|

市場調查報告書

商品編碼

1698263

智慧藥丸市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Smart Pills Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

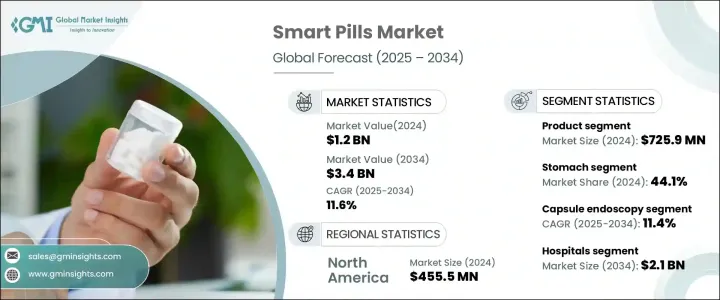

2024 年全球智慧藥丸市場規模達到 12 億美元,預計 2025 年至 2034 年期間複合年成長率將達到驚人的 11.6%。胃腸道疾病盛行率的上升以及對非侵入性診斷解決方案的需求的增加是推動這一成長的主要因素。隨著醫療保健產業向微創技術轉變,智慧藥丸正在徹底改變診斷和治療方法。這些可攝取的醫療設備配備感測器、微晶片和無線通訊功能,可實現即時患者監測、精確藥物傳輸和增強疾病追蹤。個人化醫療和遠距醫療解決方案的需求日益成長,進一步加速了市場採用智慧藥丸,因為智慧藥丸提供了無縫的診斷和治療組合,同時最大限度地減少了患者的不適。

此外,慢性病負擔的增加、全球人口老化以及醫療保健支出的增加也促進了市場的擴張。政府支持數位醫療以及人工智慧 (AI) 和物聯網 (IoT) 技術進步的舉措正在促進市場的快速發展。人工智慧藥丸正在提高資料處理效率,實現更快、更準確的診斷,同時最佳化治療方案。同時,物聯網整合可以實現持續的病患監控,減少醫院就診次數並改善整體醫療管理。隨著醫療保健提供者和患者越來越認知到智慧藥丸的好處,未來十年市場將呈指數級成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 12億美元 |

| 預測值 | 34億美元 |

| 複合年成長率 | 11.6% |

市場根據組件細分為產品和患者監測軟體。 2024 年,該產品部門的收入為 7.259 億美元,這主要得益於嵌入微晶片和感測器的智慧膠囊的日益普及。這些膠囊在監測胃腸道健康、確保藥物依從性和追蹤病情進展方面發揮著至關重要的作用。透過提供即時資料,智慧膠囊可以實現精確的藥物管理,同時無需傳統的侵入性診斷程序。這些解決方案的易用性和非侵入性使其成為醫療診斷和治療應用的首選。

市場進一步依目標區域分類,應用範圍涵蓋胃、小腸、大腸和食道。 2024 年,胃病領域佔據了 44.1% 的市場佔有率,這主要是由於胃病患病率不斷上升以及對即時、非侵入性診斷工具的需求增加。專為胃部應用而設計的智慧藥丸可提高診斷準確性和治療效果,解決多種胃腸道疾病。胃病發病率的不斷上升刺激了對這些創新解決方案的需求,使胃部成為市場的主導部分。

北美仍然是智慧藥丸的主要市場,到 2024 年將達到 4.555 億美元,預計未來幾年的複合年成長率為 11.3%。該地區受益於完善的醫療保健基礎設施、早期採用的先進醫療技術以及日益成長的易患慢性疾病的老年人口。胃腸道疾病的增多,加上可攝取感測器技術的不斷進步,正在推動市場擴張。專注於醫療技術研究和創新的關鍵產業參與者正在進一步推動市場成長,鞏固北美在全球智慧藥丸產業的地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 胃腸道疾病盛行率不斷上升

- 智慧藥丸技術的不斷改進

- 非侵入性診斷工具的需求不斷成長

- 產業陷阱與挑戰

- 嚴格的監管要求

- 設備成本高

- 成長動力

- 成長潛力分析

- 技術格局

- 監管格局

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按組成部分,2021 年至 2034 年

- 主要趨勢

- 產品

- 膠囊

- 其他產品

- 病人監護軟體

第6章:市場估計與預測:按目標區域,2021 年至 2034 年

- 主要趨勢

- 胃

- 小腸

- 大腸

- 食道

第7章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 膠囊內視鏡

- 靶向藥物輸送

- 生命徵象監測

第8章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 診斷中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- ANX Robotica

- Bodycap

- CapsoVision

- Check-Cap

- etectRx

- Intromedic

- Medtronic

- Otsuka Holdings

- Olympus Corporation

- RF Co

The Global Smart Pills Market reached USD 1.2 billion in 2024 and projected to register an impressive CAGR of 11.6% from 2025 to 2034. The rising prevalence of gastrointestinal disorders and the increasing demand for non-invasive diagnostic solutions are major factors fueling this growth. As the healthcare industry shifts toward minimally invasive technologies, smart pills are revolutionizing diagnostics and treatment approaches. These ingestible medical devices, equipped with sensors, microchips, and wireless communication capabilities, enable real-time patient monitoring, precise drug delivery, and enhanced disease tracking. The growing need for personalized medicine and remote healthcare solutions is further accelerating market adoption, as smart pills offer a seamless blend of diagnostics and treatment with minimal discomfort to patients.

Additionally, the rising burden of chronic diseases, an aging global population, and increased healthcare spending are contributing to the market's expansion. Government initiatives supporting digital healthcare and technological advancements in artificial intelligence (AI) and the Internet of Things (IoT) are reinforcing the market's rapid evolution. AI-powered smart pills are enhancing data processing efficiency, enabling faster and more accurate diagnoses while optimizing treatment plans. Meanwhile, IoT integration allows continuous patient monitoring, reducing hospital visits and improving overall healthcare management. With healthcare providers and patients increasingly recognizing the benefits of smart pills, the market is poised for exponential growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 11.6% |

The market is segmented based on components into products and patient monitoring software. In 2024, the product segment generated USD 725.9 million, largely driven by the increasing adoption of smart capsules embedded with microchips and sensors. These capsules play a crucial role in monitoring gastrointestinal health, ensuring medication adherence, and tracking disease progression. By delivering real-time data, smart capsules enable precise drug administration while eliminating the need for traditional invasive diagnostic procedures. The ease of use and non-invasive nature of these solutions are making them a preferred choice for medical diagnostics and therapeutic applications.

The market is further classified by target area, with applications spanning the stomach, small intestine, large intestine, and esophagus. The stomach segment accounted for 44.1% of the market share in 2024, largely due to the increasing prevalence of stomach-related disorders and the demand for real-time, non-invasive diagnostic tools. Smart pills designed for stomach applications offer enhanced diagnostic accuracy and improved treatment efficacy, addressing a broad range of gastrointestinal conditions. The growing incidence of gastric diseases is fueling demand for these innovative solutions, making the stomach a dominant segment within the market.

North America remains a leading market for smart pills, reaching USD 455.5 million in 2024 and expected to grow at a CAGR of 11.3% in the coming years. The region benefits from a well-established healthcare infrastructure, early adoption of advanced medical technologies, and a rising elderly population prone to chronic illnesses. The increasing number of gastrointestinal disorders, coupled with continuous technological advancements in ingestible sensors, is driving market expansion. Key industry players focused on research and innovation in medical technology are further propelling market growth, reinforcing North America's stronghold in the global smart pills industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of gastrointestinal disorders

- 3.2.1.2 Continuous improvements in smart pill technology

- 3.2.1.3 Growing demand for non-invasive diagnostic tools

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements

- 3.2.2.2 High cost of devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Product

- 5.2.1 Capsule

- 5.2.2 Other products

- 5.3 Patient monitoring software

Chapter 6 Market Estimates and Forecast, By Target Area, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Stomach

- 6.3 Small intestine

- 6.4 Large intestine

- 6.5 Esophagus

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Capsule endoscopy

- 7.3 Targeted drug delivery

- 7.4 Vital sign monitoring

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ANX Robotica

- 10.2 Bodycap

- 10.3 CapsoVision

- 10.4 Check-Cap

- 10.5 etectRx

- 10.6 Intromedic

- 10.7 Medtronic

- 10.8 Otsuka Holdings

- 10.9 Olympus Corporation

- 10.10 RF Co

全球智慧藥丸市場按治療領域、應用、適應症、最終用戶和地區分類 - 預測至 2030 年

全球智慧藥丸市場按治療領域、應用、適應症、最終用戶和地區分類 - 預測至 2030 年 智慧藥丸市場報告:趨勢、預測和競爭分析(至 2031 年)

智慧藥丸市場報告:趨勢、預測和競爭分析(至 2031 年) 智慧注射器技術市場分析及預測至 2033 年:按類型、產品、服務、技術、組件、應用、最終用戶、設備、功能和安裝類型

智慧注射器技術市場分析及預測至 2033 年:按類型、產品、服務、技術、組件、應用、最終用戶、設備、功能和安裝類型 智慧藥丸技術市場規模、佔有率和成長分析(按目標領域、適用疾病、應用、最終用戶和地區):產業預測(2025-2032)

智慧藥丸技術市場規模、佔有率和成長分析(按目標領域、適用疾病、應用、最終用戶和地區):產業預測(2025-2032) 智慧藥丸技術市場,按目標領域、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

智慧藥丸技術市場,按目標領域、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 可攝取智慧藥丸的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

可攝取智慧藥丸的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年) 智慧藥物和藥丸市場:按目標領域、類型、最終用戶、應用 - 2025-2030 年全球預測

智慧藥物和藥丸市場:按目標領域、類型、最終用戶、應用 - 2025-2030 年全球預測 2024-2032 年智慧藥丸市場報告(按目標領域、疾病適應症、應用、最終用戶和地區)

2024-2032 年智慧藥丸市場報告(按目標領域、疾病適應症、應用、最終用戶和地區) 全球心理健康數位藥丸市場 - 2024-2031

全球心理健康數位藥丸市場 - 2024-2031 智慧藥丸市場規模、佔有率和成長分析:按應用、目標領域、最終用戶、地區 - 產業預測,2024-2031 年

智慧藥丸市場規模、佔有率和成長分析:按應用、目標領域、最終用戶、地區 - 產業預測,2024-2031 年