|

市場調查報告書

商品編碼

1698264

智慧家庭安全攝影機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Smart Home Security Camera Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

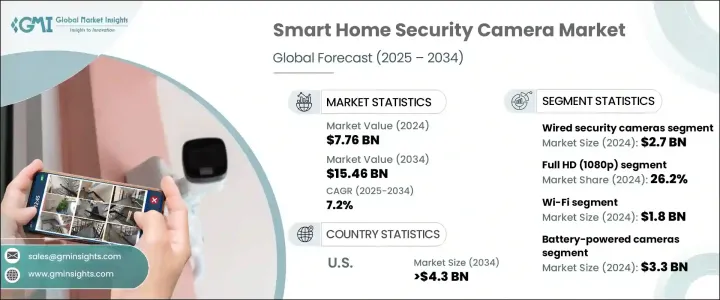

2024 年全球智慧家庭安全攝影機市場價值為 77.6 億美元,預計 2025 年至 2034 年的複合年成長率為 7.2%。市場擴張主要受到智慧家庭設備日益普及和安全問題日益加劇的推動。智慧攝影機、鎖和運動感測器正變得越來越重要,它們使用戶能夠遠端監控他們的家,同時與家庭自動化系統無縫整合。 5G網路和物聯網技術的廣泛應用,顯著提升了智慧安防系統的效能。此外,智慧型手機和語音助理用戶數量的不斷成長繼續支持市場成長,使安全解決方案能夠無縫運作。日益嚴重的安全威脅進一步刺激了對具有高清攝影機、雲端儲存和基於人工智慧的威脅偵測功能的先進監控解決方案的需求。

市場分為有線和無線安全攝影機。 2024 年,有線安全攝影機的估值為 27 億美元。它們的受歡迎程度源於增強的可靠性、最佳的電源供應和卓越的視訊品質。此外,乙太網路供電 (PoE) 技術簡化了多個安全設備的安裝。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 77.6億美元 |

| 預測值 | 154.6億美元 |

| 複合年成長率 | 7.2% |

按解析度,市場包括高清 (720p)、全高清 (1080p)、2K 和 4K 以上攝影機。 2024 年,全高清 (1080p) 攝影機佔據了 26.2% 的市場。由於其可靠的連接性以及與網路錄影機和集中監控系統的兼容性,它們被廣泛應用於大型物業和商業場所。

市場還根據連接選項進行分類,包括 Wi-Fi、藍牙和 ZigBee。 2024 年,支援 Wi-Fi 的安全攝影機以 18 億美元的市場規模領先。其日益普及的原因是安裝簡單、與家庭網路的無縫整合以及遠端存取。網狀和雙頻 Wi-Fi 技術的發展提高了可靠性,同時減少了連線問題和延遲。

就電源而言,市場包括電池供電、插入式和太陽能供電的相機。電池供電的攝影機佔據了主導地位,2024 年的估值為 33 億美元。由於太陽能充電、人工智慧驅動的能源管理和鋰離子電池技術的進步,室內和室外使用對電池供電攝影機的需求都在不斷成長。人們對攜帶式、DIY 型安全解決方案的日益青睞繼續推動其採用。

在應用方面,室內安全正在經歷快速成長,預計複合年成長率為 10.4%。消費者和企業都擴大投資室內監控解決方案,特別是嬰兒和寵物監控以及老年人照護。人工智慧運動偵測、臉部辨識和雲端儲存進一步增強了這些安全解決方案的吸引力。

配銷通路部分包括線上銷售、超市、大賣場、專賣店和電子產品零售商。 2024 年,線上銷售將成為主導市場,創造 30 億美元的銷售額。人們對電子商務日益成長的偏好是由有競爭力的定價、產品多樣性和便利的價格比較所推動的。

由於犯罪率上升和對智慧安全解決方案的需求增加,預計到 2034 年美國市場規模將超過 43 億美元。安全系統與家庭自動化和保險激勵措施的結合進一步支持了市場擴張。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 智慧家庭設備的普及率不斷提高

- 安全擔憂加劇

- 技術進步

- 改進的連接性和即時監控

- DIY 安裝,經濟實惠

- 產業陷阱與挑戰

- 高昂的初始成本和訂閱費用

- 網路連線受限和頻寬問題

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 有線安全攝影機

- 無線安全攝影機

第6章:市場估計與預測:依決議,2021 年至 2034 年

- 主要趨勢

- 高清(720p)

- 全高清 (1080p)

- 2K

- 4K 以上

第7章:市場估計與預測:依連結性,2021 年至 2034 年

- 主要趨勢

- 無線上網

- 藍牙

- Zigbee

- 其他

第8章:市場估計與預測:按電源,2021 年至 2034 年

- 主要趨勢

- 電池供電相機

- 插入式電源攝影機

- 太陽能攝影機

第9章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 室內安防

- 戶外安全

第 10 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 網上銷售

- 電子商務平台

- 品牌網站

- 超市/大賣場

- 專賣店

- 電子產品商店

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳新銀行

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第12章:公司簡介

- Abode Systems, Inc.

- ADT Inc.

- Arlo Technologies, Inc.

- Blink

- Canary Connect, Inc.

- D-Link Corporation

- Ecobee

- Eufy

- Frontpoint Security Solutions, LLC

- Google Nest

- Hikvision Digital Technology

- Lorex

- Reolink

- Ring

- Samsung Electronics Co., Ltd.

- SimpliSafe

- Synology

- TP-Link

- Ubiquiti Inc.

- Vivint Smart Home

- Wyze Labs, Inc.

- Xiaomi Inc.

- YI Technology

- Zmodo

The Global Smart Home Security Camera Market was valued at USD 7.76 billion in 2024 and is projected to grow at a CAGR of 7.2% from 2025 to 2034. Market expansion is largely driven by the increasing adoption of smart home devices and heightened security concerns. Smart cameras, locks, and motion sensors are becoming essential, allowing users to monitor their homes remotely while seamlessly integrating with home automation systems. The widespread adoption of 5G networks and IoT technology has significantly enhanced the performance of smart security systems. Moreover, the growing number of smartphone and voice assistant users continues to support market growth, enabling seamless operation of security solutions. Rising security threats have further fueled the need for advanced surveillance solutions featuring high-definition cameras, cloud storage, and AI-based threat detection.

The market is divided into wired and wireless security cameras. In 2024, wired security cameras held a valuation of USD 2.7 billion. Their popularity stems from enhanced reliability, optimal power supply, and superior video quality. Additionally, Power over Ethernet (PoE) technology has simplified the installation of multiple security devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.76 Billion |

| Forecast Value | $15.46 Billion |

| CAGR | 7.2% |

By resolution, the market includes HD (720p), Full HD (1080p), 2K, and 4K & above cameras. Full HD (1080p) cameras accounted for 26.2% of the market share in 2024. They are widely used in large properties and commercial settings due to their reliable connectivity and compatibility with network video recorders and centralized monitoring systems.

The market is also categorized by connectivity options, including Wi-Fi, Bluetooth, and ZigBee. Wi-Fi-enabled security cameras led the market with USD 1.8 billion in 2024. Their increasing adoption is attributed to easy installation, seamless integration with home networks, and remote access. The development of mesh and dual-band Wi-Fi technology has improved reliability while reducing connectivity issues and lag.

Regarding power sources, the market consists of battery-powered, plug-in, and solar-powered cameras. Battery-powered cameras dominated the segment with a valuation of USD 3.3 billion in 2024. Their demand is rising for both indoor and outdoor use due to advancements in solar charging, AI-driven energy management, and lithium-ion battery technology. The increasing preference for portable, DIY-friendly security solutions continues to drive adoption.

In terms of application, indoor security is witnessing rapid growth, with a projected CAGR of 10.4%. Consumers and businesses alike are increasingly investing in indoor surveillance solutions, particularly for baby and pet monitoring, as well as elderly care. AI-powered motion detection, facial recognition, and cloud storage further enhance the appeal of these security solutions.

The distribution channel segment includes online sales, supermarkets, hypermarkets, specialty stores, and electronics retailers. Online sales emerged as the dominant segment in 2024, generating USD 3 billion. The growing preference for e-commerce is driven by competitive pricing, product variety, and convenient price comparisons.

The U.S. market is expected to exceed USD 4.3 billion by 2034, fueled by rising crime rates and increased demand for smart security solutions. The integration of security systems with home automation and insurance incentives is further supporting market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of smart home devices

- 3.2.1.2 Rising security concerns

- 3.2.1.3 Technological advancements

- 3.2.1.4 Improved connectivity and real-time monitoring

- 3.2.1.5 DIY installation and cost-effectiveness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost and subscription fees

- 3.2.2.2 Limited internet connectivity and bandwidth issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Mn)

- 5.1 Key trends

- 5.2 Wired security cameras

- 5.3 Wireless security cameras

Chapter 6 Market Estimates and Forecast, By Resolution, 2021 – 2034 (USD Mn)

- 6.1 Key trends

- 6.2 HD (720p)

- 6.3 Full HD (1080p)

- 6.4 2K

- 6.5 4K & Above

Chapter 7 Market Estimates and Forecast, By Connectivity, 2021 – 2034 (USD Mn)

- 7.1 Key trends

- 7.2 Wi-Fi

- 7.3 Bluetooth

- 7.4 Zigbee

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Power Source, 2021 – 2034 (USD Mn)

- 8.1 Key trends

- 8.2 Battery-powered cameras

- 8.3 Plug-in power cameras

- 8.4 Solar-powered cameras

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Mn)

- 9.1 Key trends

- 9.2 Indoor security

- 9.3 Outdoor security

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Mn)

- 10.1 Key trends

- 10.2 Online sales

- 10.2.1 E-commerce platforms

- 10.2.2 Brand websites

- 10.3 Supermarkets/Hypermarkets

- 10.4 Specialty stores

- 10.5 Electronics stores

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Abode Systems, Inc.

- 12.2 ADT Inc.

- 12.3 Arlo Technologies, Inc.

- 12.4 Blink

- 12.5 Canary Connect, Inc.

- 12.6 D-Link Corporation

- 12.7 Ecobee

- 12.8 Eufy

- 12.9 Frontpoint Security Solutions, LLC

- 12.10 Google Nest

- 12.11 Hikvision Digital Technology

- 12.12 Lorex

- 12.13 Reolink

- 12.14 Ring

- 12.15 Samsung Electronics Co., Ltd.

- 12.16 SimpliSafe

- 12.17 Synology

- 12.18 TP-Link

- 12.19 Ubiquiti Inc.

- 12.20 Vivint Smart Home

- 12.21 Wyze Labs, Inc.

- 12.22 Xiaomi Inc.

- 12.23 YI Technology

- 12.24 Zmodo

營運應用的定價模型:全球市場預測(2024-2029)

營運應用的定價模型:全球市場預測(2024-2029) 2025 年無線家庭保全攝影機全球市場報告

2025 年無線家庭保全攝影機全球市場報告 無線家庭安全攝影機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

無線家庭安全攝影機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 安全攝影機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

安全攝影機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 全球保全攝影機市場(2025-2029)

全球保全攝影機市場(2025-2029) 全球智慧家庭保全攝影機市場:市場規模、佔有率和趨勢分析(按技術、應用、地區和細分市場,2025-2030 年)

全球智慧家庭保全攝影機市場:市場規模、佔有率和趨勢分析(按技術、應用、地區和細分市場,2025-2030 年) 北美智慧家庭保全攝影機市場規模、佔有率和趨勢分析報告:按產品、應用、國家和細分市場進行預測,2025-2030 年

北美智慧家庭保全攝影機市場規模、佔有率和趨勢分析報告:按產品、應用、國家和細分市場進行預測,2025-2030 年 家庭安全攝影機市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分、按產品、類型、解析度、服務、地區、競爭,2019-2029F 2019-2029F

家庭安全攝影機市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分、按產品、類型、解析度、服務、地區、競爭,2019-2029F 2019-2029F PoE保全攝影機市場:按類型、應用、解析度、組件、連接性、最終用戶、技術、電源、分銷管道 - 2025-2030 年全球預測

PoE保全攝影機市場:按類型、應用、解析度、組件、連接性、最終用戶、技術、電源、分銷管道 - 2025-2030 年全球預測 智慧家庭保全攝影機市場:攝影機形狀、特殊功能、可見範圍、音訊功能、鏡頭類型、耐候性 - 2025-2030 年全球預測

智慧家庭保全攝影機市場:攝影機形狀、特殊功能、可見範圍、音訊功能、鏡頭類型、耐候性 - 2025-2030 年全球預測