MW & Units)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, MW & Units)

- 7.1 Key trends

- 7.2 Industrial

- 7.3 CHP

- 7.4 Energy & utility

- 7.5 Landfill & biogas

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, MW & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.3.9 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Iran

- 8.5.7 Egypt

- 8.5.8 Turkey

- 8.5.9 Jordan

- 8.5.10 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 Atlas Copco

- 9.3 Caterpillar

- 9.4 Clarke Energy

- 9.5 GE Vernova

- 9.6 HIMOINSA

- 9.7 Kirloskar

- 9.8 MAN Energy Solutions

- 9.9 Mitsubishi Heavy Industries

- 9.10 Motorenfabrik Hatz

- 9.11 Rehlko

- 9.12 Rolls-Royce

- 9.13 Scania

- 9.14 Wartsilä

- 9.15 Yamaha Motor

- 9.16 Yuchai International

柴油引擎:全球市場佔有率和排名、總銷售量和需求預測(2025-2031年)

柴油引擎:全球市場佔有率和排名、總銷售量和需求預測(2025-2031年) 柴油引擎市場按應用、功率輸出、技術、冷卻方式、汽缸數和排放氣體標準分類-2025-2032年全球預測

柴油引擎市場按應用、功率輸出、技術、冷卻方式、汽缸數和排放氣體標準分類-2025-2032年全球預測 2025年全球柴油引擎市場報告2025年全球往復式發電引擎市場報告2025年原動機往復式發電機全球市場報告

2025年全球柴油引擎市場報告2025年全球往復式發電引擎市場報告2025年原動機往復式發電機全球市場報告 往復式發電引擎市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

往復式發電引擎市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球柴油引擎市場:2031 年預測

全球柴油引擎市場:2031 年預測 柴油引擎:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

柴油引擎:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2030 年柴油引擎市場預測:按燃料類型、引擎類型、零件、應用和地區進行的全球分析全球備用往復式發電機引擎市場

2030 年柴油引擎市場預測:按燃料類型、引擎類型、零件、應用和地區進行的全球分析全球備用往復式發電機引擎市場