|

市場調查報告書

商品編碼

1685178

腸內餵食設備市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Enteral Feeding Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

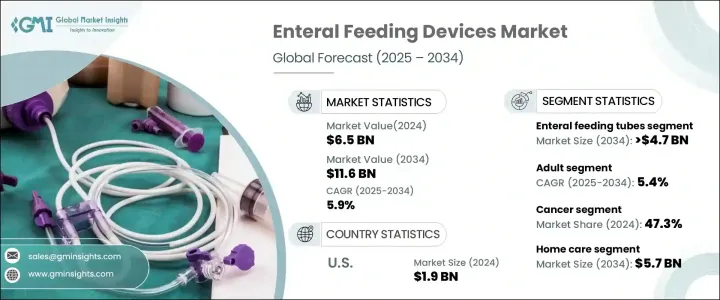

2024 年全球腸內餵食設備市場價值為 65 億美元,預計 2025 年至 2034 年的複合年成長率為 5.9%。該領域的成長主要得益於慢性病盛行率的上升、新生兒和早產兒餵食需求的增加以及家庭護理環境中腸內餵食解決方案的廣泛採用。隨著越來越多的人面臨損害其自然進食能力的狀況,對這些設備的需求持續上升。腸內餵食對於因醫療狀況而無法口服進食的患者提供必需的營養素起著至關重要的作用。接受影響咀嚼或吞嚥能力的治療的患者依靠這些設備來維持充足的營養。家庭護理由於其成本效益和便利性而正在顯著成長。醫療保健提供者擴大推薦腸內餵食解決方案來滿足短期和長期的營養需求。

腸內餵食設備市場依產品類型分類,包括腸內餵食管、幫浦、注射器、給藥裝置和配件。預計腸內營養管將引領市場擴張,預計複合年成長率為 5.6%,到 2034 年將達到 47 億美元以上。這些管子對於為患有各種健康狀況的個人提供有針對性的營養至關重要。它們在急性和慢性護理環境中的作用使它們成為確保適當營養的首選解決方案。不同類型的餵食管使得醫療專業人員能夠根據患者的個別需求量身訂做治療方案。隨著醫院、診所和家庭護理機構的廣泛採用,腸內餵食管仍然是市場成長的主要驅動力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 65億美元 |

| 預測值 | 116億美元 |

| 複合年成長率 | 5.9% |

市場也根據患者群體進行細分,包括成人和兒童人群。成人類別佔最大佔有率,預計從 2025 年到 2034 年的複合年成長率為 5.4%。需要腸內營養的成人數量不斷增加,導致這些設備的需求持續增加。許多患有長期疾病的成年人需要長期腸內餵食以維持健康並預防併發症。這些解決方案在安寧療護中的應用越來越廣泛,進一步刺激了需求,因為它們在無法進行傳統餵食的情況下提供了重要的營養支持。

在應用方面,腸內營養裝置廣泛應用於各種醫療狀況,包括癌症、神經系統疾病和胃腸道疾病。 2024 年,癌症領域佔了 47.3% 的市場。許多治療導致進食困難,因此需要腸內餵食以維持充足的營養。對於需要長期照護的個人,這些設備在確保能量水平保持穩定同時防止進一步併發症方面發揮著至關重要的作用。

市場也按最終用途分類,包括家庭護理、醫院和其他設施。家庭護理產業在 2024 年引領市場,預計到 2034 年將達到 57 億美元。人口老化推動了對家庭腸內營養的需求,使個人能夠在保持獨立性的同時獲得必要的營養支持。與長期住院相比,居家照護由於價格便宜,成為許多患者的首選。隨著可近性的提高,更多的人可以從這些解決方案中受益,特別是在自付醫療費用較高的地區。

2024 年美國腸內營養設備市場價值為 19 億美元,預計到 2034 年將以 5.2% 的複合年成長率成長。老年人口的成長和家庭醫療保健服務的日益普及支持了市場擴張。領先公司的研發努力促進了創新和產品的可用性。優惠的報銷政策和政府支持的促進營養療法的舉措進一步增強了市場成長。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病盛行率上升

- 新生兒和早產兒腸餵食需求增加

- 居家照護環境中腸內餵食的偏好不斷增加

- 腸內營養裝置的技術進步

- 產業陷阱與挑戰

- 與腸內營養管相關的併發症

- 嚴格的政府法規和合規要求

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 報銷場景

- 差距分析

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 腸內營養管

- 鼻腸管/鼻飼管

- 鼻胃管

- 鼻空腸管

- 腹部/造口飼管

- 胃造口管

- 空腸造口/空腸管

- 胃空腸管 (GJ) 或經空腸管

- 鼻腸管/鼻飼管

- 腸內營養泵

- 腸內注射器

- 贈送套裝

- 配件

第 6 章:市場估計與預測:按患者,2021 - 2034 年

- 主要趨勢

- 成人

- 兒科

第 7 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 癌症

- 頭頸癌

- 胃腸道癌症

- 其他癌症類型

- 中樞神經系統 (CNS) 和心理健康

- 非惡性胃腸道 (GI) 疾病

- 其他應用

第 8 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 居家護理

- 醫院

- 其他最終用途

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- ALCOR SCIENTIFIC

- Abbott

- AMSINO

- AMT

- - Braun

- Baxter

- Becton Dickinson

- Boston Scientific

- Cardinal Health

- CONMED

- Cook Medical

- DANONE

- FRESENIUS KABI

- HALYARD

- MOOG

- VYGON

The Global Enteral Feeding Devices Market was valued at USD 6.5 billion in 2024 and is projected to grow at a CAGR of 5.9% from 2025 to 2034. Growth in this sector is driven by the increasing prevalence of chronic illnesses, rising demand for neonatal and preterm feeding, and the expanding adoption of enteral feeding solutions in home care settings. As more individuals face conditions that impair their ability to consume food naturally, the demand for these devices continues to climb. Enteral feeding plays a crucial role in delivering essential nutrients to individuals who cannot eat orally due to medical conditions. Patients undergoing treatments that impact their ability to chew or swallow rely on these devices to maintain adequate nutrition. Home-based care is seeing significant growth due to its cost-effectiveness and convenience. Healthcare providers increasingly recommend enteral feeding solutions for managing both short-term and long-term nutritional needs.

The enteral feeding devices market is categorized based on product type, including enteral feeding tubes, pumps, syringes, giving sets, and accessories. Enteral feeding tubes are expected to lead market expansion with a projected CAGR of 5.6%, reaching over USD 4.7 billion by 2034. These tubes are essential for delivering targeted nutrition to individuals dealing with various health conditions. Their role in acute and chronic care settings makes them a preferred solution for ensuring proper nourishment. The availability of different types of feeding tubes enables healthcare professionals to customize treatments based on individual patient needs. With broad adoption across hospitals, clinics, and home care facilities, enteral feeding tubes remain a primary driver of market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 5.9% |

The market is also segmented based on patient groups, including adult and pediatric populations. The adult category holds the largest share and is expected to grow at a CAGR of 5.4% from 2025 to 2034. A rising number of adults requiring enteral nutrition contributes to sustained demand for these devices. Many adults with long-term conditions need enteral feeding for extended periods to maintain health and prevent complications. The increasing adoption of these solutions in palliative care further boosts demand, as they provide vital nutritional support in cases where traditional feeding is not an option.

In terms of application, enteral feeding devices are widely used across various medical conditions, including cancer, neurological disorders, and gastrointestinal diseases. The cancer segment accounted for 47.3% of the market share in 2024. Many treatments lead to difficulties in consuming food, making enteral feeding necessary to maintain adequate nutrition. For individuals requiring long-term care, these devices play an essential role in ensuring energy levels remain stable while preventing further complications.

The market is also divided by end-use, including home care, hospitals, and other facilities. The home care sector led the market in 2024 and is expected to reach USD 5.7 billion by 2034. An aging population drives demand for home-based enteral feeding, allowing individuals to receive necessary nutritional support while maintaining independence. The affordability of home-based care, compared to extended hospital stays, makes it a preferred choice for many patients. With increased accessibility, more individuals can benefit from these solutions, particularly in regions with high out-of-pocket healthcare expenses.

The U.S. enteral feeding devices market was valued at USD 1.9 billion in 2024 and is projected to grow at a CAGR of 5.2% through 2034. A growing elderly population and increasing adoption of home healthcare services support market expansion. Research and development efforts by leading companies contribute to innovation and product availability. Favorable reimbursement policies and government-backed initiatives promoting nutritional therapies further strengthen market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Increase in demand for neonatal and preterm enteral feeding

- 3.2.1.3 Surging preference for enteral feeding at home care settings

- 3.2.1.4 Technological advancements in enteral feeding devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications associated with enteral feeding tubes

- 3.2.2.2 Stringent government regulations and compliance requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Enteral feeding tubes

- 5.2.1 Nasoenteric/nasal feeding tube

- 5.2.1.1 Nasogastric tube

- 5.2.1.2 Nasojejunal tube

- 5.2.2 Abdominal/ostotomy feeding tube

- 5.2.2.1 Gastrostomy tube

- 5.2.2.2 Jejunostomy/jejunal tube

- 5.2.2.3 Gastrojejunal (GJ) or transjejunal tube

- 5.2.1 Nasoenteric/nasal feeding tube

- 5.3 Enteral feeding pumps

- 5.4 Enteral syringes

- 5.5 Giving sets

- 5.6 Accessories

Chapter 6 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cancer

- 7.2.1 Head and neck cancer

- 7.2.2 Gastrointestinal cancer

- 7.2.3 Other cancer types

- 7.3 Central nervous system (CNS) and mental health

- 7.4 Non-malignant gastrointestinal (GI) disorders

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Home care

- 8.3 Hospitals

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALCOR SCIENTIFIC

- 10.2 Abbott

- 10.3 AMSINO

- 10.4 AMT

- 10.5 - Braun

- 10.6 Baxter

- 10.7 Becton Dickinson

- 10.8 Boston Scientific

- 10.9 Cardinal Health

- 10.10 CONMED

- 10.11 Cook Medical

- 10.12 DANONE

- 10.13 FRESENIUS KABI

- 10.14 HALYARD

- 10.15 MOOG

- 10.16 VYGON

2025 年全球經腸營養設備市場報告

2025 年全球經腸營養設備市場報告 經腸營養設備市場:按產品、年齡層、應用和最終用戶 - 2025-2030 年全球預測

經腸營養設備市場:按產品、年齡層、應用和最終用戶 - 2025-2030 年全球預測 胃按鈕市場,按產品、按應用、按使用、按最終用戶、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測經腸營養市場:按管、年齡、應用、最終用戶分類 - 全球預測 2025-2030腸道餵食幫浦市場:按類型、產品和最終用戶分類 - 全球預測 2025-2030

胃按鈕市場,按產品、按應用、按使用、按最終用戶、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測經腸營養市場:按管、年齡、應用、最終用戶分類 - 全球預測 2025-2030腸道餵食幫浦市場:按類型、產品和最終用戶分類 - 全球預測 2025-2030 經腸營養設備的全球市場:洞察,競爭情形,市場預測:2030年

經腸營養設備的全球市場:洞察,競爭情形,市場預測:2030年 經腸營養器材市場規模、佔有率、成長分析、按產品類型、年齡層、應用、地區 - 產業預測,2024-2031 年

經腸營養器材市場規模、佔有率、成長分析、按產品類型、年齡層、應用、地區 - 產業預測,2024-2031 年 腸內飼管市場、機會、成長動力、產業趨勢分析與預測,2024-20322024-2032 年按產品類型、年齡層、應用、最終用戶和地區分類的腸內餵食設備市場報告2024 年新生兒經腸營養裝置全球市場報告

腸內飼管市場、機會、成長動力、產業趨勢分析與預測,2024-20322024-2032 年按產品類型、年齡層、應用、最終用戶和地區分類的腸內餵食設備市場報告2024 年新生兒經腸營養裝置全球市場報告