|

市場調查報告書

商品編碼

1684647

抗 VEGF 治療市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Anti-VEGF Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

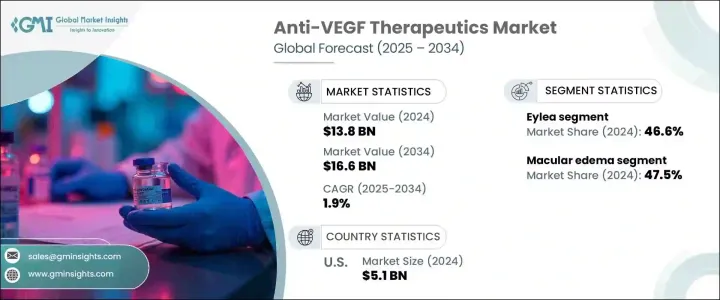

2024 年全球抗 VEGF 治療市場價值為 138 億美元,預計將穩定成長,預計 2025 年至 2034 年的複合年成長率為 1.9%。這一成長主要受多種因素推動,例如眼部疾病患病率不斷上升、全球人口老化以及對可用治療方案的認知不斷提高。老年黃斑部病變 (AMD)、糖尿病視網膜病變和視網膜靜脈阻塞是推動抗 VEGF 療法需求的主要疾病。這些疾病通常與血管異常生長有關,可以使用 VEGF 抑制劑有效治療。由於這些療法顯著改善了視力和整體疾病管理,它們已成為眼科的重要組成部分。

市場受到關鍵細分領域的影響,包括提供令人印象深刻的臨床結果和更長的給藥間隔的著名抗 VEGF 療法。 2024 年,一種此類療法由於減少了注射頻率,提高了患者的便利性和對治療方案的依從性,佔據了 46.6% 的市場佔有率。由於注射次數較少,該療法成為醫療保健提供者的首選,並促進了其日益廣泛的應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 138億美元 |

| 預測值 | 166億美元 |

| 複合年成長率 | 1.9% |

從應用方面來看,黃斑水腫、糖尿病視網膜病變、視網膜靜脈阻塞、AMD、近視脈絡膜新生血管是市場的主要類別。黃斑水腫通常由糖尿病和血管併發症引起,2024 年該疾病佔 47.5% 的市場佔有率,佔據市場主導地位。全球糖尿病盛行率的上升加劇了黃斑水腫的發生,推動了對針對性治療的需求增加。隨著越來越多的患者被診斷出患有這種疾病並接受治療,盛行率的變化是推動成長的重要動力,導致治療需求顯著上升。

在美國,受人口老化和視網膜疾病高發生率的推動,抗 VEGF 治療市場規模將在 2024 年達到 51 億美元。 AMD 仍然是導致視力障礙的主要原因之一,在市場擴張中發揮著至關重要的作用。美國先進的醫療保健體系確保患者能夠廣泛接受尖端治療,並透過全面的報銷框架提供支援。這種可及性使更多患者受益於抗 VEGF 療法,鞏固了美國在全球市場的主導地位。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 眼部疾病發生率不斷上升

- 老齡人口增加

- 藥物開發的技術進步

- 人們越來越意識到及時治療眼科疾病

- 產業陷阱與挑戰

- 治療費用高昂

- 副作用和安全問題

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 艾莉婭

- 路欣迪

- 貝奧武

- 瓦比斯莫

- 其他產品

第 6 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 黃斑水腫

- 糖尿病視網膜病變

- 視網膜靜脈阻塞

- 老年性黃斑部病變

- 近視脈絡膜新生血管

第 7 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Alcon

- Amgen

- Bausch Health Companies

- Bayer

- Biogen

- Bristol-Myers Squibb

- Coherus BioSciences

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Hoya Corporation

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Viatris

The Global Anti-VEGF Therapeutics Market, valued at USD 13.8 billion in 2024, is poised to expand steadily with a projected CAGR of 1.9% from 2025 to 2034. This growth is primarily driven by a combination of factors such as the increasing prevalence of eye diseases, the aging global population, and heightened awareness surrounding available treatment options. Age-related macular degeneration (AMD), diabetic retinopathy, and retinal vein occlusion are among the leading conditions fueling the demand for anti-VEGF therapies. These diseases are typically associated with abnormal blood vessel growth, which can be effectively treated using VEGF inhibitors. As these therapies offer significant improvements in vision and overall disease management, they have become an essential part of ophthalmology.

The market is being shaped by key segments, including prominent anti-VEGF therapies that offer impressive clinical outcomes and longer dosing intervals. In 2024, one such therapy captured a substantial 46.6% market share due to its reduced injection frequency, enhancing patient convenience and adherence to treatment regimens. The ability to receive fewer injections has made this therapy the preferred choice among healthcare providers, contributing to its growing adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.8 Billion |

| Forecast Value | $16.6 Billion |

| CAGR | 1.9% |

In terms of application, macular edema, diabetic retinopathy, retinal vein occlusion, AMD, and myopic choroidal neovascularization represent the main categories within the market. Macular edema, which often results from diabetes and vascular complications, led the market with a 47.5% share in 2024. The rising global prevalence of diabetes has exacerbated the occurrence of macular edema, driving an increased demand for targeted treatments. This shift in prevalence is a significant driver of growth, as more patients are diagnosed and treated for the condition, resulting in a notable uptick in therapeutic needs.

In the U.S., the anti-VEGF therapeutics market reached USD 5.1 billion in 2024, driven by the country's aging population and the high incidence of retinal disorders. AMD remains one of the leading causes of vision impairment, playing a crucial role in market expansion. The advanced healthcare system in the U.S. ensures that patients have broad access to cutting-edge treatments, bolstered by a comprehensive reimbursement framework. This accessibility has allowed more patients to benefit from anti-VEGF therapies, solidifying the U.S. as a dominant force within the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of eye diseases

- 3.2.1.2 Rise in aging population

- 3.2.1.3 Technological advancements in drug development

- 3.2.1.4 Growing awareness towards timely treatment of ophthalmic disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects and safety concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Eylea

- 5.3 Lucentis

- 5.4 Beovu

- 5.5 Vabysmo

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Macular edema

- 6.3 Diabetic retinopathy

- 6.4 Retinal vein occlusion

- 6.5 Age-related macular degeneration

- 6.6 Myopic choroidal neovascularization

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Alcon

- 8.2 Amgen

- 8.3 Bausch Health Companies

- 8.4 Bayer

- 8.5 Biogen

- 8.6 Bristol-Myers Squibb

- 8.7 Coherus BioSciences

- 8.8 Eli Lilly and Company

- 8.9 F. Hoffmann-La Roche

- 8.10 Hoya Corporation

- 8.11 Novartis

- 8.12 Pfizer

- 8.13 Regeneron Pharmaceuticals

- 8.14 Sanofi

- 8.15 Viatris

2030 年近視治療市場預測:按類型、治療方法、給藥途徑、年齡層、最終用戶和地區進行的全球分析

2030 年近視治療市場預測:按類型、治療方法、給藥途徑、年齡層、最終用戶和地區進行的全球分析 全球眼科包裝市場 - 2025 - 2033

全球眼科包裝市場 - 2025 - 2033 眼科器材市場:按產品、診斷、最終用戶、分銷管道 - 全球預測 2025-2030眼科器材市場:按設備、按應用分類 - 2025-2030 年全球預測

眼科器材市場:按產品、診斷、最終用戶、分銷管道 - 全球預測 2025-2030眼科器材市場:按設備、按應用分類 - 2025-2030 年全球預測 獸醫眼科設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭細分,2019-2029F先進眼科技術市場:按類型、最終用戶分類 - 2025-2030 年全球預測獸醫眼科設備市場:按設備類型、動物類型和最終用戶分類 - 2025-2030 年全球預測眼科市場:按疾病、產品類型、最終用戶分類 - 全球預測 2025-2030眼藥水市場:按類型、類別、最終用戶、適應症分類 - 全球預測 2025-2030糖尿病相關眼部治療市場:按產品類型、應用和最終用途分類-2025-2030 年全球預測

獸醫眼科設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭細分,2019-2029F先進眼科技術市場:按類型、最終用戶分類 - 2025-2030 年全球預測獸醫眼科設備市場:按設備類型、動物類型和最終用戶分類 - 2025-2030 年全球預測眼科市場:按疾病、產品類型、最終用戶分類 - 全球預測 2025-2030眼藥水市場:按類型、類別、最終用戶、適應症分類 - 全球預測 2025-2030糖尿病相關眼部治療市場:按產品類型、應用和最終用途分類-2025-2030 年全球預測