|

市場調查報告書

商品編碼

1698268

電動商用車牽引馬達市場機會、成長動力、產業趨勢分析及2025-2034年預測Electric Commercial Vehicle Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

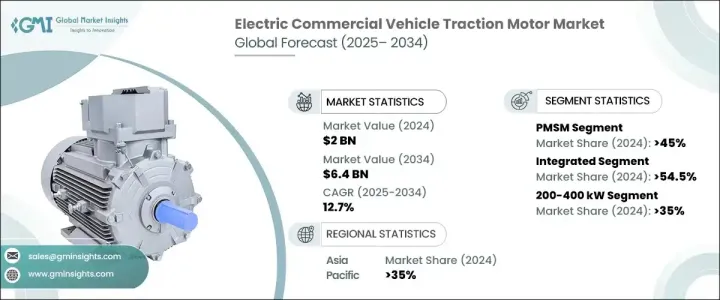

2024 年全球電動商用車牽引馬達市場價值 20 億美元,預計 2025 年至 2034 年的複合年成長率為 12.7%。在效率、耐用性和性能進步的推動下,該行業正在快速發展。新興電機技術,包括永磁同步馬達 (PMSM)、開關磁阻電機 (SRM) 和橫向磁通電機,正在提高能量輸出,同時最大限度地減少浪費。配備先進冷卻系統的碳化矽 (SiC) 逆變器進一步最佳化了能源使用、延長了行駛里程並提高了整體性能。輕質材料和緊湊的設計提高了扭矩密度,使馬達成為重型商用車的理想選擇。同時,快速充電基礎設施和電池效率的發展正在提高電動卡車和巴士在城市和長途應用中的實用性。充電站數量的增加大大減少了車隊營運商的等待時間。

電動商用車牽引馬達市場按馬達類型、車軸結構、車輛類別和額定功率進行細分。 PMSM憑藉其高能源效率、緊湊的結構和卓越的功率輸出,將在2024年佔總收入的45%以上。這些電機具有出色的扭矩密度和再生煞車,使其成為電動卡車和公共汽車的首選。在車軸架構的基礎上,整合式電子車軸在 2024 年佔據 54.5% 的收入佔有率,引領市場。這些系統將馬達、逆變器和變速箱整合到一個單元中,從而減輕了重量,提高了能源效率,並最佳化了電動卡車和貨車內的空間。中央驅動裝置對於高扭矩和耐用性至關重要的重型應用來說仍然至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 20億美元 |

| 預測值 | 64億美元 |

| 複合年成長率 | 12.7% |

按車輛類別分類,受嚴格的排放法規和車隊電氣化程度不斷提高的推動,中型和重型卡車將在 2024 年佔據市場主導地位。這些卡車需要強大的高扭矩牽引電機,以在高負載下保持效率。先進的熱管理和模組化馬達設計進一步提高了可靠性並降低了整體擁有成本。隨著採用率的提高,製造商正在開發可擴展的馬達平台,以實現與各個商用電動車領域的無縫整合。

根據額定功率,200-400 kW 部分在 2024 年佔據最大佔有率,貢獻總收入的 35% 以上。該系列電機非常適合長途電動卡車和公共汽車,支援永續物流和貨運。 100kW以下馬達主要服務於小型電動廂型車和城市配送車,而100-200kW馬達則廣泛應用於輕型和中型卡車。 400 kW 以上的等級專門用於高性能應用,包括氫燃料電池汽車和電動採礦卡車。

2024年,亞太地區佔據最大的市場佔有率,佔全球產業的35%以上。中國成為主導者,預計到 2034 年將達到 18 億美元,這得益於政策激勵、技術進步以及其在電池和稀土材料生產方面的優勢。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 馬達製造商

- 電池供應商

- 原始設備製造商

- 電力電子供應商

- 充電基礎設施供應商

- 供應商格局

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 新創企業融資分析

- 監管格局

- 衝擊力

- 成長動力

- 電動商用車(ECVS)的普及率不斷上升

- 嚴格的排放法規與永續發展目標

- 馬達效率和技術的進步

- 充電基礎設施的擴展和電池的進步

- 產業陷阱與挑戰

- 車隊營運商的初始成本高且投資回報率有限

- 供應鍊和原料限制

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按汽車,2021 - 2034 年

- 主要趨勢

- 交流感應電機

- 永磁同步馬達(PMSM)

- 開關磁阻馬達(SRM)

- 直流馬達

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 皮卡車

- 中型和重型卡車

- 貨車

- 公車

第7章:市場估計與預測:依功率等級,2021 年至 2034 年

- 主要趨勢

- 小於100千瓦

- 100-200千瓦

- 200-400千瓦

- 400度以上

第8章:市場估計與預測:按車橋架構,2021 - 2034 年

- 主要趨勢

- 融合的

- 中央驅動單元

第9章:市場估計與預測:依傳輸方式,2021 - 2034 年

- 主要趨勢

- 單速驅動

- 多速驅動

第10章:市場估計與預測:依設計,2021 - 2034 年

- 主要趨勢

- 徑向通量

- 軸向通量

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第12章:公司簡介

- ABB

- Allison Transmission

- BorgWarner

- Bosch

- Continental

- Dana

- Danfoss Editron

- General Electric

- Hitachi Automotive

- Magna

- Mitsubishi Electric

- Nidec

- Siemens

- Skoda Transportation

- Toshiba

- Valeo

- Wabtec

- Wolong Electric

- Yaskawa Electric

- ZF

The Global Electric Commercial Vehicle Traction Motor Market was valued at USD 2 billion in 2024 and is projected to grow at a CAGR of 12.7% from 2025 to 2034. The industry is rapidly evolving, driven by advancements in efficiency, durability, and performance. Emerging motor technologies, including permanent magnet synchronous motors (PMSM), switched reluctance motors (SRM), and lateral flux motors, are enhancing energy output while minimizing waste. Silicon carbide (SiC) inverters with advanced cooling systems are further optimizing energy use, extending driving range, and improving overall performance. Lightweight materials and compact designs are increasing torque density, making motors ideal for heavy-duty commercial vehicles. Meanwhile, developments in fast-charging infrastructure and battery efficiency are improving the practicality of electric trucks and buses for both urban and long-haul applications. The increasing number of charging stations is significantly reducing wait times for fleet operators.

The electric commercial vehicle traction motor market is segmented by motor type, axle architecture, vehicle category, and power rating. PMSM accounted for over 45% of total revenue in 2024 due to its high energy efficiency, compact structure, and superior power output. These motors offer excellent torque density and regenerative braking, making them the preferred choice for electric trucks and buses. On the basis of axle architecture, integrated e-axles led the market with a 54.5% revenue share in 2024. These systems integrate motors, inverters, and transmissions into a single unit, reducing weight, increasing energy efficiency, and optimizing space within electric trucks and vans. Central drive units remain essential for heavy-duty applications where high torque and durability are critical.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 12.7% |

By vehicle category, medium and heavy-duty trucks dominated the market in 2024, driven by strict emissions regulations and increasing fleet electrification. These trucks require powerful, high-torque traction motors that maintain efficiency under demanding loads. Advanced thermal management and modular motor designs are further improving reliability and reducing the total cost of ownership. As adoption grows, manufacturers are developing scalable motor platforms for seamless integration across various commercial EV segments.

Based on power rating, the 200-400 kW segment held the largest share in 2024, contributing over 35% of total revenue. Motors in this range are ideal for long-haul electric trucks and buses, supporting sustainable logistics and freight transport. Motors below 100 kW primarily serve compact electric vans and urban delivery vehicles, while 100-200 kW motors are widely used in light and medium-duty trucks. The above 400 kW category is reserved for high-performance applications, including hydrogen fuel cell-powered vehicles and electric mining trucks.

The Asia Pacific region held the largest share of the market in 2024, accounting for over 35% of the global industry. China emerged as the dominant player, projected to reach USD 1.8 billion by 2034, fueled by policy incentives, technological advancements, and its stronghold in battery and rare-earth material production.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Motor manufacturers

- 3.1.2 Battery suppliers

- 3.1.3 OEMs

- 3.1.4 Power electronics suppliers

- 3.1.5 Charging infrastructure providers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Startup funding analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of electric commercial vehicles (ECVS)

- 3.9.1.2 Stringent emission regulations & sustainability goals

- 3.9.1.3 Advancements in motor efficiency & technology

- 3.9.1.4 Expansion of charging infrastructure & battery advancements

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial cost & limited ROI for fleet operators

- 3.9.2.2 Supply chain & raw material constraints

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Motor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 AC induction motors

- 5.3 Permanent magnet synchronous motors (PMSM)

- 5.4 Switched reluctance motors (SRM)

- 5.5 DC motors

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Pickups trucks

- 6.3 Medium and heavy-duty trucks

- 6.4 Vans

- 6.5 Buses

Chapter 7 Market Estimates & Forecast, By Power Rating, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Less than 100 kW

- 7.3 100-200 kW

- 7.4 200-400 kW

- 7.5 Above 400 kW

Chapter 8 Market Estimates & Forecast, By Axle Architecture, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Integrated

- 8.3 Central drive unit

Chapter 9 Market Estimates & Forecast, By Transmission, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Single-speed drive

- 9.3 Multi-speed drive

Chapter 10 Market Estimates & Forecast, By Design, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Radial flux

- 10.3 Axial flux

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 Allison Transmission

- 12.3 BorgWarner

- 12.4 Bosch

- 12.5 Continental

- 12.6 Dana

- 12.7 Danfoss Editron

- 12.8 General Electric

- 12.9 Hitachi Automotive

- 12.10 Magna

- 12.11 Mitsubishi Electric

- 12.12 Nidec

- 12.13 Siemens

- 12.14 Skoda Transportation

- 12.15 Toshiba

- 12.16 Valeo

- 12.17 Wabtec

- 12.18 Wolong Electric

- 12.19 Yaskawa Electric

- 12.20 ZF

電動商用車:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

電動商用車:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 電動商用車市場:全球按車輛類型、推進系統、續航里程、電池類型、功率輸出、電池容量、組件、最終用戶、車輛配置和地區分類 - 預測至 2030 年

電動商用車市場:全球按車輛類型、推進系統、續航里程、電池類型、功率輸出、電池容量、組件、最終用戶、車輛配置和地區分類 - 預測至 2030 年 電動工業車輛市場-2025-2035年全球產業分析、規模、佔有率、成長、趨勢及預測

電動工業車輛市場-2025-2035年全球產業分析、規模、佔有率、成長、趨勢及預測 電動商用車市場:未來預測(2025-2030)

電動商用車市場:未來預測(2025-2030) 電動商用車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

電動商用車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2025 年至 2029 年全球電動商用車 (ECV) 市場電力LCV (輕型商旅車) 市場評估:車輛類型·推動區分·各地區的機會及預測 (2018-2032年)

2025 年至 2029 年全球電動商用車 (ECV) 市場電力LCV (輕型商旅車) 市場評估:車輛類型·推動區分·各地區的機會及預測 (2018-2032年) 輕型商用車電氣化市場:按車輛類型和推進類型分類的全球預測 - 2025-2030電動商用車市場:按組件、按車輛類型、按推進類型、按電池容量、按功率、按自動化、按里程、按最終用戶 - 2025-2030 年全球預測電動商用車牽引馬達市場:按車型、馬達類型、額定功率、設計分類 - 全球預測 2025-2030

輕型商用車電氣化市場:按車輛類型和推進類型分類的全球預測 - 2025-2030電動商用車市場:按組件、按車輛類型、按推進類型、按電池容量、按功率、按自動化、按里程、按最終用戶 - 2025-2030 年全球預測電動商用車牽引馬達市場:按車型、馬達類型、額定功率、設計分類 - 全球預測 2025-2030