|

市場調查報告書

商品編碼

1684798

加密軟體市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Encryption Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

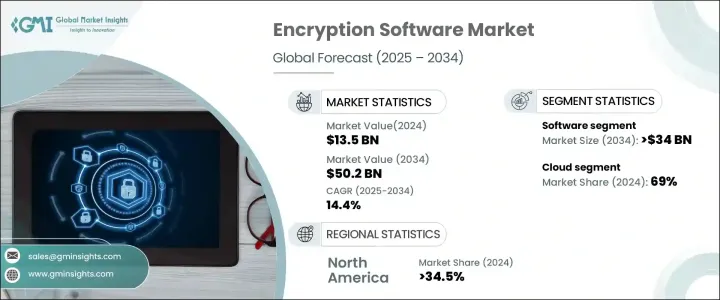

2024 年全球加密軟體市場價值為 135 億美元,預計 2025 年至 2034 年期間的複合年成長率為 14.4%。隨著全球企業面臨日益嚴重的網路威脅、資料外洩和更嚴格的合規法規,對強大加密解決方案的需求持續上升。各行各業的組織都優先使用加密軟體來保護敏感資料、降低網路安全風險並滿足不斷變化的監管要求。隨著技術的快速進步,加密軟體現在更加複雜,利用人工智慧、區塊鏈和量子加密來提供下一代安全解決方案。

人工智慧驅動的加密正在透過不斷適應新威脅和改進即時風險檢測來重新定義資料保護。同時,基於區塊鏈的加密透過確保防篡改資料傳輸來增強安全性,使其成為金融交易、醫療記錄和政府通訊的理想選擇。量子加密雖然仍處於早期階段,但它利用量子力學原理來防止未經授權的訪問,並有望實現前所未有的資料安全水平。隨著數位轉型的加速,企業正在大力投資加密技術,以維護信任、保護智慧財產權和保護關鍵基礎設施。雲端運算、物聯網 (IoT) 設備和遠端勞動力的迅猛成長進一步凸顯了保護分散式網路中資料的高級加密解決方案的必要性。市場的上升趨勢反映了全球對更強大的網路安全框架的推動,企業和政府都認知到加密是抵禦網路威脅的重要防御手段。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 135億美元 |

| 預測值 | 502億美元 |

| 複合年成長率 | 14.4% |

軟體產業在 2024 年佔據了 70% 的市場佔有率,預計到 2034 年將創造 340 億美元的市場價值。企業繼續青睞加密軟體,因為它能夠保護各種網路、儲存系統和數位平台上的敏感資訊。網路攻擊的激增增加了企業部署保護結構化和非結構化資料的尖端加密工具的必要性。金融、醫療保健和零售等行業依靠加密軟體來遵守嚴格的資料保護法,同時確保客戶和內部營運的無縫安全。

2024 年,雲端部署佔據了加密軟體市場佔有率的 69%,反映了向基於雲端的資料儲存和運算的廣泛轉變。企業擴大將業務遷移到雲端,需要強大的加密措施來保護敏感資訊免受網路威脅和未經授權的存取。雲端原生加密解決方案可確保資料在儲存和傳輸過程中的安全,解決了人們對資料完整性、合規性和存取控制日益成長的擔憂。企業意識到加密在維護 GDPR、CCPA 和 HIPAA 等框架的監管合規性方面發揮關鍵作用,從而增加了對先進雲端安全解決方案的投資。

2024 年,北美佔據加密軟體市場的 34.5%,成為網路安全創新的重要中心。憑藉完善的技術基礎設施和嚴格的資料隱私法規,該地區的企業積極將加密軟體整合到其安全策略中。金融部門、醫療保健產業和政府機構優先考慮加密,以保護高價值資產、防止資料外洩並確保交易安全。人們對網路安全風險的認知不斷增強,加上對數位轉型的投資不斷增加,繼續推動市場擴張。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 雲端服務供應商

- 託管安全服務提供者

- 加密軟體整合商

- 最終用戶

- 利潤率分析

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 資料安全疑慮加劇

- 資料量不斷增加

- 雲端服務的激增

- 加密技術的創新

- 產業陷阱與挑戰

- 實施的複雜性與成本

- 與現有系統的整合挑戰

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 軟體

- 端點加密

- 電子郵件加密

- 雲端加密

- 磁碟加密

- 資料庫加密

- 其他

- 服務

- 培訓與諮詢

- 整合與維護

- 託管服務

第6章:市場估計與預測:依部署模型,2021 - 2034 年

- 主要趨勢

- 本地

- 雲

第 7 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 資訊科技和電信

- 金融保險業協會

- 衛生保健

- 零售

- 政府和公共部門

- 製造業

- 其他

第 8 章:市場估計與預測:按企業規模,2021 - 2034 年

- 主要趨勢

- 中小企業

- 大型企業

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- AO Kaspersky Lab

- Bitdefender

- Broadcom

- Check Point Software

- Cisco Systems

- Dell Technologies

- ESET

- F-Secure

- HPE

- IBM

- McAfee

- Microsoft

- OpenText

- Oracle

- Palo Alto

- Panda Security

- Proofpoint

- Sophos Ltd.

- Thales

- Trend Micro

The Global Encryption Software Market, valued at USD 13.5 billion in 2024, is on track to grow at a CAGR of 14.4% between 2025 and 2034. As businesses worldwide face increasing cyber threats, data breaches, and stricter compliance regulations, the demand for robust encryption solutions continues to rise. Organizations across industries prioritize encryption software to safeguard sensitive data, mitigate cybersecurity risks, and meet evolving regulatory requirements. With rapid technological advancements, encryption software is now more sophisticated, leveraging artificial intelligence, blockchain, and quantum encryption to provide next-generation security solutions.

AI-driven encryption is redefining data protection by continuously adapting to new threats and improving real-time risk detection. Meanwhile, blockchain-based encryption enhances security by ensuring tamper-proof data transfers, making it ideal for financial transactions, healthcare records, and government communications. Quantum encryption, though still in its early stages, promises an unprecedented level of data security by leveraging the principles of quantum mechanics to prevent unauthorized access. As digital transformation accelerates, enterprises are investing heavily in encryption technologies to maintain trust, protect intellectual property, and secure critical infrastructure. The exponential growth of cloud computing, Internet of Things (IoT) devices, and remote workforces further underscores the necessity for advanced encryption solutions that protect data across distributed networks. The market's upward trajectory reflects a global push for stronger cybersecurity frameworks, with businesses and governments alike recognizing encryption as an essential defense against cyber threats.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.5 Billion |

| Forecast Value | $50.2 Billion |

| CAGR | 14.4% |

The software segment, which accounted for 70% of the market share in 2024, is set to generate USD 34 billion by 2034. Companies continue to favor encryption software due to its ability to secure sensitive information across various networks, storage systems, and digital platforms. The surge in cyberattacks has heightened the need for businesses to deploy cutting-edge encryption tools that protect both structured and unstructured data. Industries such as finance, healthcare, and retail rely on encryption software to comply with stringent data protection laws while ensuring seamless security for their customers and internal operations.

Cloud deployment accounted for 69% of the encryption software market share in 2024, reflecting the widespread shift toward cloud-based data storage and computing. Businesses increasingly migrate their operations to the cloud, necessitating strong encryption measures to protect sensitive information from cyber threats and unauthorized access. Cloud-native encryption solutions ensure data remains secure both in storage and in transit, addressing growing concerns over data integrity, compliance, and access control. Enterprises recognize the critical role encryption plays in maintaining regulatory compliance with frameworks such as GDPR, CCPA, and HIPAA, leading to increased investment in advanced cloud security solutions.

North America held a 34.5% share of the encryption software market in 2024, establishing itself as a key hub for cybersecurity innovation. With a well-developed technological infrastructure and stringent data privacy regulations, businesses in the region actively integrate encryption software into their security strategies. The financial sector, healthcare industry, and government institutions prioritize encryption to protect high-value assets, prevent data breaches, and ensure secure transactions. Growing awareness of cybersecurity risks, coupled with increasing investments in digital transformation, continues to drive market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Cloud service providers

- 3.2.2 Managed security service providers

- 3.2.3 Encryption software integrators

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising data security concerns

- 3.7.1.2 Increasing data volume

- 3.7.1.3 Proliferation of cloud services

- 3.7.1.4 Innovations in encryption technologies

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Complexity and cost of implementation

- 3.7.2.2 Integration challenges with existing systems

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Endpoint encryption

- 5.2.2 Email encryption

- 5.2.3 Cloud encryption

- 5.2.4 Disk encryption

- 5.2.5 Database encryption

- 5.2.6 Others

- 5.3 Services

- 5.3.1 Training & consulting

- 5.3.2 Integration & maintenance

- 5.3.3 Managed service

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 IT & telecom

- 7.3 BFSI

- 7.4 Healthcare

- 7.5 Retail

- 7.6 Government & public sector

- 7.7 Manufacturing

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AO Kaspersky Lab

- 10.2 Bitdefender

- 10.3 Broadcom

- 10.4 Check Point Software

- 10.5 Cisco Systems

- 10.6 Dell Technologies

- 10.7 ESET

- 10.8 F-Secure

- 10.9 HPE

- 10.10 IBM

- 10.11 McAfee

- 10.12 Microsoft

- 10.13 OpenText

- 10.14 Oracle

- 10.15 Palo Alto

- 10.16 Panda Security

- 10.17 Proofpoint

- 10.18 Sophos Ltd.

- 10.19 Thales

- 10.20 Trend Micro

加密即服務市場按服務類型、組織規模、部署類型和最終用戶分類 - 2025-2030 年全球預測

加密即服務市場按服務類型、組織規模、部署類型和最終用戶分類 - 2025-2030 年全球預測 2025年全球資料加密市場報告2025年全球電子郵件加密市場報告2025 年至 2033 年電子郵件加密市場報告(按加密類型、部署類型、組件、最終用戶、組織規模和地區分類)

2025年全球資料加密市場報告2025年全球電子郵件加密市場報告2025 年至 2033 年電子郵件加密市場報告(按加密類型、部署類型、組件、最終用戶、組織規模和地區分類) 加密貨幣即服務市場按服務類型、組織規模、垂直行業和地區分類 - 預測至 2030 年

加密貨幣即服務市場按服務類型、組織規模、垂直行業和地區分類 - 預測至 2030 年 全球 EaaS(加密即服務)市場:市場規模、佔有率、趨勢、產業分析(依服務類型、組織規模、產業和地區)、未來預測(2025-2034年)2025 年全球加密軟體市場報告

全球 EaaS(加密即服務)市場:市場規模、佔有率、趨勢、產業分析(依服務類型、組織規模、產業和地區)、未來預測(2025-2034年)2025 年全球加密軟體市場報告 加密軟體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)行動加密:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)加密軟體市場評估:零組件·展開·用途·組織規模·終端用戶·各地區的機會及預測 (2018-2032年)

加密軟體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)行動加密:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)加密軟體市場評估:零組件·展開·用途·組織規模·終端用戶·各地區的機會及預測 (2018-2032年)