|

市場調查報告書

商品編碼

1684675

產後憂鬱症治療市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Postpartum Depression Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

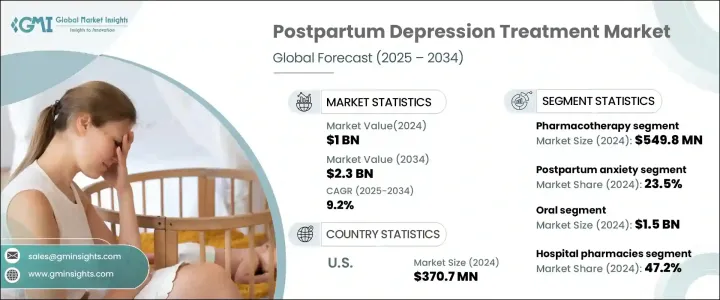

2024 年全球產後憂鬱症治療市場規模達到 10 億美元,預計 2025 年至 2034 年期間將以 9.2% 的強勁複合年成長率擴張。產後憂鬱症影響全球相當一部分新手媽媽,成為人們關注的公共衛生議題。

隨著心理健康成為產婦護理的核心組成部分,世界各地的醫療保健系統正在不斷發展,優先考慮全面的產後支持。對創新治療的需求不斷成長,以及對早期診斷的日益關注,為該市場的發展創造了肥沃的土壤。政府、醫療保健組織和倡導團體正在齊心協力消除產後憂鬱症的恥辱感,使更多女性能夠尋求幫助。這些共同努力正在培養一個鼓勵創新、研究和投資突破性療法的市場環境。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 10億美元 |

| 預測值 | 23億美元 |

| 複合年成長率 | 9.2% |

近年來,人們對產後憂鬱症認知的轉變促進了該市場的快速發展。產後護理期間的常規篩檢已成為許多地區的標準做法,使醫療保健提供者能夠及早發現和治療產後憂鬱症。公共衛生運動正在強調母親心理健康的重要性,使女性更容易識別症狀並尋求治療。醫療保健基礎設施的改善,加上遠距醫療和數位健康解決方案的進步,增加了人們獲得醫療服務的機會,特別是對於醫療服務不足的人。隨著針對性治療的需求不斷上升,這些發展為持續的市場成長奠定了基礎。

產後憂鬱症治療市場根據相關情況進行細分,包括產後焦慮症、產後憂鬱症、產後創傷後壓力症候群 (PTSD)、產後強迫症 (OCD)、產後恐慌症和產後精神病。其中,產後焦慮佔比最大,2024 年為 23.5%。對母親心理健康的重視,加上醫療保健服務的增強,提高了診斷率和治療採用率。遠距醫療平台的日益普及進一步增強了人們獲得醫療服務的機會,確保有需要的人能夠及時介入。

在美國,2024 年產後憂鬱症治療市場價值為 3.707 億美元,預計到 2032 年複合年成長率為 8.9%。美國醫療保健體系擁有完善的基礎設施和支持性心理健康政策,在提高醫療可近性方面發揮關鍵作用。產後憂鬱症治療的保險覆蓋範圍進一步鼓勵了人們的採用,推動了全國市場的持續擴張。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 產後憂鬱症盛行率不斷上升

- 藥物開發的進展

- 人們對女性健康的認知和關注度不斷提高

- 產業陷阱與挑戰

- 相關副作用導致的安全性問題

- 產後憂鬱症藥物價格高昂

- 成長動力

- 成長潛力分析

- 未來趨勢

- 監管格局

- 管道分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 產後焦慮

- 產後憂鬱症

- 產後創傷後壓力症候群 (PTSD)

- 產後強迫症 (OCD)

- 產後恐慌症

- 產後精神病

第6章:市場估計與預測:依治療方式,2021 – 2034 年

- 主要趨勢

- 藥物治療

- 選擇性血清素再攝取抑制劑 (SSRI)

- 血清素去甲腎上腺素再攝取抑制劑 (SNRI)

- 三環抗憂鬱劑 (TCA)

- 其他藥物療法

- 荷爾蒙治療

- 其他治療

第 7 章:市場估計與預測:按管理路線,2021 年至 2034 年

- 主要趨勢

- 口服

- 腸外

- 其他給藥途徑

第 8 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 醫院藥房

- 零售藥局

- 網路藥局

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Bausch Health Companies

- Biogen

- Cipla

- Eli Lilly and Company

- GSK

- Merck

- Novartis

- Pfizer

- Sage Therapeutics

- Teva Pharmaceutical Industries

The Global Postpartum Depression Treatment Market reached USD 1 billion in 2024 and is anticipated to expand at a robust CAGR of 9.2% between 2025 and 2034. This rapid growth reflects increasing awareness of maternal mental health and the critical need for effective interventions. Postpartum depression, affecting a significant percentage of new mothers globally, has been thrust into the spotlight as a public health concern.

As mental health becomes a central component of maternal care, healthcare systems worldwide are evolving to prioritize comprehensive postpartum support. The rise in demand for innovative treatments, alongside the growing focus on early diagnosis, has created fertile ground for advancements in this market. Governments, healthcare organizations, and advocacy groups are working in tandem to destigmatize postpartum depression, enabling more women to seek help. These collective efforts are fostering a market environment that encourages innovation, research, and investment in groundbreaking therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 9.2% |

In recent years, a paradigm shift in how postpartum depression is perceived has contributed to this market's rapid development. Routine screening during postnatal care has become standard practice in many regions, allowing healthcare providers to identify and address postpartum depression early. Public health campaigns are shedding light on the importance of maternal mental well-being, making it easier for women to recognize symptoms and seek treatment. Improved healthcare infrastructure, coupled with advancements in telemedicine and digital health solutions, has increased access to care, especially for underserved populations. These developments have laid the foundation for sustained market growth as the demand for targeted treatments continues to rise.

The postpartum depression treatment market is segmented based on associated conditions, including postpartum anxiety, postpartum blues, postpartum post-traumatic stress disorder (PTSD), postpartum obsessive-compulsive disorder (OCD), postpartum panic disorder, and postpartum psychosis. Among these, postpartum anxiety accounted for the largest share at 23.5% in 2024. This condition is highly prevalent among new mothers, driving demand for effective treatment options. The emphasis on maternal mental health, coupled with enhanced access to healthcare services, has improved diagnosis rates and treatment adoption. The growing popularity of telehealth platforms has further bolstered access to care, ensuring timely interventions for individuals in need.

In the United States, the postpartum depression treatment market was valued at USD 370.7 million in 2024, with projections indicating an 8.9% CAGR through 2032. Several factors fuel this growth, including the increasing prevalence of postpartum depression, greater public awareness of maternal mental health, and the availability of cutting-edge therapies. The U.S. healthcare system, with its established infrastructure and supportive mental health policies, plays a pivotal role in enhancing accessibility. Insurance coverage for postpartum depression treatments has further encouraged adoption, driving continued market expansion across the country.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of postpartum depression

- 3.2.1.2 Advancements in drug development

- 3.2.1.3 Growing awareness and focus on women's health

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Safety concerns due to associated side effects

- 3.2.2.2 High cost of postpartum depression drugs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future trends

- 3.5 Regulatory landscape

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Postpartum anxiety

- 5.3 Postpartum blues

- 5.4 Postpartum post-traumatic stress disorder (PTSD)

- 5.5 Postpartum obsessive-compulsive disorder (OCD)

- 5.6 Postpartum panic disorder

- 5.7 Postpartum psychosis

Chapter 6 Market Estimates and Forecast, By Treatment, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pharmacotherapy

- 6.2.1 Selective serotonin reuptake inhibitors (SSRIs)

- 6.2.2 Serotonin norepinephrine reuptake inhibitors (SNRIs)

- 6.2.3 Tricyclic antidepressants (TCA)

- 6.2.4 Other pharmacotherapies

- 6.3 Hormone therapy

- 6.4 Other treatments

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

- 7.4 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bausch Health Companies

- 10.2 Biogen

- 10.3 Cipla

- 10.4 Eli Lilly and Company

- 10.5 GSK

- 10.6 Merck

- 10.7 Novartis

- 10.8 Pfizer

- 10.9 Sage Therapeutics

- 10.10 Teva Pharmaceutical Industries

2025 年至 2033 年憂鬱症藥物市場報告(依藥物類別、疾病類型、藥物類型、配銷通路和地區分類)產後憂鬱症治療市場:依治療類型、分佈 - 2025-2030 年全球預測

2025 年至 2033 年憂鬱症藥物市場報告(依藥物類別、疾病類型、藥物類型、配銷通路和地區分類)產後憂鬱症治療市場:依治療類型、分佈 - 2025-2030 年全球預測 到 2030 年抗治療性憂鬱症市場預測:按治療方式、分銷管道、最終用戶和地區進行的全球分析

到 2030 年抗治療性憂鬱症市場預測:按治療方式、分銷管道、最終用戶和地區進行的全球分析 產後憂鬱症治療藥物的市場規模、佔有率和趨勢分析報告:按類型、治療、給藥途徑、分銷管道、地區和細分市場預測,2024-2030年抗治療性憂鬱症市場:依藥物類型、通路和地區分類

產後憂鬱症治療藥物的市場規模、佔有率和趨勢分析報告:按類型、治療、給藥途徑、分銷管道、地區和細分市場預測,2024-2030年抗治療性憂鬱症市場:依藥物類型、通路和地區分類 憂鬱症藥物市場 - 全球產業規模、佔有率、趨勢、機會和預測,按藥物類別、疾病類型、藥物類型、地區和競爭細分,2019-2029F

憂鬱症藥物市場 - 全球產業規模、佔有率、趨勢、機會和預測,按藥物類別、疾病類型、藥物類型、地區和競爭細分,2019-2029F 非藥物憂鬱症治療市場:現況分析與預測(2023-2030)憂鬱症治療藥物市場:依藥物類型、依適應症、依配銷通路、依地區

非藥物憂鬱症治療市場:現況分析與預測(2023-2030)憂鬱症治療藥物市場:依藥物類型、依適應症、依配銷通路、依地區