|

市場調查報告書

商品編碼

1684787

低速汽車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Low Speed Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

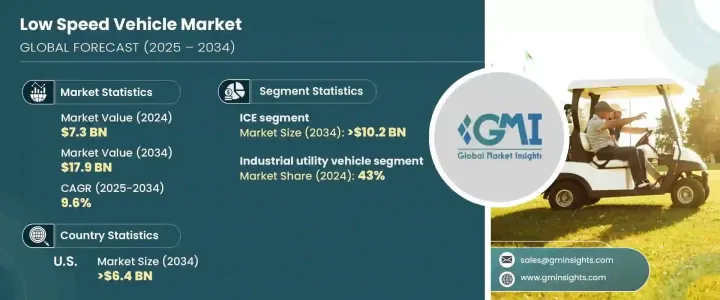

2024 年全球低速汽車市場價值為 73 億美元,預計 2025 年至 2034 年期間複合年成長率將達到 9.6%。隨著都市化進程不斷加速,城市面臨交通擁擠、污染和噪音過大等日益嚴重的挑戰。這迫切需要更有效率、更環保的交通選擇,進而推動低速汽車的普及。這些車輛已成為越來越受歡迎的短途旅行解決方案,尤其是在人口密集的城市地區、私人社區和商業空間。

隨著對更清潔的行動解決方案的追求,低速汽車因其永續性、成本效益以及在擁擠地區無縫導航的能力而越來越受到青睞。隨著電池技術的進步,這些車輛的效率更高、使用壽命更長、充電時間更快、能量密度更高,它們正成為個人和商業用途更具吸引力的選擇。電動替代品的日益普及,加上政府的激勵措施和基礎設施投資的增加,正在塑造這個市場的發展軌跡。此外,低速車輛在最後一哩配送、工業營運和設施內運輸中的作用不斷擴大,反映了向永續城市交通解決方案的更廣泛趨勢。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 73億美元 |

| 預測值 | 179億美元 |

| 複合年成長率 | 9.6% |

從推進類型來看,市場分為兩個主要部分:內燃機(ICE)和電動車。 2024 年,內燃機驅動的低速車佔據領先地位,佔有 61% 的市場佔有率,預計到 2034 年將創造 102 億美元的市場價值。內燃機汽車經久不衰的受歡迎程度可以歸因於其價格實惠、可靠性以及現有的加油基礎設施。與電動車相比,內燃機汽車的前期成本通常較低,因為它們不需要昂貴的電池系統。此外,其更大的續航里程和快速加油能力使其成為需要不間斷性能的用戶的理想選擇。在電動車充電網路有限的地區,內燃機驅動的低速車尤其受到青睞,這確保了它們在偏遠或低度開發地區仍然是一種可行的選擇。

工業多功能車類別是低速汽車市場的主要細分市場,到 2024 年將佔 43% 的佔有率。這些車輛對於提高各行業的營運效率至關重要。它們體積小、耐用,可以在狹小空間內輕鬆移動,執行艱鉅的任務,是物料運輸、設施管理和物流領域不可或缺的一部分。隨著企業不斷精簡營運,工業多功能車的採用率預計將上升,進一步推動其在市場上的主導地位。

在美國,低速汽車佔據主導地位,2024 年佔 94% 的市場佔有率,預計到 2034 年將達到 64 億美元。這一成長得益於該國強大的基礎設施和對永續移動解決方案日益成長的需求。美國長期以來一直有著將低速汽車用於娛樂和商業用途的文化,這支持了其廣泛應用。隨著永續發展措施不斷獲得關注,在技術進步和消費者偏好不斷變化的推動下,市場可望穩步擴張。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 技術提供者

- 零件供應商

- 原始設備製造商

- 最終用戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 都市化和對環保交通的需求不斷成長

- 電動車 (EV) 技術的進步

- 政府激勵和監管支持

- 旅遊和休閒活動需求不斷成長

- 產業陷阱與挑戰

- 範圍有限和速度限制

- 電動車的初始成本較高

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 高爾夫球車

- 商用多用途車

- 工業多用途車

- 個人代步車

第 6 章:市場估計與預測:按推進方式,2021 - 2034 年

- 主要趨勢

- 冰

- 電的

第 7 章:市場估計與預測:按應用 2021 - 2034

- 主要趨勢

- 高爾夫球場

- 飯店及度假村

- 機場

- 工業設施

- 其他

第 8 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第9章:公司簡介

- AGT Electric Cars.

- American Landmaster

- Bradshaw EV

- CLUB CAR

- Columbia Vehicle Group Inc.

- Deere & Company

- EVolution Electric Vehicles

- Garia

- ICON Electric Vehicles

- KUBOTA Corporation.

- Moto Electric Vehicles

- Motrec International Inc.

- Star EV Corporation

- Stealth

- Suzhou Eagle Electric Vehicle Manufacturing Co., Ltd

- Textron Inc.

- The Toro Company

- Waev Inc.

- Yamaha Motor Co., Ltd.

The Global Low Speed Vehicle Market was valued at USD 7.3 billion in 2024 and is forecasted to grow at an impressive CAGR of 9.6% from 2025 to 2034. As urbanization continues to accelerate, cities are facing escalating challenges such as traffic congestion, pollution, and excessive noise. This has created an urgent demand for more efficient, eco-friendly transportation options, which is driving the adoption of low-speed vehicles. These vehicles have become an increasingly popular solution for short-distance travel, especially in densely populated urban areas, private communities, and commercial spaces.

With the push for cleaner mobility solutions, low-speed vehicles are gaining traction due to their sustainability, cost-effectiveness, and ability to navigate congested areas seamlessly. As advancements in battery technology make these vehicles more efficient, with longer lifespans, faster charging times, and improved energy density, they are becoming an even more attractive choice for both personal and commercial use. The growing popularity of electric alternatives, alongside government incentives and increasing investments in infrastructure, is shaping the trajectory of this market. Furthermore, the role of low-speed vehicles in last-mile delivery, industrial operations, and intra-facility transport continues to expand, reflecting the broader movement toward sustainable urban mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $17.9 Billion |

| CAGR | 9.6% |

When looking at the propulsion types, the market is divided into two key segments: internal combustion engine (ICE) and electric variants. In 2024, internal combustion engine-powered low-speed vehicles took the lead with a 61% market share, and they are expected to generate USD 10.2 billion by 2034. The enduring popularity of ICE variants can be attributed to their affordability, reliability, and the existing infrastructure for fueling. ICE vehicles typically have a lower upfront cost compared to their electric counterparts, as they do not require expensive battery systems. Additionally, their extended range and quick refueling capabilities make them an appealing choice for users who need uninterrupted performance. ICE-powered low-speed vehicles are especially favored in regions with limited access to electric charging networks, ensuring they remain a viable option in remote or less developed areas.

The industrial utility vehicle category is a major segment in the low-speed vehicle market, holding a 43% share in 2024. These vehicles are crucial in enhancing operational efficiency across various industries. Their compact size and durability allow them to maneuver easily through tight spaces while performing demanding tasks, making them indispensable for material transportation, facility management, and logistics. As businesses continue to streamline operations, the adoption of industrial utility vehicles is expected to rise, further driving their dominance in the market.

In the U.S., low-speed vehicles dominate, accounting for 94% of the market share in 2024, with expectations to reach USD 6.4 billion by 2034. This growth is fueled by the country's robust infrastructure and an increasing demand for sustainable mobility solutions. The U.S. has a long-established culture of both recreational and commercial use of low-speed vehicles, which supports their widespread adoption. As sustainability initiatives continue to gain traction, the market is poised for steady expansion, driven by technological advancements and evolving consumer preferences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 OEMs

- 3.1.4 End user

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Urbanization and increasing demand for eco-friendly transportation

- 3.7.1.2 Advancements in electric vehicle (EV) technology

- 3.7.1.3 Government incentives and regulatory support

- 3.7.1.4 Rising demand in tourism and recreational activities

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Limited range and speed constraints

- 3.7.2.2 High initial cost of electric variants

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Golf cart

- 5.3 Commercial utility vehicle

- 5.4 Industrial utility vehicle

- 5.5 Personal mobility vehicle

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Application 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Golf courses

- 7.3 Hotels & resorts

- 7.4 Airports

- 7.5 Industrial facilities

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 AGT Electric Cars.

- 9.2 American Landmaster

- 9.3 Bradshaw EV

- 9.4 CLUB CAR

- 9.5 Columbia Vehicle Group Inc.

- 9.6 Deere & Company

- 9.7 EVolution Electric Vehicles

- 9.8 Garia

- 9.9 ICON Electric Vehicles

- 9.10 KUBOTA Corporation.

- 9.11 Moto Electric Vehicles

- 9.12 Motrec International Inc.

- 9.13 Star EV Corporation

- 9.14 Stealth

- 9.15 Suzhou Eagle Electric Vehicle Manufacturing Co., Ltd

- 9.16 Textron Inc.

- 9.17 The Toro Company

- 9.18 Waev Inc.

- 9.19 Yamaha Motor Co., Ltd.

低速車輛(LSV)全球市場報告2025年

低速車輛(LSV)全球市場報告2025年 低速車輛(LSV)的全球市場的評估:各車輛類型,各用途,不同速度,推動因素,各地區,機會,預測(2018年~2032年)低速車輛市場 - 全球產業規模、佔有率、趨勢、機會和預測,按推進類型、車輛類型、應用、地區和競爭細分,2019-2029F

低速車輛(LSV)的全球市場的評估:各車輛類型,各用途,不同速度,推動因素,各地區,機會,預測(2018年~2032年)低速車輛市場 - 全球產業規模、佔有率、趨勢、機會和預測,按推進類型、車輛類型、應用、地區和競爭細分,2019-2029F 到 2030 年低速汽車市場預測:按類型、動力來源、輸出、電池類型、座椅數量、應用、最終用戶和地區進行的全球分析

到 2030 年低速汽車市場預測:按類型、動力來源、輸出、電池類型、座椅數量、應用、最終用戶和地區進行的全球分析 低速車輛市場:按車輛、推進、動力、應用分類 - 2025-2030 年全球預測低速汽車市場:按車型、速度、應用和地區分類

低速車輛市場:按車輛、推進、動力、應用分類 - 2025-2030 年全球預測低速汽車市場:按車型、速度、應用和地區分類 全球低速汽車市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測

全球低速汽車市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測 全球低速車輛市場:按車型、功率、馬達類型和配置、推進部分、電池類型、應用、類別、電壓 - 預測(至 2030 年)低速車的全球市場:輸出·推動區分·用途·各地區 (~2030年)全球低速車輛 (LSV) 市場:到 2033 年的機會與策略

全球低速車輛市場:按車型、功率、馬達類型和配置、推進部分、電池類型、應用、類別、電壓 - 預測(至 2030 年)低速車的全球市場:輸出·推動區分·用途·各地區 (~2030年)全球低速車輛 (LSV) 市場:到 2033 年的機會與策略