|

市場調查報告書

商品編碼

1684634

即時乘客資訊系統市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Real-Time Passenger Information Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

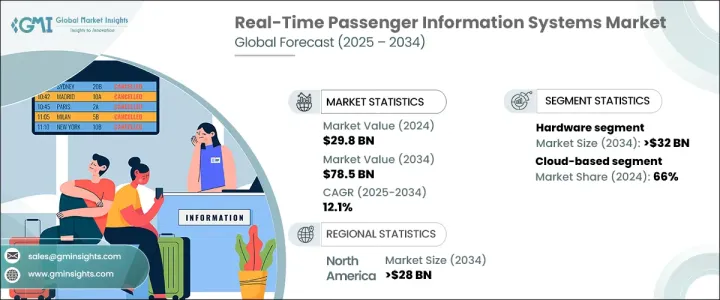

2024 年全球即時乘客資訊系統市場規模價值 298 億美元,預計 2025 年至 2034 年期間的複合年成長率為 12.1%。這些系統旨在提高公共交通效率並減少延誤。透過向通勤者提供準確的即時時間表、路線和中斷資訊更新,RTPI 系統能夠幫助他們做出明智的出行決策。它們與智慧城市計劃的結合確保了公共交通網路的無縫連接,進一步改善了城市交通。

世界各國政府在推動 RTPI 系統市場成長方面發揮著至關重要的作用。隨著城市化進程的加快,政府部門大力投資智慧城市項目,升級交通基礎設施,以提高效率和乘客滿意度。 RTPI 系統提供公車、火車和電車時刻表的即時更新,正在成為這些現代化建設不可或缺的一部分。這些系統不僅提升了整體乘客體驗,而且有助於降低公共交通網路的營運效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 298億美元 |

| 預測值 | 785億美元 |

| 複合年成長率 | 12.1% |

市場根據組件分為硬體、軟體和服務。 2024 年,硬資料部分佔據了 40% 的市場佔有率,預計到 2034 年將創造 320 億美元的市場價值。顯示單元、GPS 設備、感測器、路由器和通訊設備等基本硬體組件構成了 RTPI 系統的骨幹。這些元件確保資料來源和最終用戶之間的無縫交互,使其成為 RTPI 系統有效運作不可或缺的一部分。

根據部署模式,即時乘客資訊市場分為本地解決方案和基於雲端的解決方案。到 2024 年,基於雲端運算的領域將佔據約 66% 的市場佔有率,這得益於其可擴展性、成本效益和易於部署。雲端解決方案消除了對大量內部基礎設施的需求,大大降低了前期成本並實現了更快的實施。這些解決方案還提供無縫的資料儲存和處理功能,確保跨多個平台為乘客提供即時更新。對基於雲端的解決方案的日益青睞凸顯了市場向更靈活、更有效率的部署模式的轉變。

2024 年,北美佔據即時乘客資訊市場 35% 的收入佔有率,預計到 2034 年將超過 280 億美元。紐約、芝加哥、洛杉磯等主要大都會區正積極部署RTPI系統,以提升乘客體驗並提高運輸效率。該地區專注於技術進步和基礎設施發展,使其成為全球 RTPI 系統市場的重要參與者。

總體而言,即時乘客資訊系統市場在預測期內將實現顯著成長。智慧城市計畫的不斷採用,加上技術的進步,預計將推動全球對 RTPI 系統的需求。隨著政府和交通管理部門繼續優先考慮效率和乘客滿意度,未來幾年市場可能會持續保持成長勢頭。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 組件提供者

- 系統整合商

- 通訊和網路供應商

- 數據提供者

- 大眾運輸業者

- 利潤率分析

- 成本分解與價格分析

- 即時資料更新相對於靜態系統的優勢

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 對智慧交通解決方案的需求增加

- 政府採取措施推動公共交通現代化

- 通訊技術的進步

- 行動裝置和應用程式的普及率不斷提高

- 更重視安全與保障

- 產業陷阱與挑戰

- 實施和維護成本高

- 數據準確性和可靠性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 硬體

- 顯示器

- 網路裝置

- 感應器

- 通訊設備

- 軟體

- 資料管理軟體

- 資訊顯示軟體

- 服務

- 安裝和維護

- 諮詢與系統整合

第 6 章:市場估計與預測:按解決方案,2021 - 2034 年

- 主要趨勢

- 資訊顯示系統

- 公告系統

- 資訊娛樂系統

- 緊急通訊系統

- 視訊監控系統

- 其他

第 7 章:市場估計與預測:按運輸方式,2021 - 2034 年

- 主要趨勢

- 道路

- 鐵路

- 航空

- 水路

第 8 章:市場估計與預測:按部署模式,2021 - 2034 年

- 主要趨勢

- 本地

- 基於雲端

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Advantech

- Alstom

- Cisco Systems

- Cubic

- Dysten

- Efftronics Systems

- Hitachi

- Huawei Technologies

- Icon Multimedia

- Indra Sistemas

- Medha Servo Drives

- Mitsubishi Electric

- Nokia

- r2p Group

- Siemens Mobility

- ST Engineering

- Teleste

- Televic

- Thales Group

- Wabtec

The Global Real-Time Passenger Information System Market size was valued at USD 29.8 billion in 2024 and is projected to grow at a CAGR of 12.1% between 2025 and 2034. The increasing pace of urbanization and worsening traffic congestion are compelling cities to adopt real-time passenger information (RTPI) systems. These systems are designed to enhance public transit efficiency and reduce delays. By providing commuters with accurate, real-time updates on schedules, routes, and disruptions, RTPI systems enable informed travel decisions. Their integration with smart city initiatives further improves urban mobility by ensuring seamless connectivity across public transport networks.

Governments worldwide are playing a crucial role in driving the growth of the RTPI systems market. With urbanization on the rise, authorities are heavily investing in smart city projects and upgrading transportation infrastructure to improve efficiency and passenger satisfaction. RTPI systems, which provide real-time updates on bus, train, and tram schedules, are becoming an integral part of these modernization efforts. These systems not only enhance the overall passenger experience but also contribute to reducing operational inefficiencies in public transportation networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.8 Billion |

| Forecast Value | $78.5 Billion |

| CAGR | 12.1% |

The market is segmented based on components into hardware, software, and services. In 2024, the hardware segment accounted for 40% of the market share and is expected to generate USD 32 billion by 2034. The hardware segment continues to dominate the real-time passenger information (RTPI) systems market due to its critical role in enabling real-time data collection and dissemination. Essential hardware components, such as display units, GPS devices, sensors, routers, and communication devices, form the backbone of RTPI systems. These components ensure seamless interaction between data sources and end-users, making them indispensable for the effective functioning of RTPI systems.

Based on deployment mode, the real-time passenger information market is divided into on-premise and cloud-based solutions. The cloud-based segment held approximately 66% of the market share in 2024, driven by its scalability, cost-effectiveness, and ease of deployment. Cloud solutions eliminate the need for extensive on-premise infrastructure, significantly reducing upfront costs and enabling faster implementation. These solutions also provide seamless data storage and processing capabilities, ensuring real-time updates for passengers across multiple platforms. The growing preference for cloud-based solutions highlights the market's shift toward more flexible and efficient deployment models.

North America accounted for 35% of the revenue share in the real-time passenger information market in 2024 and is expected to exceed USD 28 billion by 2034. The United States leads the market in the North American region, with projections indicating it will surpass USD 24 billion by 2034. This growth is attributed to advanced public transportation networks and substantial investments in smart city initiatives. Major metropolitan areas, including New York, Chicago, and Los Angeles, are actively deploying RTPI systems to enhance passenger experiences and improve transportation efficiency. The region's focus on technological advancements and infrastructure development positions it as a key player in the global RTPI systems market.

Overall, the real-time passenger information systems market is poised for significant growth during the forecast period. The increasing adoption of smart city initiatives, coupled with advancements in technology, is expected to drive demand for RTPI systems globally. As governments and transportation authorities continue to prioritize efficiency and passenger satisfaction, the market is likely to witness sustained momentum in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 System integrators

- 3.2.3 Communication and network providers

- 3.2.4 Data providers

- 3.2.5 Public transport operators

- 3.3 Profit margin analysis

- 3.4 Cost breakdown and price analysis

- 3.5 Benefits of real-time data updates vs. static systems

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increased demand for smart transportation solutions

- 3.9.1.2 Government initiatives for modernizing public transport

- 3.9.1.3 Advancements in communication technologies

- 3.9.1.4 Growing adoption of mobile devices and apps

- 3.9.1.5 Increasing focus on safety and security

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High implementation and maintenance costs

- 3.9.2.2 Data accuracy and reliability concern

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Displays

- 5.2.2 Networking devices

- 5.2.3 Sensors

- 5.2.4 Communication devices

- 5.3 Software

- 5.3.1 Data management software

- 5.3.2 Information display software

- 5.4 Services

- 5.4.1 Installation and maintenance

- 5.4.2 Consulting and system integration

Chapter 6 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Information display system

- 6.3 Announcement system

- 6.4 Infotainment system

- 6.5 Emergency communication system

- 6.6 Video surveillance system

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Mode of Transportation, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Roadways

- 7.3 Railways

- 7.4 Airways

- 7.5 Waterways

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 On-premise

- 8.3 Cloud-based

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Advantech

- 10.2 Alstom

- 10.3 Cisco Systems

- 10.4 Cubic

- 10.5 Dysten

- 10.6 Efftronics Systems

- 10.7 Hitachi

- 10.8 Huawei Technologies

- 10.9 Icon Multimedia

- 10.10 Indra Sistemas

- 10.11 Medha Servo Drives

- 10.12 Mitsubishi Electric

- 10.13 Nokia

- 10.14 r2p Group

- 10.15 Siemens Mobility

- 10.16 ST Engineering

- 10.17 Teleste

- 10.18 Televic

- 10.19 Thales Group

- 10.20 Wabtec

2025年全球自動乘客引導系統市場報告

2025年全球自動乘客引導系統市場報告 乘客資訊系統市場:未來預測(2025-2030)

乘客資訊系統市場:未來預測(2025-2030) 2025-2033 年按組件、飛機、配銷通路和地區分類的航空客運通訊系統市場報告2025-2033 年按運輸方式、組件、系統類型、位置和地區分類的客運資訊系統市場報告全球乘客資訊系統市場:按組件、位置、功能模型、交通途徑和最終用戶 - 預測 2025-2030全球自動客運資訊系統市場:按組件、類型、功能、運輸方式和最終用戶分類 - 預測 2025-2030

2025-2033 年按組件、飛機、配銷通路和地區分類的航空客運通訊系統市場報告2025-2033 年按運輸方式、組件、系統類型、位置和地區分類的客運資訊系統市場報告全球乘客資訊系統市場:按組件、位置、功能模型、交通途徑和最終用戶 - 預測 2025-2030全球自動客運資訊系統市場:按組件、類型、功能、運輸方式和最終用戶分類 - 預測 2025-2030 客運資訊系統市場規模、佔有率、按產品、地點、交通途徑和地區分類的成長分析 - 產業預測,2024-2031 年

客運資訊系統市場規模、佔有率、按產品、地點、交通途徑和地區分類的成長分析 - 產業預測,2024-2031 年 2024-2028 年全球乘客資訊系統市場乘客資訊系統的全球市場預測(截至 2030 年):按組件、交通途徑、功能模型、位置和區域進行分析

2024-2028 年全球乘客資訊系統市場乘客資訊系統的全球市場預測(截至 2030 年):按組件、交通途徑、功能模型、位置和區域進行分析 乘客資訊系統(PIS)的全球市場:透過提供細分市場(解決方案/服務)、位置(機上/車內/機上、車站內)、交通方式(鐵路(火車/路面電車)、公路、航空和水路)和地區- 預測(~2028)

乘客資訊系統(PIS)的全球市場:透過提供細分市場(解決方案/服務)、位置(機上/車內/機上、車站內)、交通方式(鐵路(火車/路面電車)、公路、航空和水路)和地區- 預測(~2028)