|

市場調查報告書

商品編碼

1684783

膜電極組裝市場機會、成長動力、產業趨勢分析及 2024 - 2032 年預測Membrane Electrode Assembly Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

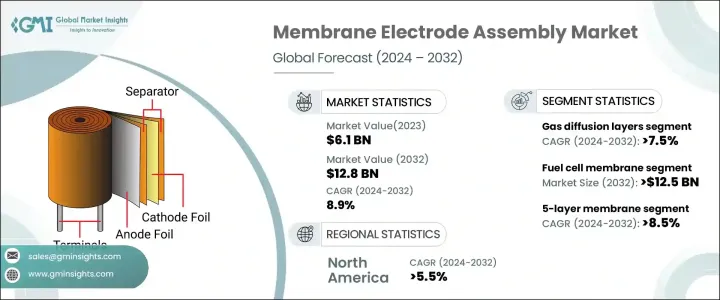

2023 年全球膜電極組件市場估值達 61 億美元,預計 2024 年至 2032 年期間複合年成長率為 8.9%。膜電極組件是燃料電池和其他電化學設備中的重要組成部分,在實現產生電能的化學反應中發揮關鍵作用。這些組件由質子傳導膜、陽極催化劑和陰極催化劑組成,它們共同作用以最大限度地提高能量轉換效率。人們對清潔能源解決方案,特別是基於氫的技術的日益關注,正在推動該市場顯著成長。

世界各國政府和私營部門正在大力投資再生能源項目,進一步推動燃料電池的普及。此外,燃料電池效率、耐用性和成本效益的進步也促進了膜電極組件設計的創新。各行業都優先考慮最佳化材料成分和製造程序,以提高性能並降低成本。燃料電池在汽車、固定式發電和攜帶式電子設備中的應用日益廣泛,進一步加速了對高品質膜電極組件的需求。隨著全球能源格局向永續性轉變,膜電極組件市場將在支持這一轉變中發揮關鍵作用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2023 |

| 預測年份 | 2024-2032 |

| 起始值 | 61億美元 |

| 預測值 | 128億美元 |

| 複合年成長率 | 8.9% |

到 2032 年,氣體擴散層部分預計將以 7.5% 的複合年成長率成長。持續的研究和開發努力正在推動材料性能的改進,從而提高效率和使用壽命。孔徑和分佈的調整可以最佳化反應物的品質傳輸和水的管理,從而提高燃料電池的整體性能。生產技術的創新也降低了成本,使得這些組件能夠得到更廣泛的應用。由於產業專注於開發高性能、長壽命的燃料電池,氣體擴散層的進步預計將顯著影響市場成長。

預計到 2032 年,五層膜電極組件市場將以 8.5% 的複合年成長率擴張。對燃料電池耐用性和可靠性的日益重視正在加速這些組件的採用。針對特定應用而最佳化的客製化系統設計正在促進市場擴張,而持續的技術進步則不斷完善燃料電池堆。雙極板和氣體擴散層等關鍵部件的創新正在加強行業趨勢並確保燃料電池性能的持續進步。這些發展使製造商能夠滿足對高效、可靠的燃料電池解決方案日益成長的需求。

預計到 2032 年,北美膜電極組件市場將以 5.5% 的複合年成長率成長。政府的支持性政策和財政激勵措施在促進燃料電池技術的應用方面發揮著至關重要的作用。旨在擴大氫基礎設施和鼓勵購買燃料電池汽車的策略性舉措正在推動市場成長。汽車製造商、研究機構和政府機構之間的合作正在促進技術進步並加速產業採用。這些合作對於擴大生產、提高效率和降低成本至關重要,確保未來幾年市場穩定成長。

目錄

第 1 章:方法論與範圍

- 市場定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 未付費來源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商矩陣

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 新冠肺炎對產業前景的影響

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 戰略儀表板

- 創新與永續發展格局

第5章:市場規模及預測:依組件分類,2019 – 2032 年

- 主要趨勢

- 膜

- 氣體擴散層

- 墊圈

- 其他

第 6 章:市場規模與預測:按應用,2019 – 2032 年

- 主要趨勢

- 燃料電池

- 電解器

第 7 章:市場規模與預測:依產品類型,2019 – 2032 年

- 主要趨勢

- 3 層

- 5 層

- 7 層

第 8 章:市場規模與預測:按地區,2019 – 2032 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 奧地利

- 西班牙

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 秘魯

- 墨西哥

第9章:公司簡介

- Ballard Power Systems

- WL Gore & Associates, Inc.

- Danish Power Systems

- BASF SE

- Giner Inc.

- IRD Fuel cells

- Greenerity GmbH

- Plug Power Inc.

- HyPlat Pty Ltd.

- Cummins Inc.

- FuelCell Energy, Inc.

- TOSHIBA CORPORATION

- Pansonic Holdings Corporation

- Dupont

- Johnson Matthey

- 3M

- EC21 Inc.

- Yangtze Energy Technologies, Inc

- YuanBo Engineering Co., Ltd.

- Ion Power, Inc.

The Global Membrane Electrode Assembly Market reached a valuation of USD 6.1 billion in 2023 and is expected to grow at a CAGR of 8.9% from 2024 to 2032. Membrane electrode assemblies, essential components in fuel cells and other electrochemical devices, play a pivotal role in enabling chemical reactions that generate electricity. These assemblies consist of a proton-conducting membrane, an anode catalyst, and a cathode catalyst, all working together to maximize energy conversion efficiency. The increasing focus on clean energy solutions, particularly in hydrogen-based technologies, is driving significant growth in this market.

Governments and private sectors worldwide are investing heavily in renewable energy initiatives, further boosting the adoption of fuel cells. Additionally, advancements in fuel cell efficiency, durability, and cost-effectiveness are fostering innovation in membrane electrode assembly designs. Industries are prioritizing the optimization of material compositions and manufacturing processes to enhance performance while reducing costs. The growing application of fuel cells in automotive, stationary power generation, and portable electronics is further accelerating the demand for high-quality membrane electrode assemblies. As the global energy landscape shifts toward sustainability, the membrane electrode assembly market is poised to play a critical role in supporting this transition.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $6.1 Billion |

| Forecast Value | $12.8 Billion |

| CAGR | 8.9% |

The gas diffusion layers segment is projected to grow at a CAGR of 7.5% through 2032. Continuous research and development efforts are driving improvements in material properties, enhancing both efficiency and longevity. Adjustments in pore size and distribution are optimizing reactant mass transport and water management, leading to better overall fuel cell performance. Innovations in production techniques are also reducing costs, making these assemblies more accessible for a broader range of applications. As the industry focuses on developing high-performance, long-lasting fuel cells, advancements in gas diffusion layers are expected to significantly influence market growth.

The 5-layer membrane electrode assembly segment is anticipated to expand at a CAGR of 8.5% through 2032. The rising emphasis on fuel cell durability and reliability is accelerating the adoption of these assemblies. Tailored system designs optimized for specific applications are contributing to market expansion, while ongoing technological advancements are refining fuel cell stacks. Innovations in key components, such as bipolar plates and gas diffusion layers, are strengthening industry trends and ensuring consistent progress in fuel cell performance. These developments are enabling manufacturers to meet the growing demand for efficient and reliable fuel cell solutions.

North America membrane electrode assembly market is forecasted to grow at a CAGR of 5.5% through 2032. Supportive government policies and financial incentives are playing a crucial role in promoting the adoption of fuel cell technologies. Strategic initiatives aimed at expanding hydrogen infrastructure and encouraging the purchase of fuel cell vehicles are driving market growth. Collaborations among automakers, research institutions, and government agencies are fostering technological advancements and accelerating industry adoption. These partnerships are essential for scaling production, improving efficiency, and reducing costs, ensuring steady market growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Unpaid sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2019 – 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Vendor matrix

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 COVID- 19 impact on the industry outlook

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2023

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2019 – 2032 (USD Million)

- 5.1 Key trends

- 5.2 Membranes

- 5.3 Gas diffusion layers

- 5.4 Gaskets

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2019 – 2032 (USD Million)

- 6.1 Key trends

- 6.2 Fuel cells

- 6.3 Electrolyzer

Chapter 7 Market Size and Forecast, By Product Type, 2019 – 2032 (USD Million)

- 7.1 Key trends

- 7.2 3-layer

- 7.3 5-layer

- 7.4 7-layer

Chapter 8 Market Size and Forecast, By Region, 2019 – 2032 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Austria

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Peru

- 8.6.3 Mexico

Chapter 9 Company Profiles

- 9.1 Ballard Power Systems

- 9.2 W. L. Gore & Associates, Inc.

- 9.3 Danish Power Systems

- 9.4 BASF SE

- 9.5 Giner Inc.

- 9.6 IRD Fuel cells

- 9.7 Greenerity GmbH

- 9.8 Plug Power Inc.

- 9.9 HyPlat Pty Ltd.

- 9.10 Cummins Inc.

- 9.11 FuelCell Energy, Inc.

- 9.12 TOSHIBA CORPORATION

- 9.13 Pansonic Holdings Corporation

- 9.14 Dupont

- 9.15 Johnson Matthey

- 9.16 3M

- 9.17 EC21 Inc.

- 9.18 Yangtze Energy Technologies, Inc

- 9.19 YuanBo Engineering Co., Ltd.

- 9.20 Ion Power, Inc.