|

市場調查報告書

商品編碼

1698286

子宮內膜異位症治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Endometriosis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

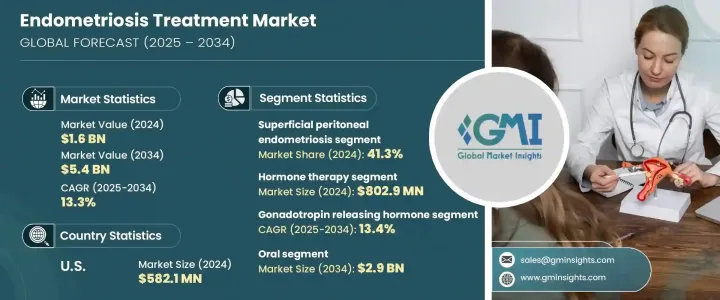

全球子宮內膜異位症治療市場價值 16 億美元,預計 2025 年至 2034 年期間的複合年成長率將達到 13.3%,這得益於人們認知的提高、醫療治療的進步以及醫療保健可及性的提高。加強教育和早期診斷工作正在幫助更多人在早期階段尋求醫療干預,從而增加對有效治療方案的需求。醫療保健提供者正專注於綜合管理策略,不僅解決即時症狀緩解問題,而且還改善長期健康結果。政府措施和倡導團體在消除對這種疾病的恥辱感、鼓勵更多女性尋求治療方面發揮關鍵作用。研發投入的不斷增加也有助於擴大治療選擇,製藥公司正在探索創新療法以加強對患者的照護。

醫療支出的增加和保險覆蓋範圍的擴大使得子宮內膜異位症的治療變得更加容易,更多的患者能夠及時得到醫療救治。隨著宣傳活動不斷強調未治療的子宮內膜異位症的長期影響,越來越多的患者正在尋求專門的護理。對非侵入性治療方案的需求激增,尤其是尋求手術介入替代方案的年輕患者。醫療保健專業人員正在努力整合個人化治療方法,以滿足個別患者的需求,進一步推動市場向前發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 16億美元 |

| 預測值 | 54億美元 |

| 複合年成長率 | 13.3% |

根據疾病類型,市場細分為不同的形式,其中淺層腹膜子宮內膜異位症部分在 2024 年佔據 41.3% 的主導佔有率。這種形式的疾病以腹膜表面病變為特徵,比深層子宮內膜異位症更廣泛且更容易辨識。因此,這種疾病的診斷頻率更高,從而需要更快的醫療干預,並且針對這種類型的治療的需求更高。早期檢測和管理淺層腹膜子宮內膜異位症的能力使其成為市場上最普遍的領域。

子宮內膜異位症的治療方案主要分為荷爾蒙療法和疼痛管理,其中荷爾蒙療法在 2024 年產生 8.029 億美元的收入。醫生通常會開立避孕藥、黃體素和荷爾蒙調節藥物來緩解骨盆腔疼痛和月經過多等症狀。這些治療方法因其有效性、易於實施以及能夠改善患者的生活品質而越來越受歡迎。越來越多的人選擇荷爾蒙療法,因為它們可以緩解症狀,而無需進行侵入性手術。

受公共衛生計畫和宣傳活動不斷加強的推動,美國子宮內膜異位症治療市場規模在 2024 年達到 5.821 億美元。努力教育人們了解子宮內膜異位症的症狀和影響,鼓勵人們做出積極的醫療保健決策,並減少圍繞疾病的恥辱感。醫學研究的進步、對生殖健康的更加關注以及專業醫療服務的改善正在進一步加速市場擴張。隨著對創新治療方案的需求不斷成長,製藥公司和醫療保健提供者正在努力透過更先進、更有針對性的治療方法來改善患者的治療效果。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 子宮內膜異位症的盛行率和認知度不斷上升

- 診斷技術的進步

- 增加政府資金和舉措

- 產業陷阱與挑戰

- 先進治療成本高

- 成長動力

- 成長潛力分析

- 監管格局

- 管道分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依疾病類型,2021 年至 2034 年

- 主要趨勢

- 表淺腹膜子宮內膜異位症

- 卵巢子宮內膜異位症

- 深部浸潤性子宮內膜異位症

- 其他疾病類型

第6章:市場估計與預測:依治療類型,2021 年至 2034 年

- 主要趨勢

- 荷爾蒙治療

- 止痛藥

第7章:市場估計與預測:依藥物類別,2021 年至 2034 年

- 主要趨勢

- 促性腺激素釋放激素

- 非類固醇抗發炎藥

- 口服避孕藥

- 其他藥物類

第8章:市場估計與預測:依管理路線,2021 年至 2034 年

- 主要趨勢

- 口服

- 注射劑

- 其他給藥途徑

第9章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 醫院藥房

- 零售藥局

- 網路藥局

第10章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- AbbVie

- Astellas Pharma

- AstraZeneca

- Bayer

- Eli Lilly and Company

- ObsEva

- Pfizer

- Teva Pharmaceutical Industries

- TerSera Therapeutics

- Zydus Healthcare Limited

The Global Endometriosis Treatment Market, valued at USD 1.6 billion in 2024, is projected to expand at a CAGR of 13.3% from 2025 to 2034, driven by rising awareness, advances in medical treatments, and improved healthcare accessibility. Increased education and early diagnosis efforts are helping more individuals seek medical intervention at earlier stages, boosting demand for effective therapeutic solutions. Healthcare providers are focusing on comprehensive management strategies that not only address immediate symptom relief but also improve long-term health outcomes. Government initiatives and advocacy groups are playing a critical role in destigmatizing the condition, encouraging more women to pursue treatment options. The growing investment in research and development is also contributing to the expansion of treatment choices, with pharmaceutical companies exploring innovative therapies to enhance patient care.

Rising healthcare expenditure and improved insurance coverage have made endometriosis treatments more accessible, allowing more patients to receive timely medical attention. As awareness campaigns continue to highlight the long-term impact of untreated endometriosis, an increasing number of patients are seeking specialized care. The demand for non-invasive treatment options has surged, particularly among younger patients looking for alternatives to surgical interventions. Healthcare professionals are working to integrate personalized treatment approaches that cater to individual patient needs, further driving the market forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 13.3% |

By disease type, the market is segmented into different forms, with the superficial peritoneal endometriosis segment holding a dominant 41.3% share in 2024. This form of the condition, characterized by lesions on the peritoneal surface, is widespread and more easily identifiable than deeper forms of endometriosis. As a result, it is diagnosed more frequently, leading to quicker medical intervention and higher demand for treatments targeting this type. The ability to detect and manage superficial peritoneal endometriosis early has positioned it as the most prevalent segment within the market.

Endometriosis treatment options are primarily divided into hormone therapy and pain management, with hormone therapy generating USD 802.9 million in 2024. Physicians commonly prescribe contraceptives, progestins, and hormone-modulating drugs to alleviate symptoms such as pelvic pain and excessive menstrual bleeding. These treatments are gaining popularity due to their effectiveness, ease of administration, and ability to improve patients' quality of life. More individuals are opting for hormone-based therapies as they provide symptom relief without the need for invasive procedures.

The United States endometriosis treatment market accounted for USD 582.1 million in 2024, fueled by increasing public health initiatives and awareness campaigns. Efforts to educate individuals about the symptoms and implications of endometriosis have encouraged proactive healthcare decisions and reduced stigma surrounding the condition. Advancements in medical research, a stronger focus on reproductive health, and improved access to specialized healthcare services are further accelerating market expansion. As demand for innovative treatment solutions continues to grow, pharmaceutical companies and healthcare providers are working to enhance patient outcomes through more advanced and targeted therapeutic approaches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence and awareness of endometriosis

- 3.2.1.2 Advancement in diagnostic techniques

- 3.2.1.3 Increased government fundings and initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Superficial peritoneal endometriosis

- 5.3 Ovarian endometriomas

- 5.4 Deep infiltrating endometriosis

- 5.5 Other disease types

Chapter 6 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hormone therapy

- 6.3 Pain medication

Chapter 7 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Gonadotropin releasing hormone

- 7.3 NSAIDs

- 7.4 Oral contraceptive

- 7.5 Other drug class

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Other routes of administration

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Astellas Pharma

- 11.3 AstraZeneca

- 11.4 Bayer

- 11.5 Eli Lilly and Company

- 11.6 ObsEva

- 11.7 Pfizer

- 11.8 Teva Pharmaceutical Industries

- 11.9 TerSera Therapeutics

- 11.10 Zydus Healthcare Limited

子宮內膜異位症治療市場規模、佔有率、趨勢分析報告,按治療類型、藥物類別、給藥途徑、分銷管道、地區、細分預測,2025-2030 年

子宮內膜異位症治療市場規模、佔有率、趨勢分析報告,按治療類型、藥物類別、給藥途徑、分銷管道、地區、細分預測,2025-2030 年 美國子宮內膜異位症治療市場規模、佔有率、趨勢分析報告,按治療類型、藥物類別、給藥途徑、分銷管道、細分預測,2025-2030 年

美國子宮內膜異位症治療市場規模、佔有率、趨勢分析報告,按治療類型、藥物類別、給藥途徑、分銷管道、細分預測,2025-2030 年 2025-2033 年子宮內膜異位症市場報告(按類型、診斷和治療、最終用戶和地區)

2025-2033 年子宮內膜異位症市場報告(按類型、診斷和治療、最終用戶和地區) 子宮內膜異位症藥物市場:按藥物類型、治療類型、分銷管道分類 - 全球預測 2025-2030

子宮內膜異位症藥物市場:按藥物類型、治療類型、分銷管道分類 - 全球預測 2025-2030 子宮內膜異位症藥物市場:按藥物類型、給藥途徑、患者特徵和最終用戶分類 - 全球預測 2025-2030

子宮內膜異位症藥物市場:按藥物類型、給藥途徑、患者特徵和最終用戶分類 - 全球預測 2025-2030 全球子宮內膜異位症藥物市場規模(按產品、應用、地區、範圍和預測)

全球子宮內膜異位症藥物市場規模(按產品、應用、地區、範圍和預測) 子宮內膜異位症治療市場 - 全球產業分析、規模、佔有率、成長、趨勢和預測,2024-2034 年

子宮內膜異位症治療市場 - 全球產業分析、規模、佔有率、成長、趨勢和預測,2024-2034 年 全球子宮內膜異位症治療市場:預測(2024-2029)

全球子宮內膜異位症治療市場:預測(2024-2029) 子宮內膜異位症市場報告:2030 年趨勢、預測與競爭分析

子宮內膜異位症市場報告:2030 年趨勢、預測與競爭分析 子宮內膜異位症治療全球市場研究報告——2023-2030 年行業分析、規模、份額、增長、趨勢和預測

子宮內膜異位症治療全球市場研究報告——2023-2030 年行業分析、規模、份額、增長、趨勢和預測