|

市場調查報告書

商品編碼

1667139

飛機健康監測系統市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Aircraft Health Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

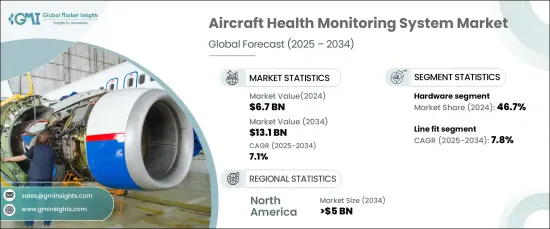

2024 年全球飛機健康監測系統市場價值為 67 億美元,預計 2025 年至 2034 年的複合年成長率為 7.1%。先進的技術可以實現即時資料收集和分析,使操作員能夠識別潛在故障並採取預防措施。這一演變是由物聯網 (IoT) 設備和巨量資料分析的整合所推動的,它們提供了全面的監控和預測見解。航空公司和機隊營運商擴大採用這些系統來確保安全、最佳化維護計劃並降低成本。

安裝在飛機上的物聯網感測器可以捕獲關鍵運行資料,例如引擎性能、溫度、振動和燃油效率。這些資訊透過基於雲端的分析平台進行處理,以識別異常、預測維護需求並提高整體系統可靠性。飛機系統和地面操作之間的無縫通訊促進了綜合航空網路的發展,改善了決策過程和營運效率。隨著這些技術變得越來越先進,其在商業、私人和軍用航空領域的應用預計將大幅成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 67億美元 |

| 預測值 | 131億美元 |

| 複合年成長率 | 7.1% |

市場按解決方案細分為硬體、軟體和服務,其中硬體部分佔據最大佔有率,到 2024 年將達到 46.7%。這些設備可以精確測量溫度、壓力和振動等參數,可提前發現潛在問題。硬體技術的進步使得組件變得更小、更輕、更耐用,從而提高了效率和安裝的簡易性。與物聯網系統的整合可實現無縫資料共享和基於雲端的分析,進一步提高功能。營運商優先考慮可靠、經濟高效且易於維護的硬體解決方案。

根據適配情況,市場分為線路適配和改造適配,其中線路適配部分預計在預測期內以 7.8% 的複合年成長率成長。線路適配涉及在飛機製造過程中安裝健康監測系統,確保與特定型號的兼容性,並增強系統整合。這種方法降低了實施成本並簡化了維護,使其成為營運商和製造商的首選。隨著對新飛機的需求不斷成長,線裝部分將經歷顯著的成長。

在美國航太業蓬勃發展的推動下,北美市場規模預計到 2034 年將超過 50 億美元。該地區受益於主要航空公司、原始設備製造商的存在以及機器學習和物聯網技術的進步,從而促進了飛機健康監測系統的採用。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 航空業對預測性維護的需求不斷增加

- 物聯網與巨量資料分析整合的進步

- 飛機機隊規模不斷擴大,營運效率需求不斷提高

- 嚴格的安全法規推動健康監測的採用

- 診斷即時資料分析日益受到關注

- 產業陷阱與挑戰

- 高昂的實施成本限制了小型航空公司的採用

- 資料安全問題影響系統可靠性和信任

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按解決方案,2021 年至 2034 年

- 主要趨勢

- 硬體

- 感應器

- 引擎和輔助動力裝置

- 飛機結構

- 輔助系統

- 航空電子設備

- 飛行資料管理系統

- 互聯飛機解決方案

- 地面伺服器

- 感應器

- 軟體

- 板載軟體

- 診斷飛行資料分析

- 預測飛行資料分析軟體

- 服務

第 6 章:市場估計與預測:按系統,2021 年至 2034 年

- 主要趨勢

- 引擎健康監測

- 結構健康監測

- 組件健康監測

第 7 章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 診斷

- 預測

- 自適應控制

- 規定性

第 8 章:市場估計與預測:按營運模式,2021 年至 2034 年

- 主要趨勢

- 即時的

- 非即時

第 9 章:市場估計與預測:按適合度,2021 年至 2034 年

- 主要趨勢

- 線擬合

- 復古版型

第 10 章:市場估計與預測:按安裝量,2021 年至 2034 年

- 主要趨勢

- 在船上

- 地面

第 11 章:市場估計與預測:按平台,2021-2034 年

- 主要趨勢

- 民事

- 軍隊

- 先進的空中機動性

第 12 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 13 章:公司簡介

- Air France KLM

- Airbus SE

- Boeing

- Curtiss-Wright Corporation

- Embraer

- FLYHT Aerospace Solutions Ltd.

- General Electric

- Honeywell International Inc

- Lufthansa

- Meggitt PLC

- Rolls-Royce PLC

- Safran Group

- Teledyne Controls LLC

The Global Aircraft Health Monitoring System Market was valued at USD 6.7 billion in 2024 and is projected to grow at a CAGR of 7.1% from 2025 to 2034. Increasing emphasis on predictive maintenance within the aviation sector is revolutionizing operational efficiency while minimizing unplanned downtime. Advanced technologies are enabling real-time data collection and analysis, allowing operators to identify potential failures and take preventive actions. This evolution is being driven by the integration of Internet of Things (IoT) devices and big data analytics, which provide comprehensive monitoring and predictive insights. Airlines and fleet operators are increasingly adopting these systems to ensure safety, optimize maintenance schedules, and reduce costs.

IoT sensors installed on aircraft capture critical operational data, such as engine performance, temperature, vibration, and fuel efficiency. This information is processed through cloud-based analytics platforms to identify anomalies, forecast maintenance needs, and enhance overall system reliability. The seamless communication between aircraft systems and ground operations fosters an integrated aviation network, improving decision-making processes and operational efficiency. As these technologies become more advanced, their adoption across commercial, private, and military aviation is expected to grow significantly.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.7 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 7.1% |

The market is segmented by solution into hardware, software, and services, with the hardware segment holding the largest share at 46.7% in 2024. Hardware components, including sensors and data acquisition devices, play a critical role in monitoring engine performance. These devices provide precise measurements of parameters such as temperature, pressure, and vibration, enabling early detection of potential issues. Advancements in hardware technology have resulted in smaller, lighter, and more durable components, enhancing efficiency and ease of installation. Integration with IoT systems further improves functionality by enabling seamless data sharing and cloud-based analysis. Operators prioritize hardware solutions that are reliable, cost-effective, and simple to maintain.

By fit, the market is divided into line fit and retrofit, with the line fit segment expected to grow at a CAGR of 7.8% during the forecast period. Line fit involves installing health monitoring systems during the aircraft manufacturing process, ensuring compatibility with specific models, and enhancing system integration. This approach reduces implementation costs and simplifies maintenance, making it a preferred choice for operators and manufacturers alike. As the demand for new aircraft rises, the line fit segment is set to experience significant growth.

The North American market is projected to exceed USD 5 billion by 2034, driven by a robust aerospace sector in the United States. The region benefits from the presence of major airlines, original equipment manufacturers, and advancements in machine learning and IoT technologies, bolstering the adoption of aircraft health monitoring systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for predictive maintenance in aviation sector

- 3.6.1.2 Advancements in IoT and big data analytics integration

- 3.6.1.3 Rising aircraft fleet size and operational efficiency needs

- 3.6.1.4 Stringent safety regulations driving health monitoring adoption

- 3.6.1.5 Growing focus on real-time data analysis for diagnostics

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High implementation costs limiting adoption in smaller airlines

- 3.6.2.2 Data security concerns impacting system reliability and trust

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Solution, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.1.1 Engines and auxiliary power units

- 5.2.1.2 Aerostructures

- 5.2.1.3 Ancillary systems

- 5.2.2 Avionics

- 5.2.3 Flight data management systems

- 5.2.4 Connected aircraft solutions

- 5.2.5 Ground servers

- 5.2.1 Sensors

- 5.3 Software

- 5.3.1 Onboard software

- 5.3.2 Diagnostic flight data analysis

- 5.3.3 Prognostic flight data analysis software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By System, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Engine health monitoring

- 6.3 Structural health monitoring

- 6.4 Component health monitoring

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Diagnostic

- 7.3 Prognostic

- 7.4 Adaptive control

- 7.5 Prescriptive

Chapter 8 Market Estimates & Forecast, By Operation Mode, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Real time

- 8.3 Non-Real time

Chapter 9 Market Estimates & Forecast, By Fit, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Line fit

- 9.3 Retro fit

Chapter 10 Market Estimates & Forecast, By Installation, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 On board

- 10.3 On ground

Chapter 11 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 11.1 Key trends

- 11.2 Civil

- 11.3 Military

- 11.4 Advanced air mobility

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Air France KLM

- 13.2 Airbus SE

- 13.3 Boeing

- 13.4 Curtiss-Wright Corporation

- 13.5 Embraer

- 13.6 FLYHT Aerospace Solutions Ltd.

- 13.7 General Electric

- 13.8 Honeywell International Inc

- 13.9 Lufthansa

- 13.10 Meggitt PLC

- 13.11 Rolls-Royce PLC

- 13.12 Safran Group

- 13.13 Teledyne Controls LLC