|

市場調查報告書

商品編碼

1685187

印刷紙箱市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Printed Cartons Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

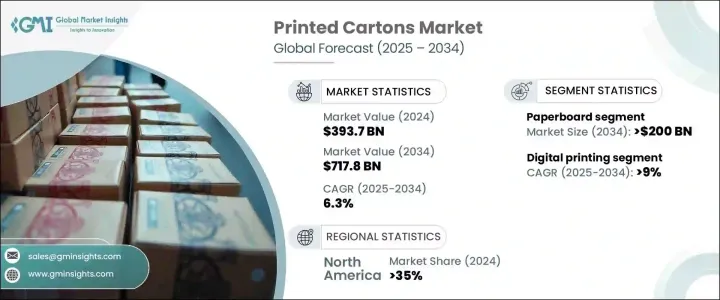

2024 年全球印刷紙箱市場價值為 3,937 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.3%。這一成長主要得益於食品、零售和奢侈品等行業對優質、可客製化包裝解決方案的需求不斷成長。隨著企業優先考慮能夠增強產品展示效果並支持永續性的包裝,高品質、視覺衝擊力強的印刷紙箱越來越受到青睞。企業正在投資創新印刷技術和自動化技術,以提高生產效率,從而能夠在不增加成本的情況下滿足消費者日益成長的期望。

永續發展的推動進一步加速了市場擴張,品牌更加重視環保材料並減少包裝浪費。消費者越來越傾向於可回收和可生物分解的包裝選擇,這迫使製造商整合對環境負責的解決方案。政府提倡永續包裝實踐的法規也在影響產業趨勢。電子商務的快速成長是另一個關鍵因素,因為線上零售商擴大尋求耐用而又具有視覺吸引力的包裝,以增強客戶體驗和品牌形象。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3937億美元 |

| 預測值 | 7178億美元 |

| 複合年成長率 | 6.3% |

印刷紙箱市場涵蓋的材料種類繁多,包括紙板、瓦楞紙板、牛皮紙板、塗佈紙和液體紙板。預計到 2034 年紙板的市場價值將達到 2000 億美元,由於其多功能性和在各個行業的廣泛應用,紙板將成為主導市場。作為一種價格實惠的高品質材料,紙板可以支持清晰、生動的圖形,使其成為化妝品、藥品和奢侈品等高階產品的理想選擇。其光滑的質地增強了印刷清晰度,為品牌提供了一種透過精緻的包裝設計吸引消費者注意力的引人注目的方式。

印刷技術的進步也推動了市場的成長。該行業包括膠印、柔版印刷、數位印刷、凹印、網版印刷和其他技術。其中,數位印刷是成長最快的領域,預計在 2025 年至 2034 年期間的複合年成長率將達到 9%。數位印刷為企業提供了更大的靈活性,允許短期生產,而無需花費印版或複雜的設定。該技術可實現快速週轉和經濟高效的客製化,對於尋求獨特、高影響力包裝的品牌來說尤其有價值。此外,數位印刷可提供具有精細細節的清晰全彩圖像,滿足旨在透過創新設計提升品牌知名度的企業的需求。

北美將繼續保持其在印刷紙箱市場的領導地位,到 2024 年將佔據 35% 的市場佔有率。該地區的主導地位源於消費者對永續包裝日益成長的需求、印刷技術的進步以及不斷擴大的電子商務格局。越來越多的公司採用紙板和牛皮紙板等可回收材料來符合環保偏好,而數位印刷和柔版印刷創新則增強了包裝的美觀性和功能性。隨著品牌在競爭激烈的市場中力求差異化,對高品質、視覺衝擊力強的印刷紙箱的需求不斷上升,進一步推動了市場的擴張。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 對永續包裝解決方案的需求不斷增加

- 隨著數位印刷技術的興起,客製化趨勢日益明顯

- 電子商務成長推動包裝需求

- 轉向優質、具吸引力的包裝設計

- 品牌和增強消費者體驗重點

- 產業陷阱與挑戰

- 生產和材料成本高限制

- 供應鏈中斷影響生產時間表

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 紙板

- 瓦楞紙板

- 牛皮紙板

- 塗料紙

- 液體板

第 6 章:市場估計與預測:按印刷技術,2021-2034 年

- 主要趨勢

- 膠印

- 柔版印刷

- 數位印刷

- 凹版印刷

- 網版印刷

- 其他

第 7 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 食品和飲料

- 個人護理和化妝品

- 製藥

- 消費品

- 電氣和電子產品

- 其他

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- All Packaging Company

- Amcor

- Ariba & Company

- Atlantic Packaging

- DS Smith

- Elopak

- Fencor Packaging Group

- LGR Packaging

- Oji Holdings

- Parksons Packaging

- Pratt Industries

- SIG Combibloc

- Stora Enso

- Tetra Pak

- TCPL Packaging

- Winston Packaging

The Global Printed Cartons Market, valued at USD 393.7 billion in 2024, is on track to expand at a CAGR of 6.3% from 2025 to 2034. This growth is fueled by the increasing demand for premium, customizable packaging solutions across industries such as food, retail, and luxury goods. As businesses prioritize packaging that enhances product presentation while supporting sustainability, high-quality, visually striking printed cartons are gaining traction. Companies are investing in innovative printing technologies and automation to boost production efficiency, allowing them to meet rising consumer expectations without inflating costs.

The push toward sustainability is further accelerating market expansion, with brands focusing on eco-friendly materials and reducing packaging waste. Consumers are gravitating toward recyclable and biodegradable packaging options, compelling manufacturers to integrate environmentally responsible solutions. Government regulations promoting sustainable packaging practices are also shaping industry trends. The rapid growth of e-commerce is another pivotal factor, as online retailers increasingly seek durable yet visually appealing packaging to enhance customer experience and brand identity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $393.7 Billion |

| Forecast Value | $717.8 Billion |

| CAGR | 6.3% |

The printed cartons market encompasses a wide range of materials, including paperboard, corrugated board, kraft board, coated paper, and liquid board. Paperboard is expected to reach USD 200 billion by 2034, making it the dominant segment due to its versatility and widespread application across industries. As an affordable and high-quality material, paperboard supports sharp, vibrant graphics, making it an ideal choice for premium products such as cosmetics, pharmaceuticals, and luxury goods. Its smooth texture enhances print clarity, offering brands a compelling way to attract consumer attention through sophisticated packaging designs.

Advancements in printing technology are also driving market growth. The industry includes offset printing, flexographic printing, digital printing, gravure printing, screen printing, and other techniques. Among these, digital printing stands out as the fastest-growing segment, poised to expand at a CAGR of 9% between 2025 and 2034. Digital printing offers businesses greater flexibility, allowing for short-run productions without the expense of printing plates or complex setups. This technology enables rapid turnarounds and cost-efficient customization, making it particularly valuable for brands seeking distinctive, high-impact packaging. Furthermore, digital printing delivers sharp, full-color images with intricate details, catering to businesses aiming to elevate brand recognition through innovative designs.

North America is set to maintain its leadership position in the printed cartons market, holding a 35% market share in 2024. The region's dominance stems from growing consumer demand for sustainable packaging, advancements in printing technology, and the expanding e-commerce landscape. Companies are increasingly adopting recyclable materials like paperboard and kraft board to align with eco-conscious preferences, while digital and flexographic printing innovations are enhancing packaging aesthetics and functionality. As brands strive for differentiation in a competitive market, the demand for high-quality, visually striking printed cartons continues to rise, further propelling the market's expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Key news & initiatives

- 3.3 Regulatory landscape

- 3.4 Impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Increasing demand for sustainable packaging solutions

- 3.4.1.2 Rise in customization with digital printing technology

- 3.4.1.3 E-commerce growth boosting packaging requirements

- 3.4.1.4 Shift towards premium and attractive packaging designs

- 3.4.1.5 Branding and enhanced consumer experience focus

- 3.4.2 Industry pitfalls & challenges

- 3.4.2.1 High production and material costs constraints

- 3.4.2.2 Supply chain disruptions impacting production timelines

- 3.4.1 Growth drivers

- 3.5 Growth potential analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Paperboard

- 5.3 Corrugated board

- 5.4 Kraft board

- 5.5 Coated paper

- 5.6 Liquid board

Chapter 6 Market Estimates & Forecast, By Printing Technology, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Offset printing

- 6.3 Flexographic printing

- 6.4 Digital printing

- 6.5 Gravure printing

- 6.6 Screen printing

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Personal care & cosmetics

- 7.4 Pharmaceutical

- 7.5 Consumer goods

- 7.6 Electricals & electronics

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 All Packaging Company

- 9.2 Amcor

- 9.3 Ariba & Company

- 9.4 Atlantic Packaging

- 9.5 DS Smith

- 9.6 Elopak

- 9.7 Fencor Packaging Group

- 9.8 LGR Packaging

- 9.9 Oji Holdings

- 9.10 Parksons Packaging

- 9.11 Pratt Industries

- 9.12 SIG Combibloc

- 9.13 Stora Enso

- 9.14 Tetra Pak

- 9.15 TCPL Packaging

- 9.16 Winston Packaging