|

市場調查報告書

商品編碼

1699266

快速流感診斷測試(RIDT)市場機會、成長動力、產業趨勢分析及2025-2034年預測Rapid Influenza Diagnostic Tests (RIDT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

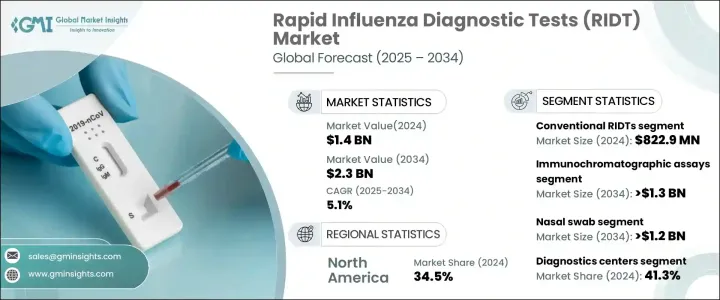

2024 年全球快速流感診斷檢測市場規模達到 14 億美元,預計 2025 年至 2034 年的複合年成長率為 5.1%。季節性流感盛行率的上升、即時檢測的進步以及診斷方法的不斷創新正在推動市場成長。世界各國政府正在加強流感監測並進行宣傳活動,進一步擴大 RIDT 的採用。技術進步顯著提高了測試準確性,數位 RIDT 提供了更高的靈敏度和特異性。

從定性到半定量 RIDT 的轉變增加了它們的臨床相關性,並且能夠檢測多種呼吸道病原體的多重測試變得越來越普遍。人工智慧 (AI) 和機器學習正在最佳化測試解釋、減少錯誤並使診斷更容易獲得。醫療保健基礎設施方面不斷增加的投資也提高了這些測試的可用性。監管機構正在透過簡化核准和對公共衛生計劃的財務支持來支持快速流感診斷。增加診斷測試的資金有助於提高公眾意識,鼓勵早期發現和治療,並推動市場向前發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 14億美元 |

| 預測值 | 23億美元 |

| 複合年成長率 | 5.1% |

RIDT 市場根據產品類型、技術、樣品類型、最終用途和地區進行細分。傳統 RIDT 領域在 2024 年創造了 8.229 億美元的收入。這些測試由於其價格實惠且易於取得而仍然被廣泛使用,特別是在醫療保健基礎設施有限的地區。它們設計簡單、生產成本低,非常適合用於公共衛生項目,確保廣泛普及。由於易於使用且只需極少的培訓要求,這些測試可以在各種環境中實施,包括診所、工作場所和學校。快速的結果可以實現快速決策,從而在管理季節性流感爆發方面非常有效。

從技術角度來看,免疫層析檢測預計將引領市場成長,預計複合年成長率為 5.9%,到 2034 年將達到 13 億美元以上。這些測試具有高靈敏度和特異性,對於檢測兒童和老年人等弱勢群體中的流感特別有價值。分散的醫療保健環境(包括藥局和緊急護理中心)對免疫層析檢測的需求正在增加。其緊湊的設計和最低限度的設備要求使其非常適合此類場所。持續的技術進步進一步提高了它們的速度和準確性,使其成為醫療保健專業人士的首選。

根據樣本類型,鼻拭子市場預計將以 5.9% 的複合年成長率成長,到 2034 年將超過 12 億美元。鼻拭子因其易於使用且在檢測流感方面具有高準確度而被廣泛使用。它們比其他樣本採集方法侵入性更小,適合兒童和成人。它們能夠捕獲高病毒量,從而有效地進行早期流感診斷,使醫療服務提供者在照護端和實驗室檢測環境中受益。

2024 年,診斷中心佔據了最高的最終用途收入佔有率,為 41.3%。這些設施提供先進的診斷技術並僱用訓練有素的專業人員,確保準確且有效率的測試。對綜合診斷服務(包括多種呼吸道感染的多重檢測)的需求不斷成長,導致診斷中心對 RIDT 的依賴性不斷增強。這些設施在大規模流感監測計畫中發揮著至關重要的作用,鞏固了其市場主導地位。

2024 年,北美佔據了 34.5% 的最大市場佔有率,這得益於完善的醫療保健系統、快速檢測試劑盒的廣泛普及以及即時檢測的日益普及。 2021 年美國市場價值為 3.31 億美元,2022 年將增至 3.658 億美元,2023 年將增至 4.013 億美元,反映出其在該地區的主導地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 流感流行率不斷上升

- 技術進步

- 早期流感診斷和管理的需求不斷成長

- 快速診斷測試日益普及

- 產業陷阱與挑戰

- 缺乏熟練的專業人員

- 嚴格的規定

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 定價分析

- 差距分析

- 波特的分析

- PESTEL分析

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 常規RIDT

- 數字RIDT

第6章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 免疫層析分析

- 橫向流動試驗

- 聚合酶連鎖反應

- 其他技術

第7章:市場估計與預測:依樣本類型,2021 - 2034 年

- 主要趨勢

- 鼻拭子

- 咽拭子

- 其他樣本類型

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 診斷中心

- 醫院

- 研究實驗室

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 3B BlackBio

- Abbott

- Access Bio

- BD

- bioMérieux

- CHEMBIO

- DiaSorin

- Meridian

- Quidel Corporation

- Roche

- SEKISUI

- Siemens HEALTHINEERS

- Thermo Fisher

The Global Rapid Influenza Diagnostic Tests Market reached USD 1.4 billion in 2024 and is projected to grow at a CAGR of 5.1% from 2025 to 2034. The rising prevalence of seasonal flu, advancements in point-of-care testing, and continuous innovations in diagnostic methods are driving market growth. Governments worldwide are strengthening influenza surveillance and running awareness campaigns, further expanding the adoption of RIDTs. Technological advancements have significantly improved test accuracy, with digital RIDTs offering enhanced sensitivity and specificity.

The shift from qualitative to semi-quantitative RIDTs has increased their clinical relevance, and multiplexed tests capable of detecting multiple respiratory pathogens are becoming more common. Artificial intelligence (AI) and machine learning are optimizing test interpretation, reducing errors, and making diagnostics more accessible. Growing investments in healthcare infrastructure are also improving the availability of these tests. Regulatory bodies are supporting rapid influenza diagnosis through streamlined approvals and financial support for public health initiatives. Increased funding for diagnostic testing is helping expand public awareness, encouraging early detection and treatment, and driving the market forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.1% |

The RIDTs market is segmented based on product type, technology, sample type, end-use, and region. The conventional RIDTs segment generated USD 822.9 million in 2024. These tests remain widely used due to their affordability and ease of access, particularly in regions with limited healthcare infrastructure. Their simple design and low production cost make them ideal for use in public health programs, ensuring broad availability. The ease of use and minimal training requirements allow these tests to be implemented in a variety of settings, including clinics, workplaces, and schools. Fast results enable quick decision-making, making them highly effective in managing seasonal flu outbreaks.

By technology, immunochromatographic assays are expected to lead market growth with a projected CAGR of 5.9%, reaching over USD 1.3 billion by 2034. These tests offer high sensitivity and specificity, making them particularly valuable for detecting influenza in vulnerable populations, such as children and the elderly. The demand for immunochromatographic assays is increasing in decentralized healthcare settings, including pharmacies and urgent care centers. Their compact design and minimal equipment requirements make them well-suited for such locations. Continued technological advancements have further improved their speed and accuracy, making them a preferred choice among healthcare professionals.

Based on sample type, the nasal swab segment is projected to grow at a CAGR of 5.9%, surpassing USD 1.2 billion by 2034. Nasal swabs are widely used due to their ease of application and high accuracy in detecting influenza. They are less invasive than other sample collection methods, making them suitable for both children and adults. Their ability to capture high viral loads makes them effective in early influenza diagnosis, benefiting healthcare providers in both point-of-care and laboratory testing environments.

Diagnostic centers accounted for the highest end-use revenue share of 41.3% in 2024. These facilities offer advanced diagnostic technologies and employ trained professionals, ensuring accurate and efficient testing. The increasing demand for comprehensive diagnostic services, including multiplex testing for multiple respiratory infections, has contributed to the growing reliance on RIDTs in diagnostic centers. These facilities play a crucial role in large-scale influenza monitoring programs, reinforcing their market dominance.

North America captured the largest market share of 34.5% in 2024, driven by a well-established healthcare system, the widespread availability of rapid test kits, and the increasing adoption of point-of-care testing. The US market was valued at USD 331 million in 2021, rising to USD 365.8 million in 2022 and USD 401.3 million in 2023, reflecting its dominant position within the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of influenza

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising demand for early influenza diagnosis and management

- 3.2.1.4 Increasing popularity of rapid diagnostic tests

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 Stringent regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Pricing analysis

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional RIDTs

- 5.3 Digital RIDTs

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunochromatographic assays

- 6.3 Lateral flow assays

- 6.4 PCR

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Sample Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Nasal swab

- 7.3 Throat swab

- 7.4 Other sample types

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostic centers

- 8.3 Hospitals

- 8.4 Research laboratories

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3B BlackBio

- 10.2 Abbott

- 10.3 Access Bio

- 10.4 BD

- 10.5 bioMérieux

- 10.6 CHEMBIO

- 10.7 DiaSorin

- 10.8 Meridian

- 10.9 Quidel Corporation

- 10.10 Roche

- 10.11 SEKISUI

- 10.12 Siemens HEALTHINEERS

- 10.13 Thermo Fisher

2025 年至 2033 年流感診斷市場報告(按產品、檢測類型、流感類型、最終用戶和地區分類)

2025 年至 2033 年流感診斷市場報告(按產品、檢測類型、流感類型、最終用戶和地區分類) 流感診斷全球市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

流感診斷全球市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 快速流感診斷檢測市場,按類型、按產品類型、按最終用途、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測

快速流感診斷檢測市場,按類型、按產品類型、按最終用途、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測 流感診斷市場規模、佔有率、成長分析、按產品、按測試、按最終用戶、按地區 - 行業預測,2024-2031 年

流感診斷市場規模、佔有率、成長分析、按產品、按測試、按最終用戶、按地區 - 行業預測,2024-2031 年 流感診斷市場:按測試類型、最終用戶分類 - 2025-2030 年全球預測

流感診斷市場:按測試類型、最終用戶分類 - 2025-2030 年全球預測 全球流感診斷市場規模(按產品、最終用戶、測試類型、地區、範圍和預測)

全球流感診斷市場規模(按產品、最終用戶、測試類型、地區、範圍和預測) 2024-2028年全球流感診斷市場

2024-2028年全球流感診斷市場 流感診斷市場 - 全球產業規模、佔有率、趨勢、機會和預測,按測試類型、最終用戶、地區和競爭細分,2019-2029F

流感診斷市場 - 全球產業規模、佔有率、趨勢、機會和預測,按測試類型、最終用戶、地區和競爭細分,2019-2029F 2024-2032 年按產品、測試類型、流感類型、最終用戶和地區分類的流感診斷市場報告

2024-2032 年按產品、測試類型、流感類型、最終用戶和地區分類的流感診斷市場報告 全球流感診斷市場:市場規模和份額分析(按產品、測試類型和最終用戶)、行業需求預測(截至 2030 年)

全球流感診斷市場:市場規模和份額分析(按產品、測試類型和最終用戶)、行業需求預測(截至 2030 年)