|

市場調查報告書

商品編碼

1685062

船用引擎市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測Marine Engines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

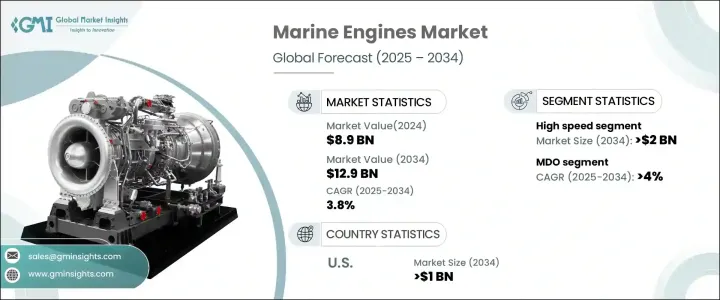

2024 年全球船用引擎市場價值為 89 億美元,預計 2025 年至 2034 年的複合年成長率為 3.8%。隨著全球貿易和運輸發生重大轉型,不斷變化的成本、供應鏈模型和物流框架正在重塑國際貿易格局。這些變化正在影響各國的競爭力,並使其進一步融入全球交通網路。貿易仍然是經濟發展的重要驅動力,推動了對更高效船用引擎的需求。港口基礎設施投資的不斷增加、船舶技術的快速進步以及海運量的不斷增加都是推動市場發展的因素。隨著人們對環境問題的關注度不斷上升,人們明顯轉向尋求環保解決方案,特別是在燃油效率和減少排放方面。隨著全球範圍內實施更加嚴格的法規,對永續船用引擎技術的關注正成為市場的主要驅動力。

預計到 2034 年,高速船用引擎的需求將達到 20 億美元。這一成長可歸因於港口設施的不斷發展以及對強力拖船的需求不斷增加。小型船舶、遊艇、渡輪和漁船尤其採用緊湊型引擎設計,不僅可以提高效率,還可以降低燃料消耗和營運成本。這些引擎不僅性能出色,而且有助於減少整體環境影響,使其成為各種船舶應用中極具吸引力的選擇。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 89億美元 |

| 預測值 | 129億美元 |

| 複合年成長率 | 3.8% |

另一方面,到 2034 年,MDO(船用柴油)船用引擎領域的複合年成長率將達到 4%。這些引擎因其效率高、能夠保持高速運轉同時保持低噪音水平的能力而越來越受歡迎。它們的四衝程引擎設計透過每隔一個循環消耗燃料來提高燃油效率,這一特點使它們有別於每次衝程都消耗燃料的二衝程引擎。此外,MDO 引擎不需要注入油或潤滑油,從而減少排放,更環保,符合日益嚴格的環境法規。

美國船用引擎市場也正在經歷長足的擴張,預計到 2034 年將創造 10 億美元的產值。隨著製造商不斷創新以獲得更好的性能,柴油引擎技術的進步在推動需求方面發揮著重要作用。經濟成長、對可靠引擎性能的日益關注以及對豪華和舒適功能的投資增加是這項擴張的主要推動力。此外,海上運輸的持續成長將長期需要更先進、更有效率的船用引擎。這種多方面的發展反映了美國市場的持續成長軌跡

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 市場估計和預測參數

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第 5 章:市場規模及預測:依產品,2021 – 2034 年

- 主要趨勢

- 多學科行動

- 鎂合金

- 液化天然氣

- 混合

- 其他

第6章:市場規模及預測:按功率,2021 – 2034 年

- 主要趨勢

- < 1,000 生命值

- 1,000 - 5,000 匹馬力

- 5,001 - 10,000 匹馬力

- 10,001 - 20,000 點生命值

- > 20,000 生命值

- 20,000 點以上

第 7 章:市場規模與預測:依技術,2021 – 2034 年

- 主要趨勢

- 低速

- 中速

- 高速

第 8 章:市場規模及預測:以推進方式,2021 – 2034 年

- 主要趨勢

- 2衝程

- 四衝程

第 9 章:市場規模與預測:按應用,2021 – 2034 年

- 主要趨勢

- 商人

- 貨櫃船

- 油輪

- 散貨船

- 氣體運輸船

- 滾裝船

- 其他

- 海上

- 鑽井平台和船舶

- 起錨船

- 離岸支援船

- 浮式生產裝置

- 平台供應船

- 遊輪和渡輪

- 郵輪

- 客運渡輪

- 客船/貨船

- 海軍

- 其他

第 10 章:市場規模與預測:按地區,2021 – 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 義大利

- 挪威

- 法國

- 俄羅斯

- 丹麥

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 越南

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 伊朗

- 安哥拉

- 埃及

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

第 11 章:公司簡介

- AB Volvo Penta

- Anglo Belgian Corporation

- Brunswick Corporation

- Caterpillar

- Cummins

- Daihatsu Diesel

- DEUTZ

- Deere & Company

- Hyundai Heavy Industries

- IHI Corporation

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Rolls-Royce

- Société Internationale des Moteurs Baudouin

- Scania

- Shanghai Diesel Engine

- STX Engines

- Wärtsilä

- Weichai Holding

- Yamaha

- Yanmar

- Yuchai International

The Global Marine Engines Market, valued at USD 8.9 billion in 2024, is poised for steady growth with an expected CAGR of 3.8% from 2025 to 2034. As global trade and transportation undergo significant transformation, evolving costs, supply chain models, and logistics frameworks are reshaping the landscape of international commerce. These changes are influencing the competitiveness of nations, integrating them further into global transport networks. Trade remains an essential driver of economic development, fueling the demand for more efficient marine engines. The growing investments in port infrastructure, rapid advancements in vessel technology, and the increasing volume of seaborne transportation are all factors bolstering the market. As environmental concerns continue to rise, there is a notable shift towards eco-friendly solutions, particularly in fuel efficiency and emissions reduction. With more stringent regulations being enforced globally, the focus on sustainable marine engine technology is becoming a central market driver.

The demand for high-speed marine engines is projected to reach USD 2 billion by 2034. This surge can be attributed to the ongoing development of port facilities and the increasing demand for powerful tugboats. Small vessels, yachts, ferries, and fishing boats are particularly adopting compact engine designs that not only improve efficiency but also cut down fuel consumption and operational costs. These engines offer excellent performance while helping to reduce the overall environmental footprint, making them a highly attractive option across various marine applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 3.8% |

On the other hand, the MDO (Marine Diesel Oil) marine engine segment is set to grow at a CAGR of 4% through 2034. These engines are increasingly popular due to their efficiency and ability to maintain high-speed operations while keeping noise levels low. Their four-stroke engine design enhances fuel efficiency by consuming fuel every other cycle, a feature that distinguishes them from two-stroke engines that consume fuel with every stroke. Additionally, MDO engines don't require oil or lubricant injections, making them more eco-friendly by producing fewer emissions, thus aligning with tightening environmental regulations.

The U.S. marine engines market is also witnessing considerable expansion, projected to generate USD 1 billion by 2034. Advancements in diesel engine technology are playing a significant role in driving demand as manufacturers continue to innovate for better performance. Economic growth, an increasing focus on reliable engine performance, and rising investment in luxury and comfort features are key contributors to this expansion. Furthermore, the continuous growth in seaborne transportation is creating a long-term need for more advanced and efficient marine engines. This multi-faceted development reflects the sustained growth trajectory of the market in the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (Units & USD Million)

- 5.1 Key trends

- 5.2 MDO

- 5.3 MGO

- 5.4 LNG

- 5.5 Hybrid

- 5.6 Others

Chapter 6 Market Size and Forecast, By Power, 2021 – 2034 (Units & USD Million)

- 6.1 Key trends

- 6.2 < 1,000 HP

- 6.3 1,000 - 5,000 HP

- 6.4 5,001 - 10,000 HP

- 6.5 10,001 - 20,000 HP

- 6.6 > 20,000 HP

Chapter 7 Market Size and Forecast, By Technology, 2021 – 2034 (Units & USD Million)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 Medium speed

- 7.4 High speed

Chapter 8 Market Size and Forecast, By Propulsion, 2021 – 2034 (Units & USD Million)

- 8.1 Key trends

- 8.2 2 stroke

- 8.3 4 stroke

Chapter 9 Market Size and Forecast, By Application, 2021 – 2034 (Units & USD Million)

- 9.1 Key trends

- 9.2 Merchant

- 9.2.1 Container vessels

- 9.2.2 Tankers

- 9.2.3 Bulk carriers

- 9.2.4 Gas carriers

- 9.2.5 RO-RO

- 9.2.6 Others

- 9.3 Offshore

- 9.3.1 Drilling RIGS & ships

- 9.3.2 Anchor handling vessels

- 9.3.3 Offshore support vessels

- 9.3.4 Floating production units

- 9.3.5 Platform supply vessels

- 9.4 Cruise & Ferry

- 9.4.1 Cruise vessels

- 9.4.2 Passenger ferries

- 9.4.3 Passenger/cargo vessels

- 9.5 Navy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (Units & USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 Norway

- 10.3.5 France

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Vietnam

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Angola

- 10.5.5 Egypt

- 10.5.6 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 AB Volvo Penta

- 11.2 Anglo Belgian Corporation

- 11.3 Brunswick Corporation

- 11.4 Caterpillar

- 11.5 Cummins

- 11.6 Daihatsu Diesel

- 11.7 DEUTZ

- 11.8 Deere & Company

- 11.9 Hyundai Heavy Industries

- 11.10 IHI Corporation

- 11.11 MAN Energy Solutions

- 11.12 Mitsubishi Heavy Industries

- 11.13 Rolls-Royce

- 11.14 Société Internationale des Moteurs Baudouin

- 11.15 Scania

- 11.16 Shanghai Diesel Engine

- 11.17 STX Engines

- 11.18 Wärtsilä

- 11.19 Weichai Holding

- 11.20 Yamaha

- 11.21 Yanmar

- 11.22 Yuchai International

小型船用引擎市場規模、佔有率和成長分析(按引擎類型、安裝位置、排氣量、應用和地區分類)-2025-2032年產業預測

小型船用引擎市場規模、佔有率和成長分析(按引擎類型、安裝位置、排氣量、應用和地區分類)-2025-2032年產業預測 船用引擎市場(按產品類型、燃料類型、應用和分銷管道)—2025-2032 年全球預測高速引擎市場按應用、燃料類型、配置、技術和通路分類 - 全球預測 2025-2032

船用引擎市場(按產品類型、燃料類型、應用和分銷管道)—2025-2032 年全球預測高速引擎市場按應用、燃料類型、配置、技術和通路分類 - 全球預測 2025-2032 2025年全球高速引擎市場報告小型船用引擎市場按引擎類型、馬力範圍、燃料類型、冷卻系統、應用、配銷通路和銷售管道分類 - 2025-2030 年全球預測2025年全球小型船用引擎市場報告

2025年全球高速引擎市場報告小型船用引擎市場按引擎類型、馬力範圍、燃料類型、冷卻系統、應用、配銷通路和銷售管道分類 - 2025-2030 年全球預測2025年全球小型船用引擎市場報告 船用往復式引擎市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

船用往復式引擎市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 高速引擎市場-全球產業規模、佔有率、趨勢、機會和預測(按引擎類型、應用、功率等級、地區和競爭細分,2020-2030 年)

高速引擎市場-全球產業規模、佔有率、趨勢、機會和預測(按引擎類型、應用、功率等級、地區和競爭細分,2020-2030 年) 2026-2032 年船用引擎市場:按燃料類型、功率範圍、應用和地區分類船用氨燃料引擎市場分析及2034年預測:類型、產品、技術、組件、應用、部署、最終用戶、功能、安裝類型、解決方案

2026-2032 年船用引擎市場:按燃料類型、功率範圍、應用和地區分類船用氨燃料引擎市場分析及2034年預測:類型、產品、技術、組件、應用、部署、最終用戶、功能、安裝類型、解決方案