|

市場調查報告書

商品編碼

1667116

電動舷外機市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測Electric Outboard Engines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

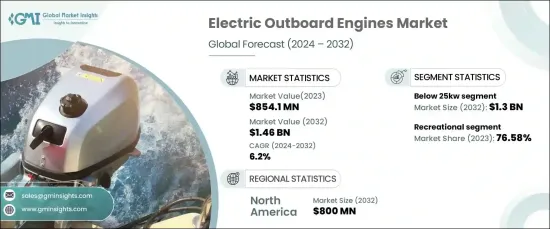

2024 年全球電動舷外機市場規模達到 8.541 億美元,預計 2025 年至 2034 年的複合年成長率為 6.2%。與傳統柴油和汽油引擎相比,這些引擎由於排放量更低、噪音水平更低、環境效益更高,在船舶工業中越來越受歡迎。

推動市場成長的主要驅動力之一是蓬勃發展的海洋旅遊業。隨著旅客尋求透過巡航和休閒划船獲得獨特和永續的體驗,對電動舷外機的需求激增。海上運輸向環保解決方案的轉變使得電動引擎成為整個產業的首選。此外,由於用戶優先考慮清潔、安靜和高效的推進系統,水上運動和休閒划船活動的日益普及進一步加速了其採用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2023 |

| 預測年份 | 2024-2032 |

| 起始值 | 8.541 億美元 |

| 預測值 | 14.6億美元 |

| 複合年成長率 | 6.2% |

根據功率輸出,市場分為 25kW 以下、25-50kW 和 50-150kW。 25kW 以下市場在 2024 年佔據主導地位,貢獻了可觀的收入,預計將穩步成長,到 2034 年達到 13 億美元。低功率電動引擎為小型船隻提供了實用的替代方案,同時符合嚴格的環境法規。

根據應用,電動舷外機市場分為休閒、商業和軍事領域。休閒娛樂領域在 2024 年佔據最大的市場佔有率,預計 2025-2034 年期間的複合年成長率為 6.1%。日益增強的環保意識和對污染的擔憂促使船主和愛好者轉向電動替代品。技術進步也提高了電動引擎的耐用性和性能,增強了其對休閒划船活動的吸引力。這些引擎不僅最大限度地減少噪音污染,而且符合不斷發展的永續發展目標。

2024 年北美引領電動舷外機市場,貢獻 4.99 億美元的收入。該地區預計將保持主導地位,到 2034 年將達到 8 億美元。領先製造商對研發的投資進一步加強了市場,創新專注於提高性能和效率。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析。

- 中斷

- 未來展望

- 製造商

- 經銷商

- 零售商

- 產業衝擊力

- 成長動力

- 增加休閒划船活動

- 遊艇產銷不斷攀升

- 不斷發展的海洋旅遊休閒產業

- 產業陷阱與挑戰

- 初期投資成本高

- 成長動力

- 成長潛力分析

- 消費者購買行為分析

- 技術概覽

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按功率

- 主要趨勢

- 25千瓦以下

- 25 – 50 千瓦

- 50 – 150 千瓦

第6章:市場估計與預測:按速度(英哩/小時)

- 主要趨勢

- 低於 5 英里/小時

- 5-10英里/小時

- 10-15英里/小時

- 時速 15 英里以上

第7章:市場估計與預測:按應用

- 主要趨勢

- 商業的

- 休閒娛樂

- 軍隊

第 8 章:市場估計與預測:按配銷通路

- 主要趨勢

- 直銷

- 間接銷售

第9章:市場估計與預測:按地區

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東及非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- MEA 其他地區

第10章:公司簡介

- Aqua watt

- Combi Outboards

- Elco Motor Yachts

- EPROPULSION

- E-TECH

- Evoy

- Golden Motors

- Hitachi, Ltd.

- KONE

- MINN KOTA

- Mitsubishi Electric Corporation

- Parsun Power

- Pure Watercraft

- Schindler

- Torqeedo GmbH

The Global Electric Outboard Engines Market reached USD 854.1 million in 2024 and is projected to grow at a CAGR of 6.2% from 2025 to 2034. Electric outboard engines installed in boats rely on electric motors to provide propulsion. These engines are gaining traction in the marine industry due to their lower emissions, reduced noise levels, and environmental benefits compared to conventional diesel and gasoline engines.

One of the key drivers fueling market growth is the booming marine tourism industry. As travelers seek unique and sustainable experiences through cruising and recreational boating, the demand for electric outboard engines has surged. The shift toward eco-friendly solutions in marine transportation has made electric engines a preferred choice across the sector. Additionally, the rising popularity of water sports and recreational boating activities has further accelerated adoption as users prioritize clean, quiet, and efficient propulsion systems.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $854.1 Million |

| Forecast Value | $1.46 Billion |

| CAGR | 6.2% |

Based on power output, the market is segmented into below 25kW, 25-50kW, and 50-150kW. The below 25kW segment dominated in 2024, contributing significant revenue, and is expected to grow steadily, reaching USD 1.3 billion by 2034. The segment growth is driven by its affordability, eco-friendly performance, and suitability for budget-conscious consumers. Low-powered electric engines offer a practical alternative for smaller boats while complying with stringent environmental regulations.

In terms of application, the electric outboard engines market is categorized into recreational, commercial, and military segments. The recreational segment held the largest market share in 2024 and is expected to grow at a CAGR of 6.1% during 2025-2034. Increasing environmental awareness and concerns about pollution have encouraged boat owners and enthusiasts to shift toward electric alternatives. Technological advancements have also improved the durability and performance of electric engines, enhancing their appeal for recreational boating activities. These engines not only minimize noise pollution but also align with evolving sustainability goals.

North America led the electric outboard engines market in 2024, contributing USD 499 million in revenue. The region is expected to maintain its dominance, reaching USD 800 million by 2034. North America's robust recreational boating industry, supported by favorable environmental policies, is a key driver of this growth. The presence of leading manufacturers investing in research and development has further strengthened the market, with innovations focused on enhancing performance and efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing recreation boating activities

- 3.2.1.2 Rising production and sale of yatch

- 3.2.1.3 Growing marine tourism and leisure industry

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost of investments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Consumer buying behavior analysis

- 3.5 Technological overview

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Company market share analysis

- 4.2 Competitive positioning matrix

- 4.3 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Power (USD Million)

- 5.1 Key trends

- 5.2 Below 25 kW

- 5.3 25 – 50 kW

- 5.4 50 – 150 kW

Chapter 6 Market Estimates & Forecast, By Speed (mph) (USD Million)

- 6.1 Key trends

- 6.2 Below 5 mph

- 6.3 5-10 mph

- 6.4 10-15 mph

- 6.5 Above 15 mph

Chapter 7 Market Estimates & Forecast, By Application (USD Million)

- 7.1 Key trends

- 7.2 Commercial

- 7.3 Recreational

- 7.4 Military

Chapter 8 Market Estimates & Forecast, By Distribution Channel (USD Million)

- 8.1 Key trends

- 8.2 Direct sale

- 8.3 Indirect sale

Chapter 9 Market Estimates & Forecast, By Region (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Aqua watt

- 10.2 Combi Outboards

- 10.3 Elco Motor Yachts

- 10.4 EPROPULSION

- 10.5 E-TECH

- 10.6 Evoy

- 10.7 Golden Motors

- 10.8 Hitachi, Ltd.

- 10.9 KONE

- 10.10 MINN KOTA

- 10.11 Mitsubishi Electric Corporation

- 10.12 Parsun Power

- 10.13 Pure Watercraft

- 10.14 Schindler

- 10.15 Torqeedo GmbH