|

市場調查報告書

商品編碼

1698308

災難性抗磷脂症候群市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Catastrophic Antiphospholipid Syndrome Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

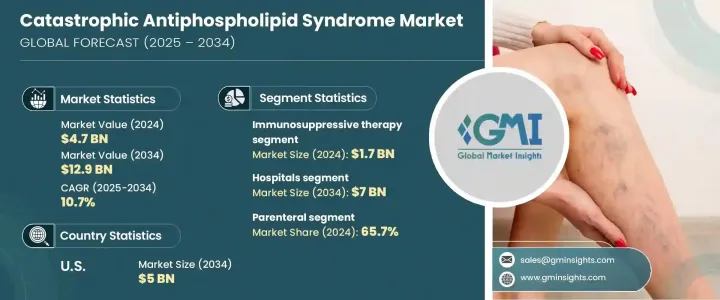

2024 年全球災難性抗磷脂症候群市場價值為 47 億美元,預計 2025 年至 2034 年的複合年成長率為 10.7%。市場發展的驅動力在於自體免疫疾病盛行率的上升以及人們對 CAPS(一種危及生命的抗磷脂症候群 (APS) 變異體)認知的不斷提高。診斷技術的進步正在增強早期疾病的檢測能力,增加對有效治療的需求。政府和私部門的研究經費正在進一步加速新療法的發展。

CAPS,也稱為阿什森症候群,是一種嚴重的自體免疫疾病,其特徵是影響多個器官的快速血栓事件。由於這種疾病的複雜性,治療方法多種多樣,通常包括抗凝血、皮質類固醇、血漿置換和其他免疫抑制療法。市場按治療類型、給藥途徑和最終用途設置進行細分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 47億美元 |

| 預測值 | 129億美元 |

| 複合年成長率 | 10.7% |

在治療方法中,免疫抑制療法仍占主導地位,2022 年的價值為 14 億美元,預計 2024 年將達到 17 億美元。這些藥物通常與抗凝血劑和皮質類固醇聯合使用,對於改善患者的預後至關重要。越來越多的臨床證據支持免疫抑制療法的有效性,從而增強了市場需求。此外,美國 FDA 和 EMA 等監管機構對孤兒藥的指定正在促進免疫抑制治療的採用,包括環磷醯胺、利妥昔單抗和皮質類固醇。

市場根據給藥途徑進一步分類,其中腸外治療佔據主導地位,到 2024 年將佔據 65.7% 的市場佔有率。預計在預測期內,該細分市場的複合年成長率將達到 10.6%。 CAPS 的嚴重性需要立即進行醫療干預,而腸外給藥由於其快速的治療效果而成為首選。透過腸外給藥方式使用利妥昔單抗和依庫珠單抗等生物療法的現像日益增多,進一步加強了市場的成長。輸液幫浦和預充式注射器等藥物輸送系統的創新正在提高治療效果並擴大應用。

就最終用途而言,醫院是最大的部分,預計到 2034 年將達到 70 億美元,複合年成長率為 10.5%。醫院配備了先進的診斷和治療設備,使其成為 CAPS 管理的主要中心。醫療保健支出的增加和醫院基礎設施的改善正在推動這一領域的成長。此外,醫院經常與製藥公司和研究機構合作,促進臨床試驗,為患者提供先進的治療方法。醫院中專業風濕病專家的不斷增加進一步促進了市場的擴大。

光是美國市場在 2024 年就創造了 19 億美元的收入,預計到 2034 年將達到 50 億美元。該國自體免疫疾病病例的不斷增加推動了對更好治療方案的需求。研究投入的增加和現代診斷系統的採用正在加速市場擴大。醫療保健專業人員對華法林和肝素等抗凝血劑的使用日益增多也支持了市場的成長。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 自體免疫疾病盛行率不斷上升

- 診斷和治療技術的進步

- 災難性抗磷脂症候群(CAPS)的認知不斷提高

- 醫療支出增加

- 產業陷阱與挑戰

- 治療費用高

- 專科治療有限

- 成長動力

- 成長潛力分析

- 監管格局

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依治療方式,2021 年至 2034 年

- 主要趨勢

- 抗凝血劑

- 免疫抑制治療

- 血漿置換療法

- 靜脈注射免疫球蛋白(IVIG)

- 其他治療

第6章:市場估計與預測:依管理路線,2021 年至 2034 年

- 主要趨勢

- 口服

- 腸外

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 專科診所

- 門診手術中心

- 其他最終用途

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott Laboratories

- AbbVie

- Boehringer Ingelheim International

- Bristol Myers Squibb Company

- Cadrenal Therapeutics

- Eli Lily and Company

- F. Hoffmann-La Roche

- Johnson & Johnson Services

- Merck

- Novartis

- Pfizer

- Sanofi

The Global Catastrophic Antiphospholipid Syndrome Market was valued at USD 4.7 billion in 2024 and is expected to grow at a CAGR of 10.7% from 2025 to 2034. The market is driven by the rising prevalence of autoimmune disorders and growing awareness of CAPS, a life-threatening variant of antiphospholipid syndrome (APS). Technological advancements in diagnostics are enhancing early disease detection, increasing demand for effective treatments. Government and private sector research funding are further accelerating the development of novel therapies.

CAPS, also known as Asherson's syndrome, is a severe autoimmune disorder characterized by rapid thrombotic events affecting multiple organs. Due to the complexity of this condition, treatment approaches vary and typically include anticoagulation, corticosteroids, plasma exchange, and other immunosuppressive therapies. The market is segmented by treatment type, route of administration, and end-use settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 10.7% |

Among treatments, immunosuppressive therapy remains the dominant segment, valued at USD 1.4 billion in 2022 and projected to reach USD 1.7 billion in 2024. These drugs, often combined with anticoagulants and corticosteroids, are vital for improving patient outcomes. Increasing clinical evidence supporting the efficacy of immunosuppressive therapy is bolstering market demand. Additionally, orphan drug designations by regulatory bodies such as the U.S. FDA and EMA are promoting the adoption of immunosuppressive treatments, including cyclophosphamide, rituximab, and corticosteroids.

The market is further categorized based on the route of administration, with parenteral treatments leading, accounting for 65.7% of the market share in 2024. This segment is expected to grow at a CAGR of 10.6% through the forecast period. The severity of CAPS necessitates immediate medical intervention, making parenteral administration the preferred choice due to its rapid therapeutic effects. The rising use of biologic therapies such as rituximab and eculizumab via parenteral delivery is further strengthening market growth. Innovations in drug delivery systems, including infusion pumps and prefilled syringes, are enhancing treatment efficacy and expanding adoption.

In terms of end-use, hospitals represent the largest segment, projected to reach USD 7 billion by 2034, growing at a CAGR of 10.5%. Hospitals are equipped with advanced diagnostic and treatment facilities, making them the primary centers for CAPS management. Rising healthcare expenditures and improved hospital infrastructure are driving this segment's growth. Additionally, hospitals frequently collaborate with pharmaceutical companies and research organizations to facilitate clinical trials, bringing advanced therapies to patients. The increasing presence of specialized rheumatologists in hospital settings is further contributing to the expanding market.

The U.S. market alone generated USD 1.9 billion in 2024 and is expected to reach USD 5 billion by 2034. The growing number of autoimmune disease cases in the country is fueling demand for better treatment options. Increased investment in research and the adoption of modern diagnostic systems are accelerating market expansion. The rising use of anticoagulants such as warfarin and heparin among healthcare professionals is also supporting market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of autoimmune disorders

- 3.2.1.2 Technological advancements in diagnostics and therapeutics

- 3.2.1.3 Rising awareness of catastrophic antiphospholipid syndrome (CAPS)

- 3.2.1.4 Increasing healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Limited availability of specialized treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anticoagulants

- 5.3 Immunosuppressive therapy

- 5.4 Plasma exchange therapy

- 5.5 Intravenous immunoglobulin (IVIG)

- 5.6 Other treatments

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Parenteral

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AbbVie

- 9.3 Boehringer Ingelheim International

- 9.4 Bristol Myers Squibb Company

- 9.5 Cadrenal Therapeutics

- 9.6 Eli Lily and Company

- 9.7 F. Hoffmann-La Roche

- 9.8 Johnson & Johnson Services

- 9.9 Merck

- 9.10 Novartis

- 9.11 Pfizer

- 9.12 Sanofi

雙特異性抗體市場:各治療領域,各作用機制,標的抗原,抗體不同格式,各主要地區,各主要企業:2035年前的產業趨勢與全球預測

雙特異性抗體市場:各治療領域,各作用機制,標的抗原,抗體不同格式,各主要地區,各主要企業:2035年前的產業趨勢與全球預測 DNA 片段市場按類型、產品類型、應用和最終用戶分類 - 2025 年至 2030 年全球預測

DNA 片段市場按類型、產品類型、應用和最終用戶分類 - 2025 年至 2030 年全球預測 雙特異性抗體市場:全球市場機會、劑量、專利、定價、銷售、臨床試驗趨勢(2030年)

雙特異性抗體市場:全球市場機會、劑量、專利、定價、銷售、臨床試驗趨勢(2030年) 診斷專業抗體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按抗體、應用、最終用戶、地區和競爭細分,2020-2030 年預測

診斷專業抗體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按抗體、應用、最終用戶、地區和競爭細分,2020-2030 年預測 雙特異性抗體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按適應症(癌症、發炎和自體免疫疾病等)細分,按地區和競爭情況,2020-2030 年預測

雙特異性抗體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按適應症(癌症、發炎和自體免疫疾病等)細分,按地區和競爭情況,2020-2030 年預測 TROP2抗體的全球市場:機會及臨床試驗趨勢(2030年)

TROP2抗體的全球市場:機會及臨床試驗趨勢(2030年) 中和抗體市場報告:2031 年趨勢、預測和競爭分析

中和抗體市場報告:2031 年趨勢、預測和競爭分析 雙特異性抗體和癌症專利態勢分析

雙特異性抗體和癌症專利態勢分析 抗體片段市場:按類型、抗體類型、應用分類 - 全球預測 2025-2030

抗體片段市場:按類型、抗體類型、應用分類 - 全球預測 2025-2030 抗體聯合研究及許可協議(2019-2024)

抗體聯合研究及許可協議(2019-2024)