|

市場調查報告書

商品編碼

1698296

表觀遺傳學診斷市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Epigenetics Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

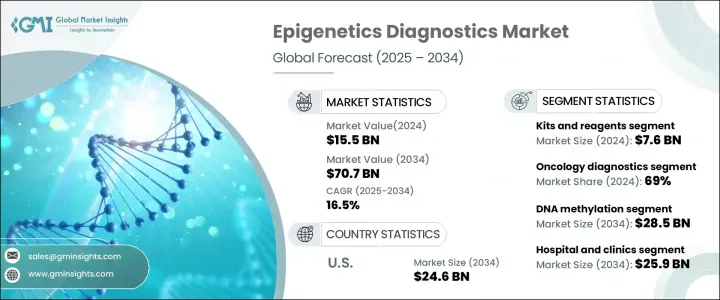

2024 年全球表觀遺傳學診斷市場價值為 155 億美元,預計 2025 年至 2034 年期間的複合年成長率將達到 16.5%。這一快速擴張很大程度上是由於人們越來越認知到表觀遺傳修飾是疾病發展和進展的關鍵因素。隨著對 DNA 甲基化、組蛋白修飾和非編碼 RNA 在各種健康狀況中的作用的研究不斷深入,對先進診斷工具的需求呈指數級成長。

近年來,精準醫療的廣泛應用,加上分子診斷技術的進步,大大加速了市場擴張。人工智慧和機器學習在表觀遺傳分析中的融合,進一步提高了診斷解決方案的準確性和效率。此外,大型製藥和生物技術公司正在大力投資研發新型表觀遺傳生物標記物,進一步推動該產業的發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 155億美元 |

| 預測值 | 707億美元 |

| 複合年成長率 | 16.5% |

研究機構和醫療保健提供者之間日益密切的合作也在將科學發現轉化為現實世界的臨床應用方面發揮關鍵作用。旨在改善早期疾病檢測和個人化醫療的資金和政府措施的增加正在推動該領域的創新。隨著癌症和神經退化性疾病等慢性疾病的增加,表觀遺傳學診斷的重要性不斷增加,為未來十年市場持續擴張奠定了基礎。

市場分為主要產品類別,包括試劑盒和試劑、儀器、軟體和服務。 2024 年,全球此類產品市場規模將達到 134 億美元,其中試劑盒和試劑部分佔據主導地位,規模達 76 億美元。這些診斷工具已成為臨床應用、學術研究和藥物開發中不可或缺的工具。它們越來越受歡迎,源自於其方便用戶使用的設計、增強的檢測靈敏度、自動化能力以及與下一代定序 (NGS) 和聚合酶鍊式反應 (PCR) 等尖端平台的兼容性。隨著業界向更高通量和更具成本效益的解決方案邁進,對可靠、高效的試劑盒的需求持續成長。

表觀遺傳學診斷的應用領域分為腫瘤學和非腫瘤學領域,其中腫瘤學在 2024 年將佔 69% 的佔有率。該領域的主導地位主要歸因於對早期癌症檢測的需求日益成長,以及表觀遺傳生物標記在診斷和治療各種惡性腫瘤中的重要性日益增加。 DNA甲基化模式、組蛋白修飾和染色質重塑的變化已成為癌症發展的關鍵指標,從而可以實現更精確和個人化的治療方法。隨著全球癌症負擔的增加和生物標記研究的不斷進步,腫瘤學領域仍然是市場成長的主要驅動力。

預計到 2034 年,美國表觀遺傳學診斷市場將以 16.5% 的複合年成長率成長,在預測期結束時達到 246 億美元。由於其強大的醫療保健基礎設施、廣泛的研發計劃以及精準醫療的早期採用,該國仍然是該行業的領導者。包括美國國立衛生研究院 (NIH) 在內的政府機構繼續資助表觀遺傳學的突破性研究,進一步加速創新和商業化。慢性病盛行率的上升、生物技術公司的投資增加以及有利的監管政策進一步鞏固了美國在全球表觀遺傳學診斷領域的主導地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 癌症和慢性病發生率不斷上升

- 表觀基因組學研究和技術的進展

- 非侵入性診斷的需求不斷成長

- 產業陷阱與挑戰

- 表觀遺傳診斷技術成本高昂

- 測驗方法標準化程度有限

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021-2034

- 主要趨勢

- 試劑盒和試劑

- 儀器

- 軟體和服務

第6章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 腫瘤診斷

- 非腫瘤診斷

第7章:市場估計與預測:按技術,2021-2034 年

- 主要趨勢

- DNA甲基化

- 組蛋白甲基化

- MicroRNA修飾

- 染色質結構

- 其他技術

第8章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 醫院和診所

- 製藥和生物技術公司

- 診斷實驗室

- 其他最終用途

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Abcam

- Agilent Technologies

- Diagenode

- Dovetail Genomics

- Element Biosciences

- Illumina

- Merck

- New England Biolabs

- PacBio

- Promega

- QIAGEN

- Roche Diagnostics

- Thermo Fisher Scientific

- Zymo Research

The Global Epigenetics Diagnostics Market was valued at USD 15.5 billion in 2024 and is poised to register a CAGR of 16.5% from 2025 to 2034. This rapid expansion is largely fueled by the increasing recognition of epigenetic modifications as key contributors to disease development and progression. As research deepens into the role of DNA methylation, histone modifications, and non-coding RNAs in various health conditions, the demand for advanced diagnostic tools is rising exponentially.

In recent years, the widespread adoption of precision medicine, coupled with technological advancements in molecular diagnostics, has significantly accelerated market expansion. The integration of artificial intelligence and machine learning in epigenetic analysis has further enhanced the accuracy and efficiency of diagnostic solutions. Additionally, major pharmaceutical and biotechnology companies are investing heavily in R&D to develop novel epigenetic biomarkers, further propelling the industry forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.5 Billion |

| Forecast Value | $70.7 Billion |

| CAGR | 16.5% |

Growing collaborations between research institutions and healthcare providers are also playing a pivotal role in translating scientific discoveries into real-world clinical applications. The increased availability of funding and government initiatives aimed at improving early disease detection and personalized medicine is driving innovation in the field. With the rise in chronic diseases, including cancer and neurodegenerative disorders, the relevance of epigenetic diagnostics continues to grow, positioning the market for sustained expansion over the next decade.

The market is segmented into key product categories, including kits and reagents, instruments, software, and services. In 2024, the global market for these products reached USD 13.4 billion, with the kits and reagents segment dominating at USD 7.6 billion. These diagnostic tools have become indispensable in clinical applications, academic research, and pharmaceutical development. Their growing popularity stems from their user-friendly designs, enhanced assay sensitivity, automation capabilities, and compatibility with cutting-edge platforms like next-generation sequencing (NGS) and polymerase chain reaction (PCR). As the industry moves toward more high-throughput and cost-effective solutions, the demand for reliable and efficient kits continues to escalate.

The application landscape of epigenetics diagnostics is categorized into oncology and non-oncology segments, with oncology commanding a substantial 69% share in 2024. The dominance of this segment is largely attributed to the growing need for early cancer detection and the rising importance of epigenetic biomarkers in diagnosing and treating various malignancies. Changes in DNA methylation patterns, histone modifications, and chromatin remodeling have emerged as crucial indicators of cancer development, enabling more precise and personalized treatment approaches. With the increasing global burden of cancer and continued advancements in biomarker research, the oncology segment remains a major driver of market growth.

The U.S. Epigenetics Diagnostics Market is projected to grow at a CAGR of 16.5% through 2034, reaching USD 24.6 billion by the end of the forecast period. The country remains a frontrunner in this industry, thanks to its robust healthcare infrastructure, extensive research and development initiatives, and early adoption of precision medicine. Government agencies, including the National Institutes of Health (NIH), continue to fund breakthrough research in epigenetics, further accelerating innovation and commercialization. The rising prevalence of chronic diseases, increasing investments from biotech firms, and favorable regulatory policies are further cementing the U.S. as a dominant player in the global epigenetics diagnostics landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cancer and chronic diseases

- 3.2.1.2 Advancements in epigenomics research and technology

- 3.2.1.3 Growing demand for non-invasive diagnostics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of epigenetic diagnostics technologies

- 3.2.2.2 Limited standardization of testing methods

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Kits and reagents

- 5.3 Instruments

- 5.4 Software and services

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology diagnostics

- 6.3 Non-oncology diagnostics

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 DNA methylation

- 7.3 Histone methylation

- 7.4 MicroRNA modification

- 7.5 Chromatin structures

- 7.6 Other technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital and clinics

- 8.3 Pharmaceutical and biotechnology companies

- 8.4 Diagnostic laboratories

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abcam

- 10.2 Agilent Technologies

- 10.3 Diagenode

- 10.4 Dovetail Genomics

- 10.5 Element Biosciences

- 10.6 Illumina

- 10.7 Merck

- 10.8 New England Biolabs

- 10.9 PacBio

- 10.10 Promega

- 10.11 QIAGEN

- 10.12 Roche Diagnostics

- 10.13 Thermo Fisher Scientific

- 10.14 Zymo Research

表觀遺傳學:技術與全球市場

表觀遺傳學:技術與全球市場 表觀遺傳學市場規模、佔有率和成長分析(按產品、技術、方法、應用、最終用途和地區)- 產業預測 2025-2032

表觀遺傳學市場規模、佔有率和成長分析(按產品、技術、方法、應用、最終用途和地區)- 產業預測 2025-2032 表觀遺傳學藥物和診斷市場 - 預測 2025 年至 2030 年

表觀遺傳學藥物和診斷市場 - 預測 2025 年至 2030 年 表觀遺傳學市場:按產品、技術、工藝、應用和最終用戶分類 - 全球預測 2025-2030全球表觀遺傳學市場規模:依產品類型、應用、最終用戶、地區、範圍和預測2024-2032 年按產品、技術、應用和地區分類的表觀遺傳學市場報告

表觀遺傳學市場:按產品、技術、工藝、應用和最終用戶分類 - 全球預測 2025-2030全球表觀遺傳學市場規模:依產品類型、應用、最終用戶、地區、範圍和預測2024-2032 年按產品、技術、應用和地區分類的表觀遺傳學市場報告 美國表觀遺傳學市場規模、佔有率、趨勢分析報告:按產品、按技術、按應用、按最終用途、細分市場預測,2024-2030 年

美國表觀遺傳學市場規模、佔有率、趨勢分析報告:按產品、按技術、按應用、按最終用途、細分市場預測,2024-2030 年 表觀遺傳市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品和服務、技術、最終用戶、地區和競爭細分,2019-2029F

表觀遺傳市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品和服務、技術、最終用戶、地區和競爭細分,2019-2029F 表觀遺傳學市場評估:表觀遺傳變化類型、產品和服務、應用、最終用戶和地區的機會和預測(2017-2031)表觀遺傳學市場規模、佔有率、趨勢分析報告:按產品、按技術、按應用、按最終用途、按地區、細分市場預測,2024-2030 年

表觀遺傳學市場評估:表觀遺傳變化類型、產品和服務、應用、最終用戶和地區的機會和預測(2017-2031)表觀遺傳學市場規模、佔有率、趨勢分析報告:按產品、按技術、按應用、按最終用途、按地區、細分市場預測,2024-2030 年