|

市場調查報告書

商品編碼

1699289

眼外傷設備市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Ocular Trauma Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

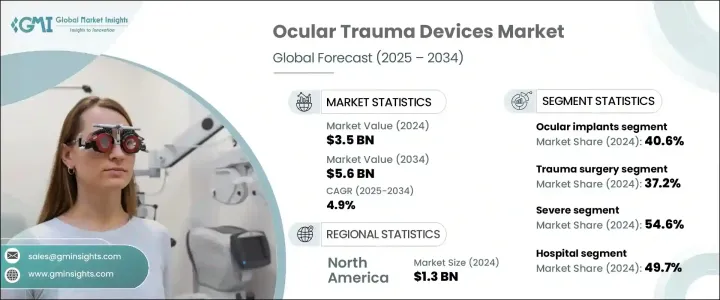

2024 年全球眼部外傷設備市場規模達到 35 億美元,預計 2025 年至 2034 年期間的複合年成長率將達到 4.9%,這主要得益於眼外傷患病率的上升以及對專門治療解決方案的需求不斷成長。眼睛創傷仍然是一個重大的公共衛生問題,其傷害範圍從輕微擦傷到需要立即進行醫療干預的嚴重穿透傷。早期診斷的進步、對可用治療方案的認知的提高以及尖端手術技術的採用正在推動市場擴張。由於醫療保健提供者優先考慮對眼部創傷病例進行快速有效的干涉,對高精度創傷設備的需求持續攀升。

微創手術和技術先進的設備在改善患者預後、縮短恢復時間和提高整體手術效率方面發揮著至關重要的作用。生物工程眼部植入物、機器人輔助眼科手術和眼科黏彈性裝置(OVD)等創新正在獲得關注,進一步促進了市場的積極發展。此外,全球各國政府的措施和醫療保健投資的增加正在加強眼科研究和開發力度,從而帶來更有效的創傷管理解決方案。人工智慧與診斷工具和手術系統的整合進一步簡化了治療方案,提高了治療精確度和效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 35億美元 |

| 預測值 | 56億美元 |

| 複合年成長率 | 4.9% |

醫院、專科診所和門診手術中心擴大採用眼部外傷設備,在推動這一上升趨勢中發揮關鍵作用。隨著全球創傷相關手術數量的不斷增加,醫療機構正在積極升級其眼科設備,從而更廣泛地採用創新解決方案。

根據產品類型,眼外傷設備市場分為手術器械、人工水晶體 (IOL)、眼部植入物、眼科黏彈性裝置 (OVD) 和其他相關設備。 2024 年,眼部植入物佔據了 40.6% 的市場佔有率,這得益於需要人工水晶體和視網膜假體等輔助解決方案的嚴重創傷病例數量的增加。這些植入物在因事故、鈍力傷害或穿透性創傷造成的結構性損傷後,對於恢復視力和維持眼部完整性起著至關重要的作用。複雜性眼部損傷的發生率不斷上升,推動了對專門用於有效治療嚴重病例的植入物的需求。

根據應用,市場還分為創傷手術、視網膜剝離、白內障手術、青光眼管理和其他手術。 2024 年,創傷外科佔據了 37.2% 的市場佔有率,這主要是由於鈍力創傷、穿透性傷口和需要高級外科手術干預的化學燒傷發生率不斷上升。嚴重眼外傷的治療涉及止血、結構修復和視功能恢復,需要使用高精度手術工具。對複雜的創傷管理解決方案的需求不斷成長,正在促進市場的擴張。

美國仍然是眼外傷設備產業的主導力量,2024 年市場價值為 12.3 億美元,預計到 2032 年將達到 18 億美元。作為醫療技術的全球領導者,美國處於眼科創新的前沿,包括機器人眼科手術、生物工程植入物和微創手術工具。來自私營和公共部門的投資正在推動突破性研究,使製造商能夠開發治療眼外傷的下一代解決方案。隨著眼部外傷護理的不斷進步,未來幾年市場將持續成長。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 眼外傷盛行率上升

- 技術進步

- 提高認知和早期診斷

- 有利的政府措施和保險覆蓋

- 產業陷阱與挑戰

- 治療費用高昂

- 缺乏熟練的醫療保健專業人員

- 成長動力

- 成長潛力分析

- 監管格局

- 報銷場景

- 未來市場趨勢

- 差距分析

- 技術格局

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 競爭定位矩陣

- 供應商矩陣分析

- 策略儀表板

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 手術器械

- 人工水晶體(IOL)

- 眼部植入物

- 眼科黏彈裝置(OVD)

- 其他產品

第6章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 創傷外科

- 視網膜剝離

- 白內障手術

- 青光眼管理

- 其他應用

第7章:市場估計與預測:依創傷嚴重程度,2021 年至 2034 年

- 主要趨勢

- 輕微

- 緩和

- 劇烈

第8章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 眼科診所

- 門診手術中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 亞太地區

- 日本

- 中國

- 印度

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Alcon

- Bausch + Lomb

- Carl Zeiss Meditec

- CooperVision

- Essilor Instruments

- Haag-Streit Group

- Innovative Optics

- IRIDEX Corporation

- Johnson & Johnson Vision

- Leica Microsystems

- Optos

- Sonomed Escalon

- Topcon Corporation

The Global Ocular Trauma Devices Market reached USD 3.5 billion in 2024 and is projected to expand at a CAGR of 4.9% from 2025 to 2034, driven by the rising prevalence of eye injuries and the growing need for specialized treatment solutions. Ocular trauma remains a significant public health concern, with incidents ranging from minor abrasions to severe penetrating injuries that require immediate medical intervention. Advancements in early diagnosis, increased awareness of available treatment options, and the adoption of cutting-edge surgical techniques are fueling market expansion. As healthcare providers prioritize rapid and effective intervention for eye trauma cases, the demand for high-precision trauma devices continues to climb.

Minimally invasive procedures and technologically advanced devices are playing a crucial role in improving patient outcomes, reducing recovery time, and enhancing overall surgical efficiency. Innovations such as bioengineered ocular implants, robotic-assisted eye surgeries, and ophthalmic viscoelastic devices (OVDs) are gaining traction, further contributing to the market's positive trajectory. Moreover, government initiatives and increased healthcare investments worldwide are strengthening ophthalmic research and development efforts, leading to the introduction of more effective trauma management solutions. The integration of artificial intelligence in diagnostic tools and surgical systems is further streamlining treatment protocols, offering enhanced precision and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 4.9% |

The increasing adoption of ocular trauma devices across hospitals, specialty clinics, and ambulatory surgical centers is playing a pivotal role in driving this upward trend. With a growing number of trauma-related surgeries performed globally, healthcare facilities are actively upgrading their ophthalmic equipment, leading to higher adoption of innovative solutions.

By product type, the ocular trauma devices market is segmented into surgical instruments, intraocular lenses (IOLs), ocular implants, ophthalmic viscoelastic devices (OVDs), and other related devices. Ocular implants captured a 40.6% market share in 2024, propelled by the rising number of severe trauma cases necessitating secondary solutions such as artificial lenses and retinal prostheses. These implants play a vital role in restoring vision and maintaining ocular integrity following structural damage caused by accidents, blunt force injuries, or penetrating trauma. The increasing prevalence of complex ocular injuries is fueling demand for specialized implants designed to address severe cases effectively.

The market is also categorized by application into trauma surgery, retinal detachment, cataract surgery, glaucoma management, and other procedures. Trauma surgery accounted for a 37.2% market share in 2024, driven by the rising incidence of blunt force trauma, penetrating wounds, and chemical burns requiring advanced surgical interventions. Managing severe ocular trauma involves hemorrhage control, structural repairs, and visual function restoration, necessitating the use of high-precision surgical tools. The growing demand for sophisticated trauma management solutions is reinforcing the market's expansion.

The United States remains a dominant force in the ocular trauma devices industry, with the market valued at USD 1.23 billion in 2024 and expected to generate USD 1.8 billion by 2032. As a global leader in medical technology, the country is at the forefront of ophthalmic innovations, including robotic eye surgeries, bioengineered implants, and minimally invasive surgical tools. Investments from both private and public sectors are fueling groundbreaking research, enabling manufacturers to develop next-generation solutions for treating traumatic eye injuries. With continuous advancements in ocular trauma care, the market is set to witness sustained growth in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of ocular trauma

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing awareness and early diagnosis

- 3.2.1.4 Favorable government initiatives and insurance coverage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Technology landscape

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Vendor matrix analysis

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical instruments

- 5.3 Intraocular lenses (IOLs)

- 5.4 Ocular implants

- 5.5 Ophthalmic viscoelastic devices (OVDs)

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Trauma surgery

- 6.3 Retinal detachment

- 6.4 Cataract surgery

- 6.5 Glaucoma management

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Trauma Severity, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Mild

- 7.3 Moderate

- 7.4 Severe

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ophthalmic clinics

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alcon

- 10.2 Bausch + Lomb

- 10.3 Carl Zeiss Meditec

- 10.4 CooperVision

- 10.5 Essilor Instruments

- 10.6 Haag-Streit Group

- 10.7 Innovative Optics

- 10.8 IRIDEX Corporation

- 10.9 Johnson & Johnson Vision

- 10.10 Leica Microsystems

- 10.11 Optos

- 10.12 Sonomed Escalon

- 10.13 Topcon Corporation

2025 年至 2033 年眼科設備市場報告(按產品類型、應用、最終用途和地區)

2025 年至 2033 年眼科設備市場報告(按產品類型、應用、最終用途和地區) 眼科醫療設備市場規模、佔有率、成長分析、按產品、按最終用戶、按應用、按地區 - 按行業預測 2024-2031

眼科醫療設備市場規模、佔有率、成長分析、按產品、按最終用戶、按應用、按地區 - 按行業預測 2024-2031 眼外傷設備市場規模、佔有率、趨勢分析報告:按設備類型、按適應症、按最終用途、按地區、細分市場預測,2025-2030 年

眼外傷設備市場規模、佔有率、趨勢分析報告:按設備類型、按適應症、按最終用途、按地區、細分市場預測,2025-2030 年 2030 年眼科器材市場預測:按產品、應用、最終用戶和地區分類的全球分析

2030 年眼科器材市場預測:按產品、應用、最終用戶和地區分類的全球分析 眼科設備市場:按產品、按應用分類 - 2025-2030 年全球預測

眼科設備市場:按產品、按應用分類 - 2025-2030 年全球預測 眼科設備市場:按產品類型、應用和最終用戶分類 - 全球預測 2025-2030

眼科設備市場:按產品類型、應用和最終用戶分類 - 全球預測 2025-2030 糖尿病眼科疾病設備市場:按產品類型、最終用戶、適應症、技術 - 全球預測 2025-2030

糖尿病眼科疾病設備市場:按產品類型、最終用戶、適應症、技術 - 全球預測 2025-2030 膠囊張力環市場:按產品類型、材料、應用、最終用戶、分銷管道 - 全球預測 2025-2030

膠囊張力環市場:按產品類型、材料、應用、最終用戶、分銷管道 - 全球預測 2025-2030 眼科設備:市場洞察·競爭環境·市場預測 (~2030年)

眼科設備:市場洞察·競爭環境·市場預測 (~2030年) 糖尿病眼科疾病設備的全球市場

糖尿病眼科疾病設備的全球市場