|

市場調查報告書

商品編碼

1667113

循環聚合物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Circular Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

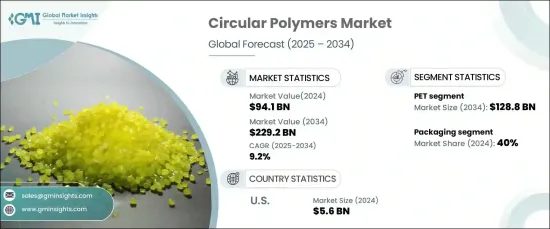

2024 年全球循環聚合物市場規模將達到 941 億美元,預計 2025 年至 2034 年期間將以 9.2% 的強勁複合年成長率成長。這種向永續資源管理的轉變涉及製造、包裝和消費品等各個領域,從而推動了對循環聚合物的需求。

消費者對環境永續性的意識不斷增強,極大地影響了購買決策,推動了對循環聚合物包裝產品的需求。消費者越來越意識到塑膠垃圾的有害影響,並積極尋求更環保的替代品。因此,製造商正在轉向循環聚合物作為包裝解決方案,以滿足對耐用和永續產品日益成長的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 941億美元 |

| 預測值 | 2292億美元 |

| 複合年成長率 | 9.2% |

市場主要按聚合物類型細分,包括 PET、聚乙烯、聚丙烯、PVC 等。其中,PET 領域在 2024聚對苯二甲酸乙二酯創收 504 億美元,預計到 2034 年將達到 1,288 億美元。 PET 廣泛用於包裝,尤其是瓶子和容器,其回收率高,確保了穩定的回收供應。它能夠透過多次回收循環保留其特性,這使得它成為閉迴路系統的理想選擇。此外,化學解聚等回收技術的進步正在提高 PET 的品質並增強其再利用潛力。

包裝是循環聚合物市場的主要應用領域,到 2024 年將佔據 40% 的佔有率。循環聚合物在包裝中的應用越來越多,因為它們有助於減少對環境的影響,同時保持性能和效率。食品、飲料、消費品和醫藥等產業都明顯轉向永續包裝。品牌擴大尋求環保包裝解決方案來滿足消費者需求並滿足監管標準。循環聚合物,尤其是再生 PET(r-PET),為包裝提供了耐用、可回收且高品質的替代品。

2024 年,美國循環聚合物市場價值為 56 億美元。消費者對環保產品(尤其是包裝)的偏好日益成長,促使製造商採用再生聚合物。對化學回收等先進回收技術的投資正在提高回收材料的質量,擴大其在各個行業的應用。企業永續發展計畫和領導企業對碳中和的承諾也推動了循環聚合物的廣泛應用。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 各行各業越來越意識到使用再生材料來減少碳足跡

- 包裝產業擴大採用可回收材料,推動市場發展

- 促進再生塑膠發展的有利舉措

- 產業陷阱與挑戰

- 傾向於使用原生塑膠而非再生聚合物

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場規模及預測:按聚合物,2021-2034 年

- 主要趨勢

- 寵物

- 聚乙烯

- 聚丙烯

- PVC

- 其他

第 6 章:市場規模與預測:按應用,2021-2034 年

- 主要趨勢

- 包裝

- 建築與施工

- 汽車

- 電氣和電子產品

- 農業

- 其他

第 7 章:市場規模與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Advanced Circular Polymers

- ALBA Group

- Banyan

- BASF

- Borealis

- Circular Polymers

- Dow

- ExxonMobil

- KW Plastics

- PlastiCycle

- Quality Circular Polymers

- SABIC

- The Shakti Plastic Industries

- Total Energies

- Veolia

The Global Circular Polymers Market reached USD 94.1 billion in 2024 and is projected to grow at a robust CAGR of 9.2% between 2025 and 2034. As environmental concerns intensify and the availability of natural resources dwindles, industries are increasingly adopting practices that focus on waste reduction and maximizing resource efficiency. This shift toward sustainable resource management spans various sectors, including manufacturing, packaging, and consumer goods, boosting the demand for circular polymers.

Rising awareness among consumers about environmental sustainability has significantly influenced purchasing decisions, driving demand for products packaged in circular polymers. Consumers are becoming more conscious of the detrimental impact of plastic waste and are actively seeking more environmentally friendly alternatives. As a result, manufacturers are turning to circular polymers for packaging solutions to meet the growing demand for durable and sustainable products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $94.1 Billion |

| Forecast Value | $229.2 Billion |

| CAGR | 9.2% |

The market is primarily segmented by polymer type, including PET, polyethylene, polypropylene, PVC, and others. Among these, the PET segment generated USD 50.4 billion in 2024 and is projected to reach USD 128.8 billion by 2034. PET (Polyethylene Terephthalate) is favored in the circular polymer market due to its exceptional recyclability and versatility. Widely used in packaging, especially for bottles and containers, PET benefits from high recovery rates, ensuring a consistent supply for recycling. Its ability to retain its properties through multiple recycling cycles makes it ideal for closed-loop systems. Furthermore, advances in recycling technologies, like chemical depolymerization, are improving PET's quality and enhancing its reuse potential.

Packaging is the dominant application segment in the circular polymers market, accounting for a 40% share in 2024. This growth is driven by the need to combat plastic waste and enhance sustainability efforts across industries. Circular polymers are increasingly used in packaging because they help reduce environmental impact while maintaining performance and efficiency. The shift toward sustainable packaging is noticeable across sectors such as food, beverage, consumer goods, and pharmaceuticals. Brands are increasingly seeking eco-friendly packaging solutions to cater to consumer demand and meet regulatory standards. Circular polymers, particularly recycled PET (r-PET), provide a durable, recyclable, and high-quality alternative for packaging.

U.S. circular polymers market was valued at USD 5.6 billion in 2024. The growth in this market is largely driven by regulations promoting sustainable waste management and a reduction in the use of virgin plastics. The rising consumer preference for eco-friendly products, particularly in packaging, is encouraging manufacturers to adopt recycled polymers. Investment in advanced recycling technologies, such as chemical recycling, is improving the quality of recycled materials, broadening their applications across various industries. Corporate sustainability initiatives and commitments to carbon neutrality by leading companies are also driving the widespread adoption of circular polymers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising awareness among various industries to use recycled materials to reduce their carbon footprints

- 3.6.1.2 Increasing adoption of recyclable materials in the packaging industry is driving the market

- 3.6.1.3 Favorable initiatives to promote recycled plastics

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Inclination toward the use of virgin plastics over recycled polymers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Polymer, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 PET

- 5.3 Polyethylene

- 5.4 Polypropylene

- 5.5 PVC

- 5.6 Others

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Packaging

- 6.3 Building & construction

- 6.4 Automotive

- 6.5 Electrical & electronics

- 6.6 Agriculture

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Advanced Circular Polymers

- 8.2 ALBA Group

- 8.3 Banyan

- 8.4 BASF

- 8.5 Borealis

- 8.6 Circular Polymers

- 8.7 Dow

- 8.8 ExxonMobil

- 8.9 KW Plastics

- 8.10 PlastiCycle

- 8.11 Quality Circular Polymers

- 8.12 SABIC

- 8.13 The Shakti Plastic Industries

- 8.14 Total Energies

- 8.15 Veolia

矽烷基丙烯酸酯聚合物市場規模、佔有率及成長分析(依產品類型、最終用途產業、通路及地區)-2025-2032 年產業預測

矽烷基丙烯酸酯聚合物市場規模、佔有率及成長分析(依產品類型、最終用途產業、通路及地區)-2025-2032 年產業預測 生物基砌塊和聚合物:全球產能、產量和趨勢(2024-2029)

生物基砌塊和聚合物:全球產能、產量和趨勢(2024-2029) 有機矽聚合物市場報告:趨勢、預測和競爭分析(至 2031 年)

有機矽聚合物市場報告:趨勢、預測和競爭分析(至 2031 年) 2025 年至 2033 年特種聚合物市場報告(按產品類型、最終用途產業和地區)

2025 年至 2033 年特種聚合物市場報告(按產品類型、最終用途產業和地區) 全球丙烯酸粉末市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年全球聚合物膠體市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球丙烯酸粉末市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年全球聚合物膠體市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 2025 年合成聚合物全球市場報告2DPA-1 市場規模、佔有率和成長分析(按應用、最終用途和地區)- 產業預測 2025-2032澱粉聚合物市場 - 全球產業規模、佔有率、趨勢、機會和預測,按來源、應用、地區和競爭細分,2020-2030 年澱粉聚合物市場報告:趨勢、預測和競爭分析(至 2031 年)

2025 年合成聚合物全球市場報告2DPA-1 市場規模、佔有率和成長分析(按應用、最終用途和地區)- 產業預測 2025-2032澱粉聚合物市場 - 全球產業規模、佔有率、趨勢、機會和預測,按來源、應用、地區和競爭細分,2020-2030 年澱粉聚合物市場報告:趨勢、預測和競爭分析(至 2031 年)