|

市場調查報告書

商品編碼

1684869

肺支架市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Lung Stent Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

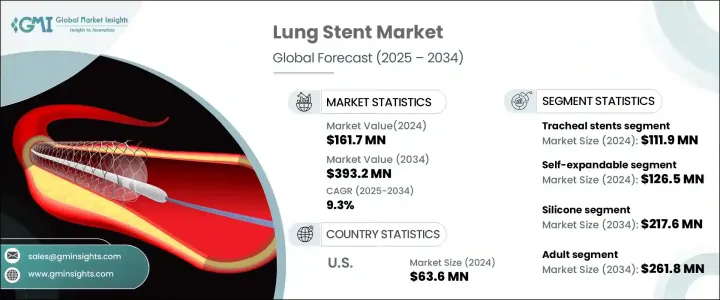

2024 年全球肺支架市場價值為 1.617 億美元,預計 2025 年至 2034 年期間將實現 9.3% 的強勁成長率。市場快速擴張可歸因於多種因素,包括慢性呼吸系統疾病盛行率上升、微創手術的進步以及旨在開發創新醫療技術的投資激增。由於空氣污染、吸煙和久坐的生活方式等因素,呼吸系統疾病變得越來越普遍。這些情況導致對肺支架的需求增加,因為它們對於因腫瘤、感染或先天性異常引起阻塞的患者維持氣道通暢和改善呼吸方面發揮著至關重要的作用。

肺支架因其透過提供有效的氣道管理解決方案來改善患者治療效果的能力而越來越受到認可。隨著醫療保健系統的發展,人們越來越傾向於採用微創治療,因為這種治療可以縮短恢復時間、減少併發症並降低醫療成本。技術進步使得肺支架能夠更適應各種氣道解剖結構,人工智慧驅動的成像和導航系統的整合進一步提高了支架放置的精準度。這種技術整合為更好的治療效果和成功率鋪平了道路。此外,全球人口老化更容易患上呼吸系統疾病,從而增加對此類醫療設備的需求。政府支持先進呼吸照護的舉措和優惠的報銷政策也推動了市場的成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1.617 億美元 |

| 預測值 | 3.932億美元 |

| 複合年成長率 | 9.3% |

肺支架市場分為三種產品類型:氣管支架、支氣管支架和喉支架。氣管支架領域在 2024 年以 1.119 億美元的市場規模領先。氣管支架在治療嚴重氣道阻塞方面已被廣泛應用,成為醫療保健提供者中最受歡迎的選擇。這些支架可以在出現嚴重呼吸道阻塞的情況下立即緩解症狀,確保氣流不間斷,並顯著降低併發症的風險。因此,氣管支架通常用於緊急手術和計劃手術。

設備類型細分包括自膨脹支架和球囊膨脹支架。自膨脹支架領域在 2024 年創造了 1.265 億美元的收入,預計在 2025 年至 2034 年期間的複合年成長率為 9.4%。這些支架因其易於部署且能夠適應複雜的氣道結構而受到青睞。放置後,自膨脹支架會自動膨脹,從而縮短手術時間並確保準確定位。它們的可靠性和效率使得它們在快速恢復氣流至關重要的緊急情況下特別有價值。

在美國,肺支架市場在 2024 年達到 6,360 萬美元,預計到 2034 年將以 8.8% 的複合年成長率成長。由於美國擁有先進的醫療基礎設施、較高的肺部疾病發生率以及對微創治療的日益重視,美國將繼續主導全球市場。人工智慧成像等尖端技術的融合,提高了支架置入的精準度,進一步鞏固了中國在該領域的領先地位。政府的支持性政策和報銷框架也對美國市場的成長軌跡做出了重大貢獻。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 肺癌發生率上升

- 慢性阻塞性肺病和結核病後狹窄的發生率不斷上升

- 公共和私人組織加大對非血管支架開發的投資

- 呼吸系統疾病微創手術越來越受青睞

- 產業陷阱與挑戰

- 替代治療的可用性

- 嚴格的規定

- 成長動力

- 成長潛力分析

- 2024 年定價分析

- 監管格局

- 報銷場景

- 技術格局

- 管道分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 氣管支架

- 支氣管支架

- 喉支架

第 6 章:市場估計與預測:按設備類型,2021 - 2034 年

- 主要趨勢

- 自膨脹式

- 球囊擴張型

第 7 章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 矽酮

- 金屬

- 不銹鋼

- 鎳鈦合金

- 混合

第 8 章:市場估計與預測:按患者,2021 - 2034 年

- 主要趨勢

- 成人

- 兒科

第 9 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用戶

第 10 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Boston Medical Products

- Boston Scientific

- HEALTH MICROPORT MEDICAL

- COOK GROUP

- EFER ENDOSCOPY

- HOOD LABORATORIES

- mi-TECH

- MERIT MEDICAL

- MICRO-TECH ENDOSCOPY

- NOVATECH

- STENING

- TaeWoong MEDICAL

- Teleflex

The Global Lung Stent Market, valued at USD 161.7 million in 2024, is projected to experience a robust growth rate of 9.3% CAGR from 2025 to 2034. This rapid market expansion can be attributed to several factors, including the rising prevalence of chronic respiratory diseases, advancements in minimally invasive procedures, and a surge in investments aimed at developing innovative medical technologies. Respiratory conditions are becoming more widespread, driven by factors like air pollution, smoking, and sedentary lifestyles. These conditions have led to an increased demand for lung stents, as they play a crucial role in maintaining airway patency and improving breathing for patients suffering from blockages caused by tumors, infections, or congenital abnormalities.

Lung stents are increasingly recognized for their ability to improve patient outcomes by offering effective solutions for airway management. As healthcare systems evolve, there is a growing shift toward minimally invasive treatments that provide quicker recovery times, reduced complications, and lower healthcare costs. Technological advancements have made lung stents more adaptable to various airway anatomies, and the integration of artificial intelligence-driven imaging and navigation systems has further enhanced the precision of stent placement. This technological integration is paving the way for better treatment outcomes and success rates. Additionally, the aging global population is more vulnerable to respiratory diseases, contributing to a higher demand for such medical devices. Government initiatives supporting advanced respiratory care and favorable reimbursement policies are also fueling the market's growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $161.7 Million |

| Forecast Value | $393.2 Million |

| CAGR | 9.3% |

The lung stent market is divided into three product types: tracheal, bronchial, and laryngeal stents. The tracheal stents segment led the market with USD 111.9 million in 2024. Their widespread use in treating severe airway obstructions has made them the most preferred choice among healthcare providers. These stents offer immediate relief in cases of critical respiratory blockages, ensuring uninterrupted airflow and significantly reducing the risk of complications. As a result, tracheal stents are commonly used in both emergency and planned procedures.

Device type segmentation includes self-expandable and balloon-expandable stents. The self-expandable stents segment generated USD 126.5 million in 2024 and is expected to grow at a CAGR of 9.4% between 2025 and 2034. These stents are favored for their ease of deployment and their ability to conform to complex airway structures. Upon placement, self-expandable stents automatically expand, cutting down procedural time and ensuring accurate positioning. Their reliability and efficiency make them especially valuable in emergency scenarios where quick restoration of airflow is critical.

In the U.S., the lung stent market reached USD 63.6 million in 2024 and is anticipated to grow at a CAGR of 8.8% through 2034. The U.S. continues to dominate the global market, thanks to its advanced healthcare infrastructure, high incidence of lung diseases, and increasing focus on minimally invasive treatments. The integration of cutting-edge technologies, such as AI-driven imaging, is improving the precision of stent placements, further bolstering the country's leading position in this sector. Supportive government policies and reimbursement frameworks are also contributing significantly to the U.S. market's growth trajectory.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of lung cancer

- 3.2.1.2 Growing incidence of COPD and post-tuberculosis stenosis

- 3.2.1.3 Increasing investments by the public and private organizations for the development of non-vascular stents

- 3.2.1.4 Growing preference for minimally invasive surgeries for respiratory disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative substitute treatment

- 3.2.2.2 Stringent regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.5 Regulatory landscape

- 3.6 Reimbursement scenario

- 3.7 Technology landscape

- 3.8 Pipeline analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Tracheal stents

- 5.3 Bronchial stents

- 5.4 Laryngeal stents

Chapter 6 Market Estimates and Forecast, By Device Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Self-expandable

- 6.3 Balloon-expandable

Chapter 7 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Silicone

- 7.3 Metal

- 7.3.1 Stainless steel

- 7.3.2 Nitinol

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Adult

- 8.3 Pediatric

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Boston Medical Products

- 11.2 Boston Scientific

- 11.3 HEALTH MICROPORT MEDICAL

- 11.4 COOK GROUP

- 11.5 EFER ENDOSCOPY

- 11.6 HOOD LABORATORIES

- 11.7 mi-TECH

- 11.8 MERIT MEDICAL

- 11.9 MICRO-TECH ENDOSCOPY

- 11.10 NOVATECH

- 11.11 STENING

- 11.12 TaeWoong MEDICAL

- 11.13 Teleflex

2025年全球氣道支架市場報告

2025年全球氣道支架市場報告 全球肺支架市場 - 2025 至 2033 年

全球肺支架市場 - 2025 至 2033 年 肺支架市場:按產品、最終用戶分類 - 2025-2030 年全球預測氣道支架市場:按產品類型、應用、材料、最終用戶分類 - 全球預測 2025-2030

肺支架市場:按產品、最終用戶分類 - 2025-2030 年全球預測氣道支架市場:按產品類型、應用、材料、最終用戶分類 - 全球預測 2025-2030 呼吸道支架/肺支架的全球市場規模:各產品,各用途,各地區,範圍及預測全球氣道/肺支架市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測氣道支架 - 全球市場回顧、競爭格局、市場預測 (2030)

呼吸道支架/肺支架的全球市場規模:各產品,各用途,各地區,範圍及預測全球氣道/肺支架市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測氣道支架 - 全球市場回顧、競爭格局、市場預測 (2030) 全球肺支架市場:按產品類型、按材料、按類型、按最終用戶、按地區

全球肺支架市場:按產品類型、按材料、按類型、按最終用戶、按地區 全球喉支架市場全球氣管支架市場

全球喉支架市場全球氣管支架市場