|

市場調查報告書

商品編碼

1684519

動脈插管市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Arterial Cannula Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

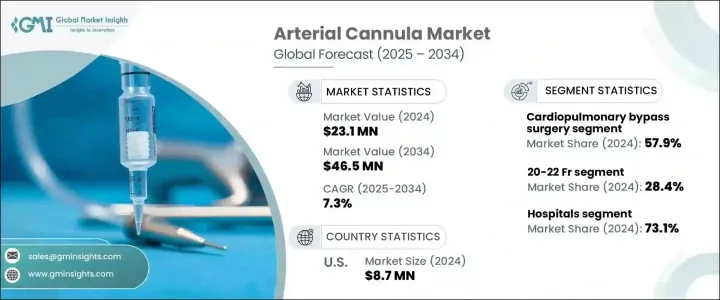

2024 年全球動脈插管市場價值為 2,310 萬美元,預計將經歷顯著成長,2025 年至 2034 年的複合年成長率為 7.3%。此外,心臟手術報銷政策的推出也促進了動脈套管的更廣泛使用,從而促進了整體市場的成長。

冠狀動脈疾病、心臟衰竭和中風等心血管疾病在全球範圍內的負擔日益加重,增加了對動脈插管等先進醫療設備的需求,這些設備對於各種心臟手術、ECMO(體外膜氧合)程序和其他救生干預措施至關重要。這些設備在改善手術和重症監護治療期間的患者結果方面發揮著至關重要的作用,從而促進了它們在醫院和外科中心的廣泛使用。套管技術的創新提高了安全性、有效性和病患舒適度,也有助於推動市場需求。此外,隨著醫療保健系統繼續投資於最新的醫療技術和外科手術,動脈套管仍然是治療方案的核心組成部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2310 萬美元 |

| 預測值 | 4650 萬美元 |

| 複合年成長率 | 7.3% |

市場按尺寸細分,包括 14-16 Fr、17-19 Fr、20-22 Fr、23-25 Fr、26-28 Fr、29-31 Fr、32-34 Fr 和 35-36 Fr 等。 20-22 Fr 尺寸類別在 2024 年佔據了最大的市場佔有率,為 28.4%。 20-22 Fr 套管針提供了有效性和安全性的最佳組合,可減少插入過程中的血管損傷和出血等併發症,確保與成人動脈結構的兼容性。與較大尺寸的套管相比,它的侵入性較小,使其成為成年患者動脈插管的首選。

就最終用戶而言,市場分為醫院、門診手術中心和其他。 2024 年,醫院佔據了 73.1% 的市場佔有率,佔據了市場主導地位。動脈插管是心肺分流術和 ECMO 等救命治療的重要工具,這兩種治療在醫院環境中都已廣泛應用。隨著對先進外科手術和重症監護治療的需求不斷上升,醫院預計將保持其作為最大終端用戶群的地位。

在美國動脈插管市場,該產業在 2024 年創造了 870 萬美元的收入。這兩種治療方法都嚴重依賴動脈套管,鞏固了該設備在國家醫療保健系統中的關鍵作用,並進一步推動市場成長。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 心血管疾病盛行率不斷上升

- 重症監護環境中呼吸和心臟支持的使用日益增多

- 套管設計的進步

- 心臟和重症監護手術的報銷和保險覆蓋範圍

- 產業陷阱與挑戰

- 嚴格的監管要求

- 與 ECMO 和心肺手術相關的複雜性

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望

第5章:市場估計與預測:依規模,2021 – 2034 年

- 主要趨勢

- 14-16 星期五

- 17-19 星期五

- 20-22 星期五

- 23-25 星期五

- 26-28 星期五

- 29-31 星期五

- 32-34 星期五

- 35-36 星期五

第 6 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 心肺旁路手術

- 體外膜氧合

- 其他應用

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用戶

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Andocor

- B. Braun

- Becton, Dickinson and Company

- Edward Lifesciences

- Freelife Medical

- Fresenius Medical Care

- Getinge

- ICU Medical

- Kangxin Medical

- LivaNova

- Medtronic

- Nipro Corporation

- Polymedicure

- Surgical Holdings

- Terumo Corporation

The Global Arterial Cannula Market was valued at USD 23.1 million in 2024 and is projected to experience significant growth with an anticipated CAGR of 7.3% from 2025 to 2034. Several key factors are driving this market expansion, including the rising prevalence of cardiovascular diseases, advancements in cannula technology, and the increasing adoption of respiratory and cardiac support systems in critical care settings. Additionally, the availability of reimbursement policies for cardiac procedures is fostering the wider use of arterial cannulas, contributing to the overall market growth.

The growing global burden of cardiovascular diseases, including coronary artery disease, heart failure, and stroke, has heightened the demand for advanced medical devices such as arterial cannulas, which are critical for various cardiac surgeries, ECMO (extracorporeal membrane oxygenation) procedures, and other life-saving interventions. These devices play a crucial role in improving patient outcomes during surgeries and critical care treatments, thereby spurring their widespread use across hospitals and surgical centers. Innovations in cannula technology, which improve safety, effectiveness, and patient comfort, are also helping propel market demand. Furthermore, as healthcare systems continue to invest in the latest medical technologies and surgical interventions, arterial cannulas remain a core component of treatment protocols.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.1 Million |

| Forecast Value | $46.5 Million |

| CAGR | 7.3% |

The market is segmented by size, with options such as 14-16 Fr, 17-19 Fr, 20-22 Fr, 23-25 Fr, 26-28 Fr, 29-31 Fr, 32-34 Fr, and 35-36 Fr. The 20-22 Fr size category held the largest market share of 28.4% in 2024. This size is particularly favored due to its balanced performance during ECMO procedures and cardiac surgeries, especially for adult patients. Offering an optimal mix of effectiveness and safety, the 20-22 Fr cannula reduces complications like vascular damage and bleeding during insertion, ensuring compatibility with adult arterial structures. Its less invasive nature, compared to larger cannula sizes, makes it the preferred choice for arterial cannulation in adult patients.

In terms of end-users, the market is categorized into hospitals, ambulatory surgical centers, and others. Hospitals dominated the market with a 73.1% share in 2024. The increasing number of critical cardiac and intensive care procedures being performed in hospitals is a major factor contributing to this segment's dominance. Arterial cannulas are an essential tool in life-saving treatments such as cardiopulmonary bypass and ECMO, both of which are extensively used in hospital settings. As the demand for advanced surgical interventions and critical care treatments continues to rise, hospitals are expected to maintain their position as the largest end-user segment.

In the U.S. arterial cannula market, the sector generated USD 8.7 million in 2024. The high prevalence of cardiovascular diseases such as coronary artery disease, heart failure, and stroke plays a significant role in driving the demand for ECMO procedures and cardiac surgeries. Both of these treatments heavily rely on arterial cannulas, solidifying the device's critical role in the country's healthcare system and further fueling market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cardiovascular disorders

- 3.2.1.2 Growing use of respiratory and cardiac support in critical care settings

- 3.2.1.3 Advancements in cannula design

- 3.2.1.4 Availability of reimbursements and coverage for cardiac and critical care procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements

- 3.2.2.2 Complexity associated with ECMO and cardiopulmonary procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Size, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 14-16 Fr

- 5.3 17-19 Fr

- 5.4 20-22 Fr

- 5.5 23-25 Fr

- 5.6 26-28 Fr

- 5.7 29-31 Fr

- 5.8 32-34 Fr

- 5.9 35-36 Fr

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiopulmonary bypass surgery

- 6.3 Extracorporeal membrane oxygenation

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Andocor

- 9.2 B. Braun

- 9.3 Becton, Dickinson and Company

- 9.4 Edward Lifesciences

- 9.5 Freelife Medical

- 9.6 Fresenius Medical Care

- 9.7 Getinge

- 9.8 ICU Medical

- 9.9 Kangxin Medical

- 9.10 LivaNova

- 9.11 Medtronic

- 9.12 Nipro Corporation

- 9.13 Polymedicure

- 9.14 Surgical Holdings

- 9.15 Terumo Corporation

套管系統市場規模、佔有率和成長分析(按產品類型、材料、尺寸、最終用途和地區)- 產業預測 2025-2032

套管系統市場規模、佔有率和成長分析(按產品類型、材料、尺寸、最終用途和地區)- 產業預測 2025-2032 動脈插管市場規模、佔有率、趨勢分析報告:按應用、規模、最終用途、地區、細分市場、預測,2025-2030 年

動脈插管市場規模、佔有率、趨勢分析報告:按應用、規模、最終用途、地區、細分市場、預測,2025-2030 年 插管市場,按產品、按尺寸、按類型、按材料、按最終用戶、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

插管市場,按產品、按尺寸、按類型、按材料、按最終用戶、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 插管市場:按產品、材料、應用和最終用戶分類 - 全球預測 2025-20302024-2032 年按產品、類型、尺寸、材料(塑膠插管、矽膠插管、金屬插管)、應用、最終用戶(醫院、門診手術中心等)和地區分列的插管市場報告插管市場規模、佔有率和趨勢分析報告:按產品、類型、材料、尺寸、最終用途、地區和細分市場進行預測,2024-2030 年

插管市場:按產品、材料、應用和最終用戶分類 - 全球預測 2025-20302024-2032 年按產品、類型、尺寸、材料(塑膠插管、矽膠插管、金屬插管)、應用、最終用戶(醫院、門診手術中心等)和地區分列的插管市場報告插管市場規模、佔有率和趨勢分析報告:按產品、類型、材料、尺寸、最終用途、地區和細分市場進行預測,2024-2030 年 插管市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、類型、材料、規模、最終用途產業、地區和競爭細分,2019-2029F

插管市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、類型、材料、規模、最終用途產業、地區和競爭細分,2019-2029F 血管造口插管市場:各類型,各用途,各終端用戶,各地區-2023~2030年的市場規模,佔有率,展望,機會分析

血管造口插管市場:各類型,各用途,各終端用戶,各地區-2023~2030年的市場規模,佔有率,展望,機會分析