|

市場調查報告書

商品編碼

1685063

智慧電網市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Smart Grid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

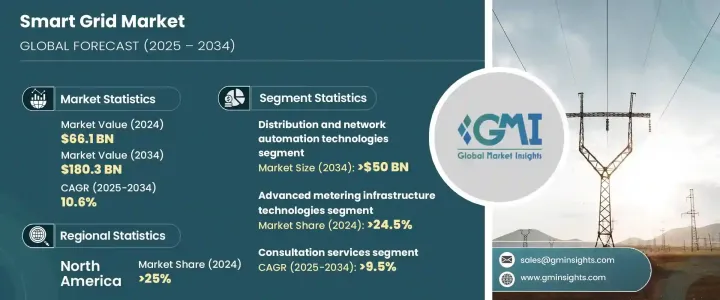

2024 年全球智慧電網市場價值為 661 億美元,預計在 2025 年至 2034 年期間將實現 10.6% 的強勁複合年成長率,這受到電力需求不斷成長、快速城市化以及對現代能源基礎設施的迫切需求的推動。隨著世界向再生能源轉型,智慧電網技術對於確保高效的能源分配、最大限度地減少傳輸損耗和提高電網可靠性變得至關重要。世界各國政府和公用事業供應商都在大力投資電網現代化、實施自動化和整合數位通訊工具以最佳化能源流。隨著電動車和智慧家庭解決方案的普及,對即時監控和智慧電網管理的需求達到了前所未有的高度。隨著氣候變遷問題和監管要求推動產業走向永續能源解決方案,智慧電網創新被證明是建立有彈性、面向未來的能源生態系統的關鍵推動因素。人工智慧、物聯網和機器學習的整合正在進一步改變市場,實現預測性維護、需求預測和增強電網安全。公用事業公司正在利用這些進步來提高營運效率並降低成本,而消費者則受益於更高的能源透明度和具有成本效益的電力消耗。

多年來,市場穩步擴張,其價值從 2022 年的 552 億美元增加到 2023 年的 602 億美元和 2024 年的 661 億美元。該產業根據技術分為消費者介面、配電和網路自動化、智慧輸配電設備、先進計量基礎設施以及通訊和無線基礎設施。其中,配電和網路自動化技術預計到 2034 年將超過 500 億美元,因為公用事業公司專注於實施自動控制和即時監控,以增強電網彈性並最佳化能源分配。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 661億美元 |

| 預測值 | 1803億美元 |

| 複合年成長率 | 10.6% |

部署和整合服務在 2024 年佔據主導地位,佔據超過 44% 的市場佔有率,並有望持續成長。日益普及的複雜IT系統和先進的智慧技術,推動了對智慧電網解決方案的無縫整合和大規模實施的需求。電動車充電站普及率的提高也在加速智慧電網技術的採用方面發揮著至關重要的作用。能源供應商正在積極投資先進的系統,以有效管理配電並平衡電力供應和波動的需求。

2024 年,北美智慧電網市場佔全球佔有率的 25%,預計到 2034 年將實現強勁成長。光是美國市場在 2022 年的價值就達到 118 億美元,到 2023 年將成長到 127 億美元,到 2024 年將成長到 137 億美元。老化能源基礎設施的現代化,加上對智慧能源解決方案的監管支持不斷增加,正在推動這一成長。同時,受電力消耗增加、城市快速擴張以及政府主導的電網技術升級措施的推動,亞太地區預計將在 2034 年創造 750 億美元的收入。隨著對先進能源管理解決方案的投資不斷增加,智慧電網市場將在全球主要地區大幅擴張。

目錄

第 1 章:方法論與範圍

- 市場定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 戰略儀表板

- 創新與永續發展格局

第 5 章:市場規模與預測:依技術,2021 – 2034 年

- 主要趨勢

- 智慧型輸配電設備

- 配電和網路自動化

- 先進的計量基礎設施

- 消費者介面

- 通訊和無線基礎設施

第6章:市場規模及預測:依服務,2021 – 2034 年

- 主要趨勢

- 諮詢

- 部署與整合

- 支援與維護

第 7 章:市場規模與預測:依部署,2021 – 2034 年

- 主要趨勢

- 世代

- 傳染

- 分配

- 最終用途

第 8 章:市場規模與預測:按地區,2021 – 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 澳洲

- 日本

- 韓國

- 印度

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 智利

第9章:公司簡介

- ABB

- Belden

- Cisco Systems

- Fujitsu

- General Electric

- Honeywell International

- Hubbell

- IBM

- Itron

- Landis+Gyr

- Oracle

- Schneider Electric

- Siemens

- Wipro

The Global Smart Grid Marketm Valued At USD 66.1 Billion In 2024, Is Projected To Register A Robust CAGR Of 10.6% Between 2025 And 2034., Driven By The Increasing Demand For Electricity, Rapid Urbanization, And The Urgent Need For Modern Energy Infrastructure. As The World Transitions Toward Renewable Energy Sources, Smart Grid Technologies Are Becoming Essential To Ensure Efficient Energy Distribution, Minimize Transmission Losses, And Enhance Grid Reliability. Governments And Utility Providers Worldwide Are Making Substantial Investments In Modernizing Power Grids, Implementing Automation, And Integrating Digital Communication Tools To Optimize Energy Flow. With The Rising Adoption Of Electric Vehicles And Smart Home Solutions, The Demand For Real-Time Monitoring And Intelligent Grid Management Is At An All-Time High. As Climate Change Concerns And Regulatory Mandates Push The Industry Toward Sustainable Energy Solutions, Smart Grid Innovations Are Proving To Be A Critical Enabler Of A Resilient And Future-Ready Energy Ecosystem. The Integration Of Artificial Intelligence, IoT, And Machine Learning Is Further Revolutionizing The Market, allowing for predictive maintenance, demand forecasting, and enhanced grid security. Utility companies are leveraging these advancements to improve operational efficiency and reduce costs, while consumers benefit from greater energy transparency and cost-effective power consumption.

The market has seen steady expansion over the years, with its value increasing from USD 55.2 billion in 2022 to USD 60.2 billion in 2023 and USD 66.1 billion in 2024. The industry is categorized based on technology into consumer interface, distribution and network automation, smart transmission and distribution equipment, advanced metering infrastructure, and communication and wireless infrastructure. Among these, distribution and network automation technologies are expected to surpass USD 50 billion by 2034, as utilities focus on implementing automated controls and real-time monitoring to strengthen grid resilience and optimize energy distribution.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $66.1 Billion |

| Forecast Value | $180.3 Billion |

| CAGR | 10.6% |

Deployment and integration services held a dominant position in 2024, accounting for over 44% of the market share, with expectations for sustained growth. The increasing adoption of sophisticated IT systems and advanced smart technologies is driving the demand for seamless integration and large-scale implementation of intelligent grid solutions. The rising penetration of electric vehicle charging stations is also playing a crucial role in accelerating the adoption of smart grid technology. Energy providers are actively investing in advanced systems to efficiently manage power distribution and balance electricity supply with fluctuating demand.

North America smart grid market accounted for 25% of the global share in 2024, with strong growth projections through 2034. The U.S. market alone was valued at USD 11.8 billion in 2022, growing to USD 12.7 billion in 2023 and USD 13.7 billion in 2024. The modernization of aging energy infrastructure, coupled with increasing regulatory support for smart energy solutions, is fueling this growth. Meanwhile, the Asia Pacific region is on track to generate USD 75 billion by 2034, driven by rising electricity consumption, rapid urban expansion, and government-led initiatives to upgrade grid technology. As investments in advanced energy management solutions continue to rise, the smart grid market is set to witness substantial expansion across key global regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Smart T&D equipment

- 5.3 Distribution & network automation

- 5.4 Advanced metering infrastructure

- 5.5 Consumer interface

- 5.6 Communication & wireless infrastructure

Chapter 6 Market Size and Forecast, By Service, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Consulting

- 6.3 Deployment & integration

- 6.4 Support & maintenance

Chapter 7 Market Size and Forecast, By Deployment, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Generation

- 7.3 Transmission

- 7.4 Distribution

- 7.5 End use

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 India

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Chile

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Belden

- 9.3 Cisco Systems

- 9.4 Fujitsu

- 9.5 General Electric

- 9.6 Honeywell International

- 9.7 Hubbell

- 9.8 IBM

- 9.9 Itron

- 9.10 Landis+Gyr

- 9.11 Oracle

- 9.12 Schneider Electric

- 9.13 Siemens

- 9.14 Wipro

全球虛擬電廠 (VPP) 市場:預測至 2032 年 - 按產品、動力來源、技術、最終用戶和地區分類的分析智慧電網基礎設施市場預測至2032年:按組件、部署類型、技術、應用、最終用戶和地區分類的全球分析

全球虛擬電廠 (VPP) 市場:預測至 2032 年 - 按產品、動力來源、技術、最終用戶和地區分類的分析智慧電網基礎設施市場預測至2032年:按組件、部署類型、技術、應用、最終用戶和地區分類的全球分析 智慧電網市場(按組件、產品、應用、最終用戶和技術)—2025-2032 年全球預測智慧電網託管服務市場(按服務類型、部署模式、最終用戶和電網細分)—全球預測 2025-2032智慧電網通訊市場(按組件、網路類型、通訊技術、應用和最終用戶分類)—2025-2032 年全球預測

智慧電網市場(按組件、產品、應用、最終用戶和技術)—2025-2032 年全球預測智慧電網託管服務市場(按服務類型、部署模式、最終用戶和電網細分)—全球預測 2025-2032智慧電網通訊市場(按組件、網路類型、通訊技術、應用和最終用戶分類)—2025-2032 年全球預測 智慧電網網路市場規模、佔有率、成長分析(硬體、軟體、服務和地區)—2025-2032 年產業預測

智慧電網網路市場規模、佔有率、成長分析(硬體、軟體、服務和地區)—2025-2032 年產業預測 2025年全球智慧電網技術市場報告2025年全球智慧電網通訊市場報告2032 年智慧電網市場預測:按組件、部署模型、通訊技術、應用、最終用戶和地區進行的全球分析

2025年全球智慧電網技術市場報告2025年全球智慧電網通訊市場報告2032 年智慧電網市場預測:按組件、部署模型、通訊技術、應用、最終用戶和地區進行的全球分析 日本智慧電網市場報告(按組件(軟體、硬體、服務)、最終用戶(住宅、商業、工業)和地區)2025-2033

日本智慧電網市場報告(按組件(軟體、硬體、服務)、最終用戶(住宅、商業、工業)和地區)2025-2033