|

市場調查報告書

商品編碼

1698556

汽車音響市場機會、成長動力、產業趨勢分析及2025-2034年預測Car Audio Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

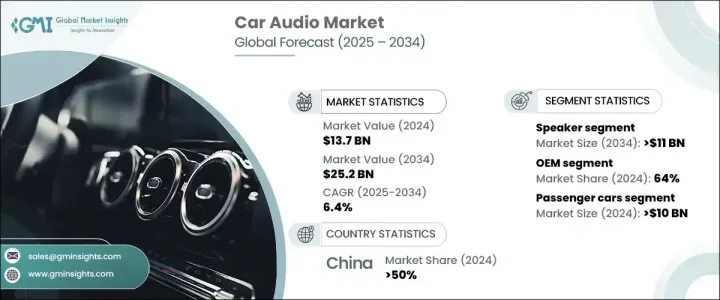

2024 年全球汽車音響市場價值為 137 億美元,預計 2025 年至 2034 年的複合年成長率為 6.4%。電動車 (EV) 的日益普及為該行業創造了新的機會。由於電動車降低了引擎噪音,它們提供了獨特的聲學環境,為創新音頻技術打開了大門。製造商正在開發解決方案來取代傳統的引擎聲音並增強車內的聽覺體驗。

受家庭和個人音響系統進步的影響,消費者越來越重視高品質的聲音。因此,購車者正在尋找能夠提供類似家庭設置的沉浸式、戲院式體驗的音響系統。對許多人來說,音訊品質已成為購買汽車的決定性因素,尤其是千禧世代和 Z 世代等年輕一代。空間音訊、高解析度串流媒體和可自訂的聲學設定等功能正在成為汽車音響系統的重要組成部分。為了滿足這些需求,汽車和售後市場製造商都在大力投資這些技術,將車輛轉變為優質的聲音環境。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 137 億美元 |

| 預測值 | 252億美元 |

| 複合年成長率 | 6.4% |

汽車音響市場按組件細分,包括揚聲器、擴大機、數位訊號處理器 (DSP)、麥克風和調諧器。 2024 年,揚聲器佔 45% 的佔有率,預計到 2034 年該細分市場將創造 110 億美元的產值。製造商正在使用碳纖維、芳綸和陶瓷注入聚合物等創新材料來提高揚聲器的性能。這些材料具有更高的剛性、更輕的重量和更優異的聲音傳輸性能,確保了車輛在溫度波動和振動等苛刻條件下的使用壽命和可靠性。

汽車音響市場的銷售管道分為OEM (原始設備製造商)和售後市場兩類。預計到 2034 年, OEM部門將創造 160 億美元的收入。汽車公司正專注於打造先進的音響系統,以提升車內音響體驗。這些系統採用尖端的音訊處理技術,包括基於物件的聲音,可產生 3D 音景,適應乘客位置和車輛的動態。這些系統中的先進演算法可以實現精確的聲音分級,在車廂內提供類似音樂廳的聲學沉浸式環境。

2024年,中國汽車音響市場將佔50%的佔有率。中國製造商正在客製化音響系統,以符合當地的喜好和聆聽習慣。機器學習等技術用於客製化聲音設定文件,而區域語言語音助理和文化相關內容使這些系統有別於全球競爭對手。聲學設計也經過最佳化,以適應中國城市獨特的城市聲音環境,為當地消費者提供增強的聆聽體驗。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 零件製造商

- 汽車音響系統製造商

- 軟體供應商

- 技術整合商

- 最終用途

- 利潤率分析

- 技術差異化因素

- 高解析度音訊技術

- 無線音訊解決方案

- 智慧連線

- 先進的放大系統

- 其他

- 重要新聞和舉措

- 成本細分分析

- 專利分析

- 監管格局

- 衝擊力

- 成長動力

- 消費者對優質音訊體驗的需求不斷成長

- 音訊設備與車輛的整合連接

- 消費者對個人化音訊體驗的需求

- 聲音技術的進步

- 產業陷阱與挑戰

- 消費者價格敏感度不斷提高

- 網路安全和資料隱私問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 揚聲器

- 雙向

- 三通

- 四通

- 擴大機

- 數位訊號處理器

- 麥克風

- 調諧器

第6章:市場估計與預測:按健全管理,2021 - 2034 年

- 主要趨勢

- 語音辨識

- 手動的

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車(LCV)

- 重型商用車(HCV)

第8章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 揚聲器

- 擴大機

- 數位訊號處理器

- 麥克風

- 調諧器

- 售後市場

- 揚聲器

- 擴大機

- 數位訊號處理器

- 麥克風

- 調諧器

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Alpine Electronics

- ASK Industries

- Bose

- Bowers & Wilkins

- Clarion

- Continental Aktiengesellschaft

- Dynaudio

- Focal JMLAB

- Harman

- JL Audio

- JVC KENWOOD

- KICKER (Stillwater Designs and Audio)

- Nippon Audiotronix

- NXP Semiconductors

- Panasonic

- Pioneer

- Premium Sound Solutions

- Rockford

- Sony

- ST Microelectronics

The Global Car Audio Market was valued at USD 13.7 billion in 2024 and is projected to grow at a CAGR of 6.4% from 2025 to 2034. The rising adoption of electric vehicles (EVs) creates new opportunities within this sector. As EVs reduce engine noise, they offer a unique acoustic environment that opens the door for innovative audio technologies. Manufacturers are developing solutions to replace traditional engine sounds and enhance the auditory experience within the vehicle.

Consumers are increasingly prioritizing high-quality sound, influenced by the advancements in home and personal audio systems. As a result, car buyers are looking for audio systems that offer immersive, theater-like experiences similar to their home setups. For many, audio quality has become a decisive factor when purchasing a vehicle, particularly among younger generations such as millennials and Gen Z. Features such as spatial audio, high-resolution streaming, and customizable acoustic settings are becoming vital components in car audio systems. To meet these demands, both automotive and aftermarket manufacturers are investing heavily in these technologies to transform vehicles into premium sound environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.7 billion |

| Forecast Value | $25.2 Billion |

| CAGR | 6.4% |

The car audio market is segmented by components, which include speakers, amplifiers, digital signal processors (DSP), microphones, and tuners. In 2024, speakers accounted for a 45% share, and this segment is expected to generate USD 11 billion by 2034. Manufacturers are enhancing speaker performance with innovative materials such as carbon fiber, aramid fiber, and ceramic-infused polymers. These materials provide increased rigidity, lighter weight, and superior sound transmission, ensuring longevity and reliability under demanding conditions within vehicles, such as temperature fluctuations and vibrations.

Sales channels in the car audio market are divided into OEM (original equipment manufacturer) and aftermarket categories. The OEM segment is projected to generate USD 16 billion by 2034. Automotive companies are focusing on creating advanced audio systems that elevate the in-vehicle sound experience. These systems use cutting-edge audio processing technologies, including object-based sound that generates 3D soundscapes, adapting to passenger positioning and the vehicle's dynamics. Advanced algorithms in these systems allow for precise sound staging, delivering an acoustically immersive environment similar to a concert hall within the vehicle cabin.

Chinese car audio market accounted for a 50% share in 2024. Manufacturers in China are customizing audio systems to align with local preferences and listening habits. Technologies such as machine learning are used to tailor sound profiles, while regional language voice assistants and culturally relevant content differentiate these systems from global competitors. Acoustic designs are also optimized to suit the unique urban sound environments in Chinese cities, offering an enhanced listening experience for local consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component manufacturers

- 3.2.2 Car audio system manufacturers

- 3.2.3 Software providers

- 3.2.4 Technology integrators

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology differentiators

- 3.4.1 High-resolution audio technology

- 3.4.2 Wireless audio solutions

- 3.4.3 Smart connectivity

- 3.4.4 Advanced amplification systems

- 3.4.5 Others

- 3.5 Key news & initiatives

- 3.6 Cost breakdown analysis

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising consumer demand for premium audio experience

- 3.9.1.2 Integrated connectivity of audio devices with vehicles

- 3.9.1.3 Consumer demand for personalized audio experiences

- 3.9.1.4 Advancements in sound technologies

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing consumer price sensitivity

- 3.9.2.2 Cybersecurity and data privacy concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Speaker

- 5.2.1 2-way

- 5.2.2 3-way

- 5.2.3 4-way

- 5.3 Amplifiers

- 5.4 DSP

- 5.5 Microphone

- 5.6 Tuners

Chapter 6 Market Estimates & Forecast, By Sound Management, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Voice recognition

- 6.3 Manual

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.2.1 Speaker

- 8.2.2 Amplifier

- 8.2.3 DSP

- 8.2.4 Microphone

- 8.2.5 Tuners

- 8.3 Aftermarket

- 8.3.1 Speaker

- 8.3.2 Amplifier

- 8.3.3 DSP

- 8.3.4 Microphone

- 8.3.5 Tuners

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alpine Electronics

- 10.2 ASK Industries

- 10.3 Bose

- 10.4 Bowers & Wilkins

- 10.5 Clarion

- 10.6 Continental Aktiengesellschaft

- 10.7 Dynaudio

- 10.8 Focal JMLAB

- 10.9 Harman

- 10.10 JL Audio

- 10.11 JVC KENWOOD

- 10.12 KICKER (Stillwater Designs and Audio)

- 10.13 Nippon Audiotronix

- 10.14 NXP Semiconductors

- 10.15 Panasonic

- 10.16 Pioneer

- 10.17 Premium Sound Solutions

- 10.18 Rockford

- 10.19 Sony

- 10.20 ST Microelectronics

全球汽車音響市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球汽車音響市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年汽車音響全球市場報告

2025 年汽車音響全球市場報告 汽車擴大機市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

汽車擴大機市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 汽車高級音訊系統市場:按組件、聲音管理、車輛類型和銷售管道- 2025-2030 年全球預測

汽車高級音訊系統市場:按組件、聲音管理、車輛類型和銷售管道- 2025-2030 年全球預測 中國的汽車音響系統產業(2024年)

中國的汽車音響系統產業(2024年) 汽車擴大機市場,按類別、擴大機、配銷通路、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測汽車高保真系統市場:按組件類型、車輛類型、技術、功率、連接性、聲音類型 - 2025-2030 年全球預測

汽車擴大機市場,按類別、擴大機、配銷通路、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測汽車高保真系統市場:按組件類型、車輛類型、技術、功率、連接性、聲音類型 - 2025-2030 年全球預測 2024-2028年全球高階汽車音訊系統市場到 2030 年汽車擴大機(汽車擴大機)的全球市場預測:按類型、類別、車型、技術、分銷管道、地區全球汽車音響市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

2024-2028年全球高階汽車音訊系統市場到 2030 年汽車擴大機(汽車擴大機)的全球市場預測:按類型、類別、車型、技術、分銷管道、地區全球汽車音響市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測