|

市場調查報告書

商品編碼

1684522

海軍艦艇市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Naval Vessels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

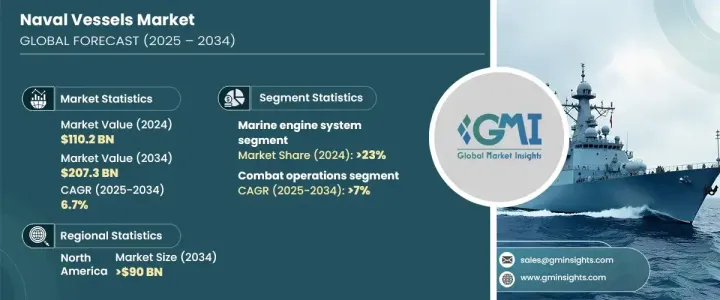

2024 年全球海軍艦艇市場規模將達到 1102 億美元,預計在 2025 年至 2034 年期間的複合年成長率為 6.7%。世界各國政府和國防組織正在大力投資尖端海軍技術,以加強海上安全並應對不斷演變的威脅。海軍艦隊的現代化,加上人工智慧(AI)、自主系統和先進推進技術的融合,正在重塑市場格局。日益加劇的地緣政治緊張局勢和海洋領土爭端進一步凸顯了海軍艦艇在國家安全戰略中的關鍵作用。此外,向環保推進系統的轉變表明了該行業對嚴格的環境法規的回應,強調永續性和營運效率。

市場依系統細分為船用引擎系統、武器發射系統、控制系統、電氣系統、通訊系統等。其中,船用引擎系統部門在 2024 年佔據了 23% 的市場佔有率,預計未來幾年將大幅擴大。海軍艦艇的推進技術正在迅速發展,明顯轉向混合動力和生物燃料驅動系統。這些技術將電動馬達與傳統燃料引擎結合在一起,符合環境要求,同時滿足現代驅逐艦和潛艇的戰術和作戰需求。對節能系統的推動反映出人們越來越重視在不影響性能的情況下減少軍事行動的碳足跡。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1102億美元 |

| 預測值 | 2073億美元 |

| 複合年成長率 | 6.7% |

根據應用,市場分為沿海作業、搜救任務、作戰行動、水雷對抗 (MCM) 作業等。作戰行動領域預計將經歷強勁成長,到 2034 年複合年成長率將達到 7%。這些技術增強了武器的射程、準確性和整體效能,為沿海地區及其他地區提供了卓越的防禦能力。此外,人工智慧和自主技術的融合從根本上改變了海軍作戰,實現了快速威脅偵測、簡化任務執行並增強了跨多個領域的態勢感知。

北美仍然是海軍艦艇市場的主要參與者,特別是在驅逐艦和潛艇領域。在美國注重提升海軍能力的推動下,該地區預計到 2034 年將創造 900 億美元的價值。美國繼續在高超音速武器和自主系統方面投入大量資金,引領市場,確保戰略主導地位和無與倫比的作戰效率。海軍艦艇市場的成長得益於國防投資的增加、推進技術的進步以及人工智慧和自主解決方案的日益普及,鞏固了其在全球海上安全中的關鍵作用。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 地緣政治緊張局勢加劇和軍事現代化

- 增加國防預算

- 潛艦戰略防禦需求不斷成長

- 海上安全日益受關注

- 更加重視海軍艦隊多樣化

- 產業陷阱與挑戰

- 開發和維護成本高

- 地緣政治不穩定與監管限制

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依船舶類型,2021-2034 年

- 主要趨勢

- 驅逐艦

- 護衛艦

- 潛水艇

- 護衛艦

- 航空母艦

- 其他

第 6 章:市場估計與預測:按系統,2021 年至 2034 年

- 主要趨勢

- 船舶引擎系統

- 武器發射系統

- 控制系統

- 電氣系統

- 通訊系統

- 其他

第 7 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 搜救

- 戰鬥行動

- 反水雷 (MCM) 行動

- 沿海作業

- 其他

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Austal

- BAE Systems

- Damen Shipyards

- Fincantieri

- General Dynamics

- Hanwha Ocean

- HD Korea Shipbuilding

- Huntington Ingalls

- Larsen & Toubro

- Lockheed Martin

- Naval Group

- ThyssenKrupp

The Global Naval Vessels Market reached USD 110.2 billion in 2024 and is poised to grow at a CAGR of 6.7% between 2025 and 2034. This growth trajectory reflects the rising prevalence of security threats across the globe, which has led to an unprecedented surge in demand for advanced offensive and defensive weapon systems. Governments and defense organizations worldwide are investing heavily in cutting-edge naval technologies to strengthen their maritime security and address evolving threats. The modernization of naval fleets, combined with the integration of artificial intelligence (AI), autonomous systems, and advanced propulsion technologies, is reshaping the market landscape. Increasing geopolitical tensions and disputes over maritime territories further underscore the critical role of naval vessels in national security strategies. Additionally, the transition toward eco-friendly propulsion systems demonstrates the sector's response to stringent environmental regulations, emphasizing sustainability alongside operational efficiency.

The market is segmented by system into marine engine systems, weapon launch systems, control systems, electrical systems, communication systems, and others. Among these, the marine engine systems segment accounted for 23% of the market share in 2024 and is anticipated to expand significantly in the coming years. Propulsion technologies for naval vessels are advancing rapidly, with a notable shift toward hybrid and biofuel-driven systems. These technologies integrate electric motors with conventional fuel engines, aligning with environmental mandates while addressing the tactical and operational needs of modern destroyers and submarines. The push for energy-efficient systems reflects a growing emphasis on reducing the carbon footprint of military operations without compromising performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $110.2 billion |

| Forecast Value | $207.3 billion |

| CAGR | 6.7% |

By application, the market is categorized into coastal operations, search and rescue missions, combat operations, Mine Countermeasures (MCM) operations, and others. The combat operations segment is expected to witness robust growth, registering a CAGR of 7% through 2034. Revolutionary advancements such as hypersonic missile technology, directed energy systems, and precision torpedoes are transforming the capabilities of naval combat forces. These technologies enhance weapon range, accuracy, and overall effectiveness, providing superior defense capabilities for coastal regions and beyond. Furthermore, the integration of AI and autonomous technologies has fundamentally changed naval operations, enabling rapid threat detection, streamlined mission execution, and enhanced situational awareness across multiple domains.

North America remains a key player in the naval vessels market, particularly in the destroyers and submarines segments. The region is projected to generate USD 90 billion in value by 2034, driven by the United States' focus on advancing naval capabilities. The U.S. continues to lead the market with substantial investments in hypersonic weapons and autonomous systems, ensuring strategic dominance and unmatched operational efficiency. The naval vessels market growth is fueled by rising defense investments, advancements in propulsion technologies, and the growing incorporation of AI and autonomous solutions, solidifying its critical role in global maritime security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing geopolitical tensions and military modernization

- 3.6.1.2 Increasing defense budgets

- 3.6.1.3 Growing demand for submarine-based strategic defense

- 3.6.1.4 Rising focus on maritime security

- 3.6.1.5 Increased focus on naval fleet diversification

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and maintenance costs

- 3.6.2.2 Geopolitical instability and regulatory constraints

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vessel Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Destroyers

- 5.3 Frigates

- 5.4 Submarines

- 5.5 Corvettes

- 5.6 Aircraft carriers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By System, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Marine engine system

- 6.3 Weapon launch system

- 6.4 Control system

- 6.5 Electrical system

- 6.6 Communication system

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Search and rescue

- 7.3 Combat operations

- 7.4 Mine countermeasures (MCM) operations

- 7.5 Coastal Operations

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Austal

- 9.2 BAE Systems

- 9.3 Damen Shipyards

- 9.4 Fincantieri

- 9.5 General Dynamics

- 9.6 Hanwha Ocean

- 9.7 HD Korea Shipbuilding

- 9.8 Huntington Ingalls

- 9.9 Larsen & Toubro

- 9.10 Lockheed Martin

- 9.11 Naval Group

- 9.12 ThyssenKrupp

全球海軍艦艇市場:趨勢、預測與競爭分析(~2031年)

全球海軍艦艇市場:趨勢、預測與競爭分析(~2031年) 海軍艦艇 MRO 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按船舶類型、MRO 類型、地區和競爭細分,2019-2029F

海軍艦艇 MRO 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按船舶類型、MRO 類型、地區和競爭細分,2019-2029F 海軍艦艇和水面作戰艦艇市場 - 全球產業規模、佔有率、趨勢、機會和預測,按船舶類型、系統類型、地區和競爭細分,2019-2029F

海軍艦艇和水面作戰艦艇市場 - 全球產業規模、佔有率、趨勢、機會和預測,按船舶類型、系統類型、地區和競爭細分,2019-2029F 全球海軍艦艇和水上戰鬥機市場:市場規模與趨勢分析(市場區隔,主要計劃,競爭情形,預測):2024年~2034年

全球海軍艦艇和水上戰鬥機市場:市場規模與趨勢分析(市場區隔,主要計劃,競爭情形,預測):2024年~2034年 2024-2028年全球海軍艦艇市場

2024-2028年全球海軍艦艇市場 全球無人水面艦艇及潛水器市場(2024-2034)

全球無人水面艦艇及潛水器市場(2024-2034) 2024-2028年全球核能戰艦市場

2024-2028年全球核能戰艦市場 全球海軍艦艇MRO市場2024-2028

全球海軍艦艇MRO市場2024-2028