|

市場調查報告書

商品編碼

1667076

瓦楞設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Corrugated Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

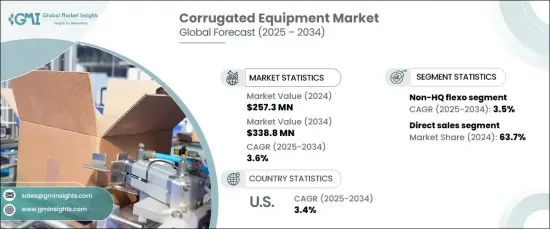

2024 年全球瓦楞設備市場規模達到 2.573 億美元,預計 2025 年至 2034 年期間的複合年成長率為 3.6%。電子商務的激增進一步增加了對可靠和保護性包裝的需求,因為企業的目標是確保貨物安全地直接送達客戶。

瓦楞紙包裝因其重量輕、耐用、可回收等特點而成為首選。製藥、食品飲料和電子等行業透過依賴瓦楞紙解決方案來確保產品安全、品牌推廣和符合永續性標準,為市場成長做出了巨大貢獻。此外,自動化和數位印刷等製造技術的進步正在提高瓦楞設備的效率和質量,鞏固其在包裝領域的地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.573億美元 |

| 預測值 | 3.388 億美元 |

| 複合年成長率 | 3.6% |

市場依靠兩種主要分銷管道蓬勃發展:直接銷售和間接銷售。直銷佔了63.7%的市場佔有率,即製造商直接與客戶接觸,提供客製化的解決方案和技術支援。對於需要與最終用戶密切合作以滿足特定要求的大型複雜系統來說,此管道至關重要。相比之下,間接銷售利用經銷商和代理商滲透更廣泛的市場並利用本地化的專業知識。這種方法對於製造商缺乏直接業務的地區尤其有利,可確保更廣泛地覆蓋和接觸不同的客戶群。

市場分為非高品質柔印設備和高品質柔印設備,凸顯了其多樣化的應用。非 HQ 柔印設備的價值在 2024 年為 6,090 萬美元,可滿足基本包裝應用的高速和經濟高效的生產需求。該細分市場優先考慮營運效率而不是印刷質量,這使其成為專注於功能性包裝的行業的理想選擇。另一方面,HQ 柔印設備將於 2024 年創造 1.22 億美元的收入,提供出色的印刷解析度和色彩準確度,滿足高階包裝需求。受各行各業強調美觀性和品牌效應以增強客戶參與度的推動,對高品質包裝解決方案的需求持續上升。

2024 年美國瓦楞設備市場價值為 4,770 萬美元,預測期內將以 3.4% 的複合年成長率穩定成長。工業擴張、技術進步和基礎設施發展是這一成長的主要驅動力。美國製造商擴大採用自動化、數位化和高速生產技術來提高營運效率並降低成本。此外,食品、電子和醫藥等行業對客製化和保護性包裝解決方案的需求日益成長,支撐了該地區對瓦楞設備的強勁需求。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算。

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素。

- 利潤率分析。

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析。

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 對永續包裝解決方案的需求不斷增加

- 電子商務行業呈指數級成長

- 產業陷阱與挑戰

- 瓦楞設備相關成本高

- 與設計和開發相關的複雜性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按設備,2021 年至 2034 年

- 主要趨勢

- 非 HQ 柔版印刷

- 平板模切機

- 旋轉模切機

- 折疊黏合

- 高品質柔版印刷

- 平板模切機

- 旋轉模切機

- 折疊黏合

- 單張紙膠印裱貼機

- 捲筒紙對捲筒紙平版裱貼機

- 排隊

- 離線

- 捲筒紙平版裱貼機

- 排隊

- 離線

第 6 章:市場估計與預測:按最終用途產業,2021-2034 年

- 主要趨勢

- 食品和飲料

- 電氣和電子產品

- 家庭和個人護理

- 紡織品

- 紙張和紙漿

- 藥品

第 7 章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 直接銷售

- 間接銷售

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

8.2.1 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第9章:公司簡介

- Automatan

- Barry-Wehmiller

- BHS Corrugated

- Bobst Group

- Edale UK

- EMBA

- Heidelberger Druckmaschinen

- Lamina System

- Manroland

- Mark Andy

- Mitsubishi Heavy Industries Machinery Systems

- MPS Systems

- OMET

- Oppliger SRL

- Rotatek

- Simon Corrugated Machinery

- Star Flex International

- Sun Automation

- Walco

- Wolverine Flexographic

The Global Corrugated Equipment Market reached USD 257.3 million in 2024 and is projected to grow at a CAGR of 3.6% between 2025 and 2034. This market expansion is fueled by the increasing adoption of sustainable packaging solutions, driven by heightened environmental awareness and regulatory support for eco-friendly practices. The surge in e-commerce further amplifies the demand for reliable and protective packaging, as businesses aim to ensure the safe delivery of goods directly to customers.

Corrugated packaging stands out as a preferred choice due to its lightweight, durability, and recyclability. Industries such as pharmaceuticals, food and beverages, and electronics are significantly contributing to market growth by relying on corrugated solutions for product safety, branding, and compliance with sustainability standards. Furthermore, advancements in manufacturing technologies, including automation and digital printing, are enhancing the efficiency and quality of corrugated equipment, solidifying its position in the packaging sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $257.3 Million |

| Forecast Value | $338.8 Million |

| CAGR | 3.6% |

The market thrives on two primary distribution channels: direct sales and indirect sales. Direct sales, accounting for 63.7% of the market, involve manufacturers directly engaging with customers to provide tailored solutions and technical support. This channel is essential for large and complex systems that demand close collaboration with end-users to meet specific requirements. In contrast, indirect sales leverage distributors and agents to penetrate wider markets and utilize localized expertise. This approach is particularly advantageous in regions where manufacturers lack a direct presence, ensuring broader reach and accessibility to diverse customer bases.

The segmentation of the market into Non-HQ flexo and HQ flexo equipment highlights its diverse applications. Non-HQ flexo equipment, valued at USD 60.9 million in 2024, addresses the need for high-speed and cost-effective production for basic packaging applications. This segment prioritizes operational efficiency over print quality, making it ideal for industries focused on functional packaging. On the other hand, HQ flexo equipment, generating USD 122.0 million in 2024, offers exceptional print resolution and color accuracy, catering to premium packaging needs. The demand for high-quality packaging solutions continues to rise, driven by industries emphasizing aesthetics and branding to enhance customer engagement.

The U.S. corrugated equipment market, valued at USD 47.7 million in 2024, is poised for steady growth at a CAGR of 3.4% over the forecast period. Industrial expansion, technological advancements, and infrastructure development are key drivers of this growth. U.S. manufacturers are increasingly adopting automation, digitalization, and high-speed production technologies to boost operational efficiency and minimize costs. Additionally, the growing need for customized and protective packaging solutions across sectors such as food, electronics, and pharmaceuticals underpins the strong demand for corrugated equipment in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis.

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for sustainable packaging solutions

- 3.6.1.2 Exponential growth of e-commerce industry

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost associated with the corrugated equipment

- 3.6.2.2 Complexities associated with the design and development

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Equipment, 2021-2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Non-HQ Flexo

- 5.2.1 Flatbed die cutter

- 5.2.2 Rotary die cutter

- 5.2.3 Folding gluing

- 5.3 HQ Flexo

- 5.3.1 Flatbed die cutter

- 5.3.2 Rotary die cutter

- 5.3.3 Folding gluing

- 5.4 Sheet-to-sheet litho-laminators

- 5.5 Web-to-web litho-laminators

- 5.5.1 Inline

- 5.5.2 Offline

- 5.6 Web-to- sheet litho-laminators

- 5.6.1 Inline

- 5.6.2 Offline

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Food & beverages

- 6.3 Electrical & electronics

- 6.4 Home & personal care

- 6.5 Textile

- 6.6 Paper & pulp

- 6.7 Pharmaceuticals

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (XXX Units)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Indirect sales

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 United Kingdom

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Automatan

- 9.2 Barry-Wehmiller

- 9.3 BHS Corrugated

- 9.4 Bobst Group

- 9.5 Edale UK

- 9.6 EMBA

- 9.7 Heidelberger Druckmaschinen

- 9.8 Lamina System

- 9.9 Manroland

- 9.10 Mark Andy

- 9.11 Mitsubishi Heavy Industries Machinery Systems

- 9.12 MPS Systems

- 9.13 OMET

- 9.14 Oppliger SRL

- 9.15 Rotatek

- 9.16 Simon Corrugated Machinery

- 9.17 Star Flex International

- 9.18 Sun Automation

- 9.19 Walco

- 9.20 Wolverine Flexographic

木工機械市場:依產品類型、應用、地區、機會、預測,2018-2032年

木工機械市場:依產品類型、應用、地區、機會、預測,2018-2032年 鋸木機械市場:2025-2029 年全球市場

鋸木機械市場:2025-2029 年全球市場 2025年全球衛生紙加工機市場報告2025年木工機械全球市場報告木工機器的全球市場 (~2032年):機器類型·動力來源·用途·自動化層級·尺寸·各地區2025 年紙漿和造紙機械全球市場報告

2025年全球衛生紙加工機市場報告2025年木工機械全球市場報告木工機器的全球市場 (~2032年):機器類型·動力來源·用途·自動化層級·尺寸·各地區2025 年紙漿和造紙機械全球市場報告 製漿造紙機械市場:按機器類型、應用、最終用戶產業、技術、機器容量 - 2025-2030 年全球預測

製漿造紙機械市場:按機器類型、應用、最終用戶產業、技術、機器容量 - 2025-2030 年全球預測 衛生紙加工機市場,按類型、操作類型、國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測

衛生紙加工機市場,按類型、操作類型、國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測 紙張分切機市場:全球產業分析,規模,佔有率,成長,趨勢,預測,2024年~2031年

紙張分切機市場:全球產業分析,規模,佔有率,成長,趨勢,預測,2024年~2031年 鋸木廠機械市場規模和預測(2021 - 2031)、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型(固定鋸木廠和攜帶式鋸木廠)、應用(木工工業和林業)和地理位置

鋸木廠機械市場規模和預測(2021 - 2031)、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型(固定鋸木廠和攜帶式鋸木廠)、應用(木工工業和林業)和地理位置